Liquidity Is More Important Than Interest Rates

Authored by Bruce Wilds via Advancing Time blog,

It would be best to consider the idea that if you have good credit you will always be able to get a loan a myth. This is not about you, it is about markets and reality. People learn in a credit crunch that liquidity is far more important than interest rates. We are currently in a credit tightening cycle and it seems that greed has temporally overshadowed the potential this has to impact the economy.

Many years of an easy credit environment have numbed people to the reality that credit is not a guaranteed right. This is a reality that can hit us like a slap in the face. The notion you stand a snowball’s chance in hell of getting a loan in such an environment has yet to dawn on many people.

Part of what we will see in the coming months could be simply an adjustment in the flow of capital to those that want it most or can afford it. Much of what may developer is a lack of willingness to lend considering the possibility the risk of not being repaid will increase in a difficult economy. The existence of so-called “loan sharks” underlines the idea that if someone is desperate to borrow money they will often put themselves in danger to do so. Loan sharks, which generally operate outside the law, offer loans at extremely high-interest rates and have strict terms of collection if the loan is not repaid.

Most people having not experienced such an environment may have difficulty imagining such a scenario. This is partially due to what may be considered “memory bias” or “recency bias.” This can result in confusion as new situations arise. Memories tend to be clouded by people incorrectly believing that recent events will likely occur again. This tendency obscures the probability the future may be quite different from the past and leads people to make poor decisions based on the recent past.

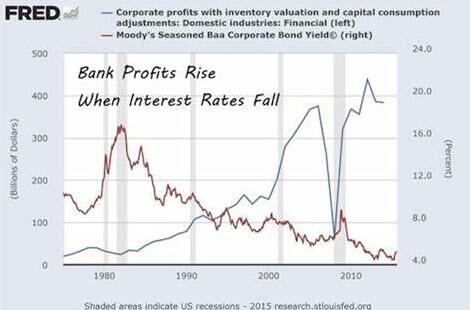

Like many businesses, the banking sector has changed over the years. While I have had some difficulty pulling up numbers to support my premise, the banking industry today is far different than it was a few decades ago. The chart above is from 2015, a similar chart from 2011 shows net interest income at 55%, I suspect it has continued to drop over the years.

A bank is a financial institution licensed to accept deposits and make loans. Not only do banks protect our money, they lend out this money to create profits. But they also perform a lot of other financial services. That said, banks are not shy about placing upon customers a lot of fees and other charges.

-

The three main business segments for a bank are retail banking, wholesale banking, and wealth management.

-

Retail banking or personal banking involves deposits, mortgages, loans, and credit cards.

-

Wholesale banking is related to sales and trading and mergers and acquisitions.

-

Wealth management generates revenue through retail brokerage services and asset management.

The simple and ugly truth is banks are not “good neighbors” there to serve and be concerned about the community. Banks do not make much money on small loans at low-interest rates. The cost of making these loans far outweighs the income flowing from them even before factoring in the risk of default. This is why most small businesses must turn to other sources in order to find financing and a lot of these are loans “hidden off the balance sheet” at much higher rates. When push comes to shove, the banks will be fast to throw you under the bus.

Interest Rates Have Fallen Over The Decades

This swings back to the title of this piece, interest rates are still very low compared to those we experienced during the 80s and 90s. To someone in need of a loan a quarter or even a few full points of interest is often not as big a deal as the availability of credit. When credit windows slam closed people get scared and shadow banking or unregulated lending soars.

Liquidity is the life blood of commerce. The massive growth in the financial sector versus Main Street, the GDP, and the real economy has made debt a major concern. Credit markets will be coming under a lot of pressure as a great deal of this debt coming due. Adding to the problem is that much of it is short-term debt that must be rolled over or extended. It will be interesting how this plays out in a “risk off” environment.

Some of these facts underline the importance of liquidity. The Fed is boxed in by the hyper-reaction of investors to anything it does. It needs to get investors to refocus on profits, margins, and risk. The combination of cheap money, and too much of it, has fueled speculation and blown the lid off markets in recent years. This makes it difficult to argue the stock market has been efficient in discovering the true value of companies.

Clearly, 2022 was the year of interest rate hikes, and while they may continue higher, 2023 will be the year where they really begin to take a toll on the economy. While recessions halt inflation the issue is just how much irreparable damage it will inflict on Main Street and society as the “lag effect” hits us in the face. The stock market is not cheap, earnings will most likely fall and stock prices with them. In response, expect tapped-out consumers to cut back on spending, unemployment to rise, and a lot of small businesses to fail.

A lack of liquidity can be poisonous. When you need money, whether the amount is small or large, not being able to get it can lead to a life-changing or grave outcome. Contagion from one area tends to spill over into other sectors of the economy and markets. It is important to point out that housing values are a far bigger issue for most Americans than stocks. Still, these markets do influence each other. Dealing with a “bubble economy” is always a problem and results in investors and people, in general, to buy high and sell low, often with devastating consequences.

Tyler Durden

Mon, 01/09/2023 – 08:20

https://www.zerohedge.com/markets/liquidity-more-important-interest-rates