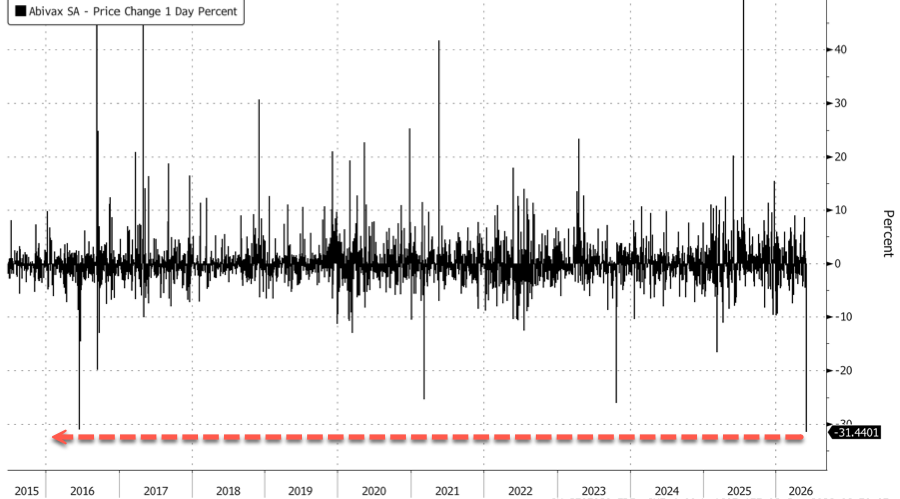

Abivax Crashes Most On Record After Cancer Cases In Trial Data Spooks Wall Street

French biotech Abivax suffered its largest intraday decline on record after reporting new data on its lead experimental inflammatory bowel disease drug, which showed cancer cases among patients in the clinical trial. The new data certainly point to regulatory headwinds and raise the risk profile for approval.

Abivax’s ABTECT maintenance data showed strong efficacy readout, with both once-daily obefazimod doses meeting the primary endpoint at week 44. Clinical remission rates were 50.8% for the 25 mg dose and 51.3% for the 50 mg dose, versus 10.4% for placebo, implying placebo-adjusted remission rates of about 39% to 40% and highly statistically significant results.

The problem for the stock was not efficacy, but safety optics…

Goldman analyst Esah Hayat pointed out that the market was focused not on efficacy but on cancer cases among patients taking the higher doses of obefazimod:

ABTECT maintenance trial out yday (press release) – “at week 44, both the 25 mg and 50 mg once-daily obefazimod doses met the primary endpoint, demonstrating placebo-adjusted clinical remission rates of ∆39.3% and ∆40.3%, respectively (25 mg: 50.8%, 50 mg: 51.3% vs placebo 10.4%; p<0.0001).”

