Two Things That Signal Job Growth Is About To Slide

While we will shortly show in our full payrolls preview that expectations for December payroll growth are clustered around 200,000, in his daily note, TS Lombard economist Steven Blitz writes that in the coming months one should expect the pace of hiring to slow, as it always does late cycle – aided and abetted by tightening monetary policy (and that’s even without the BLS admitting the recent finding by the Philly Fed that payroll growth in Q2 was just 10,000 not 1,100,000 as initially reported). Recall that in 2005, the median monthly change in nonfarm payrolls was 175,000, when then dropped to 143,000 in 2006 and 61,500 in 2007. In 2018, the median was 165,000 and123,500 in 2019. In other words, “expect the monthly hiring pace to drop closer to 150,000 in Q1.”

But where, in a world where most indicators such as initial claims, ADP, Challenger layoffs and ISM employment data are showing strong labor market data, should one look to find downward inflection points or their harbingers? According to Blitz, there are two critical datapoints to keep an eye on, the first of which we discussed just yesterday, namely the data series on new hires and the hiring rate from the JOLTs report, which as we showed had unexpectedly shrunk to the lowest level in two years even as the level of quits has remained surprising high.

The other data point is corporate profits as proxied most directly (and without any non-GAAP adjustments by management or political operatives at the BLS) by the amount of taxes corporations pay to the Treasury.

Starting with the former, Blitz writes: “Indicating the coming slowdown in hiring, against the backdrop of a tighter monetary policy, although still not tight, are hiring rates dropping back to 2018 levels.” Helping to drive the drop in hiring rates is profit growth slowing in Q4. December corporate tax payments to the Federal government dropped from Q3, and payments were below December 2021 levels. Earnings are a key determinant of growth in hiring and wages.”

Let’s take a closer look at the hiring rate which we first touched upon yesterday: In November the private sector hiring rate (which according to the TS Lombard strategist is more meaningful than job openings in terms of identifying cyclical turns) slipped to its 2018 average, along with manufacturing.

Perhaps more telling about the cycle is that the hiring rate for business and professional services is sinking further below its 2018 average. As Blitz explains, when economies drop into recession, sectors are impacted differently and in the coming downturn it is reasonable to presume that the area least effected by the inability to work in person is the one where the downturn hits first and hardest. The hiring rate in accommodation and food services remains high relative to 2018, a function of travel, commuting and otherwise, returning to normal, however slowly.

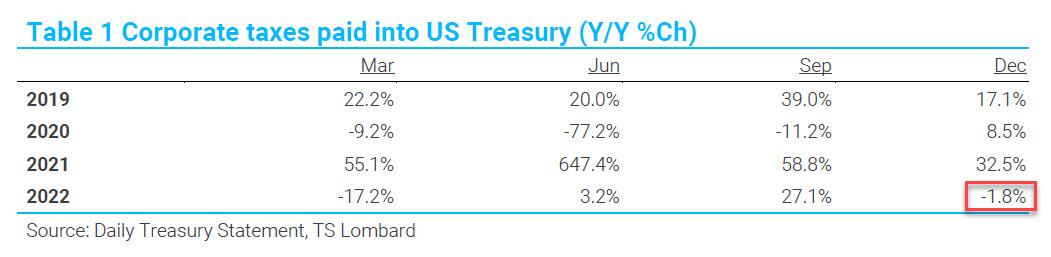

What about profits? Obviously, profits are critical to the pace of hiring and job gains, and corporate tax receipts at the Treasury – which the BLS can’t seasonally adjust or tamper with for political reasons or otherwise – suggest Q4 was not as good a quarter for earnings. Blitz explains that US firms pay estimates of current year taxes quarterly, and when December falls short it means firms figured they overpaid in September, given what were their full-year earnings expectations at the time.

Well, as shown below, December tax receipts were 1.8% below year-ago levels, compared with 32.5% last year. In September, tax payments were 27.1% above year ago levels, which gave us the signal at the time that quarterly profits would be strong.

As the TS Lombard strategist concludes, “with the fall off in Q4 and the normal lag in hiring relative to earnings, a slower pace of job growth should be expected in the months ahead – as indicated by the drop in the hiring rate…. In sum, the 2022 pace of extraordinary job growth despite record low unemployment is coming to an end. The coming months should see the pace slow towards 150,000, on par with prior late-cycle periods. It is too soon to say this is, in total, precursor to recession, but the sharp drop-off in the hiring rate for business and professional services may be more telling of an impending cyclical turn. Once hiring drops well-enough below 200,000 the Fed’s pace of rate hikes will slip to 25BP and then 0 in short order.”

Tyler Durden

Thu, 01/05/2023 – 20:38

https://www.zerohedge.com/markets/two-things-signal-job-growth-about-slide