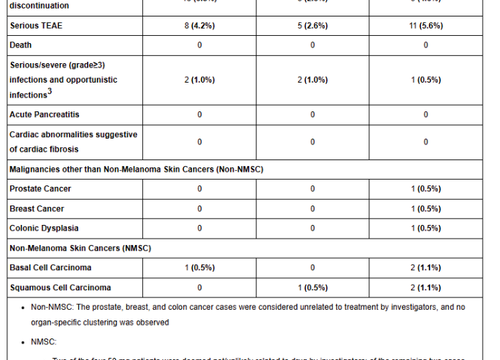

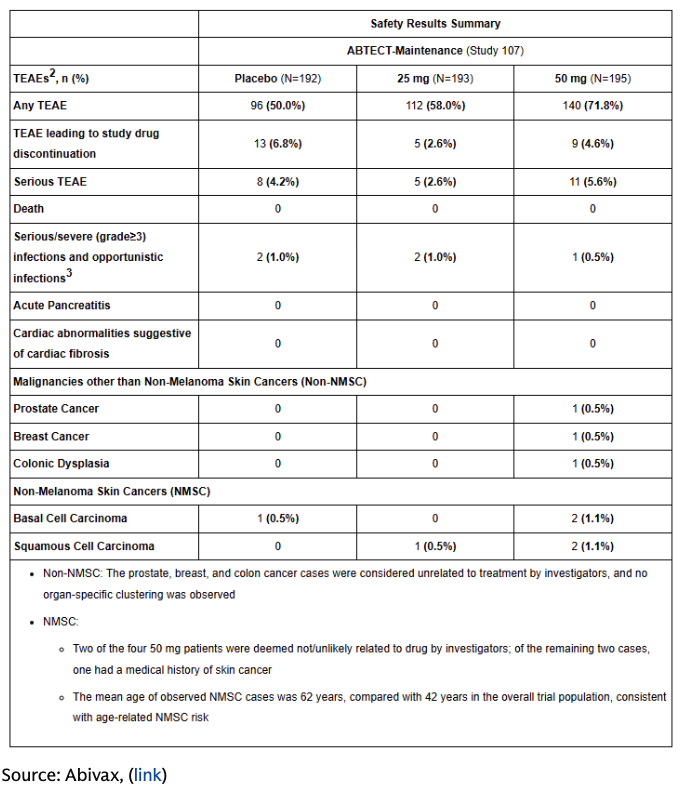

Though no new safety signals were observed per the press release, the safety results summary table (below) indicated 8 cases of malignancy, which spooked the market. Note, a number of investors are in this name for the M&A takeout story which could be muddied on this update. Mgmt did host a call on the results in which they did suggest the malignancies observed do align with background rates in UC (e.g. here for basal cell carcinoma), and weren’t considered a new safety signal by monitoring committees. Wonder if this becomes a Fenebrutinib-like situation where market goes negative on headline safety imbalance, those are explained away as non-treatment linked at a detailed presentation and docs come out in support of the drug, and we see a re-rating.

The pushback this morning is that pharma BD teams are now unlikely to take on the risk here – and that this is now a solid solo story with fair value likely still in the $100+ region, and so there is upside out of today’s levels but in fairness, not many (visible) catalysts to realise it – CD data in mid-27. And we are in a challenging biotech tape as it is, with SMMT -10% yday on myopic focus around >65 age subgroup, despite mgmt assuring this was due to baseline imbalances (which had been addressed at 2025 ESMO too, no less) and after adjusting for these, PFS HR would’ve been an in-line 0.69, not 0.88 (note).

In a separate note, Jefferies analysts stated, “The cancer signal complicates matters. Even if it is unrelated noise, we think the overhang will be real, especially considering the absence of other value-inflecting data events over the next year.“

They noted that “a reasonable explanation” for the cancer cases was plausible, but “it doesn’t seem like an easily dismissed overhang.” This prompted the analysts to downgrade the stock from a “Buy” rating to “Hold.”

Abivax shares in Paris crashed 31.4%, exceeding the 31.03% drop on June 6, 2016.

All gains for 2026 were wiped out.

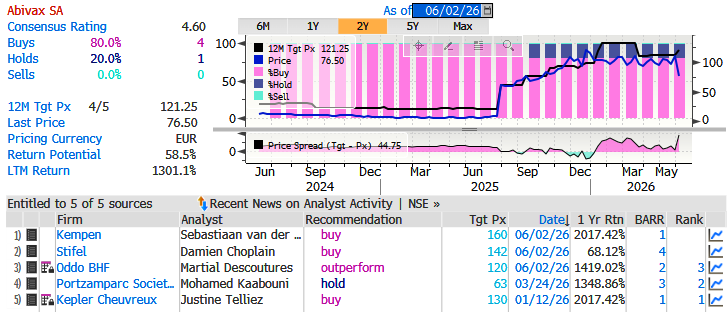

Analysts tracked by Bloomberg were overwhelmingly bullish, with 4 “Buy” ratings, 1 “Hold,” and 0 “Sells.”

“While the malignancy signal cannot be ignored, we view it as a potential labeling overhang rather than evidence of a clear causal safety risk,” Stifel analyst Damien Choplain told clients.

CNBC noted, “Abivax has been positioned as a prime takeover target, with unconfirmed rumors that big pharma has its eyes on the clinical-stage biotech led by CEO Marc de Garidel.”

The key question now is whether Abivax remains a “prime” takeover target after the cancer overhang complicated what had been a clean M&A story in the rumor mill.

Tyler Durden

Tue, 06/02/2026 – 07:45

{kind=link}

{kind=link}

{kind=link}

{kind=link}