Saylor’s Strategy Buys The Dip As Bitcoin Nears Mining Cost Floor

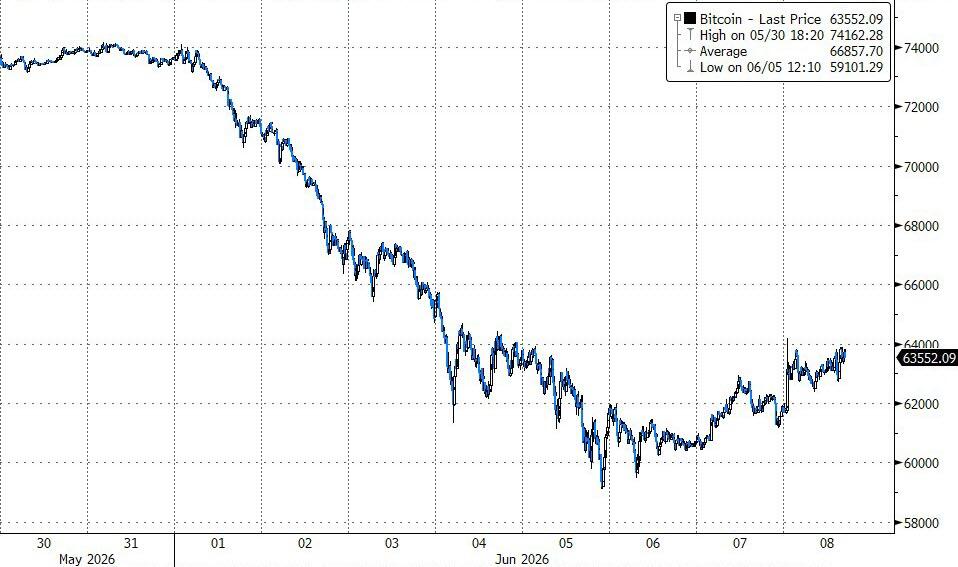

A week after SELLING 32 Bitcoin – and (in part) triggering a waterfall decline in crypto – Bitcoin treasury company Strategy just BOUGHT an additional 1,550 BTC for approximately $101.3 million at an average price of $65,332 per bitcoin between June 1 and June 7, according to an 8-K filing with the SEC on Monday.

Strategy now holds a total of 845,256 BTC – worth around $53.5 billion – bought at an average price of $75,680 per bitcoin for a total cost of around $64 billion, including fees and expenses, according to the company’s co-founder and executive chairman, Michael Saylor.

{kind=link}

This means Saylor’s horde represents 4% of bitcoin’s 21 million supply cap.

Was Saylor’s ‘sale’ last week designed to lower the price for this big purchase?

Bitcoin had been trading for around $73,700 before the sale announcement.

However, the news, despite increasingly being flagged by the company as a possibility in recent weeks, saw the market subsequently drop around 20% to a low of roughly $59,300 on Friday, before recovering back above the $63,000 level over the weekend.

{kind=link}

Last week, JPMorgan analysts said Strategy’s recent decision to sell 32 BTC “spooked” markets even if the sale was “symbolic and voluntary,” intended to demonstrate the company’s commitment and flexibility to preferred stockholders.

As TheBlock.co reports, Saylor posted another Strategy bitcoin acquisition tracker chart on Sunday with the caption “A good time to add more dots,” a commonly-understood signal that the largest corporate bitcoin holder may disclose fresh bitcoin purchases this week.

{kind=link}

The framing this time went further than the usual nod toward another buy, in that it explicitly positioned current price levels as attractive, with bitcoin trading in the low $60,000 range.

Following bitcoin’s worst week in two years, Strategy(MSTR) Executive Chairman Michael Saylor published a framework on X, arguing that the Bitcoin community is evolving into four distinct ideological camps.

{kind=link}

As CoinDesk reports, rather than viewing these groups as competitors, he presents them as complementary forces that will collectively shape bitcoin’s future.

The first group, Bitcoin Maximalists, sees Bitcoin as the ultimate monetary breakthrough. They believe bitcoin has already solved the problem of digital scarcity and offers superior property rights, protection from inflation, and economic empowerment. Their focus is conviction: bitcoin is not one crypto asset among many, but the dominant digital monetary network.

The second group, Bitcoin Capitalists, views Bitcoin as a form of digital capital that should be integrated into the global economy. They support corporate treasury adoption, institutional custody, bitcoin-backed securities, lending markets, and broader financial infrastructure. Their goal is to expand bitcoin’s reach by embedding it into existing economic systems rather than replacing them.

The third group, Bitcoin Technologists, focuses on improving the protocol. They argue that Bitcoin must continue to evolve to address challenges in scalability, privacy, usability, security, and future threats such as quantum computing. While they support innovation, Saylor notes that changes to bitcoin’s base layer must be approached cautiously to avoid unintended consequences.

The fourth group, Bitcoin Fundamentalists, prioritize protecting bitcoin’s original principles: decentralization, self-custody, immutability, censorship resistance, and individual sovereignty. They are wary of excessive institutional influence, financialization, and protocol changes that could compromise Bitcoin’s core characteristics.

Saylor’s central argument is that Bitcoin needs all four perspectives. Maximalists provide conviction, Capitalists drive adoption, Technologists ensure long-term resilience, and Fundamentalists safeguard the protocol’s integrity.

Saylor argues that Bitcoin’s most successful path lies in a balance among these four forces.

The piece was published as observers debated whether Strategy’s June 1 disclosure had itself contributed to the latest leg lower.

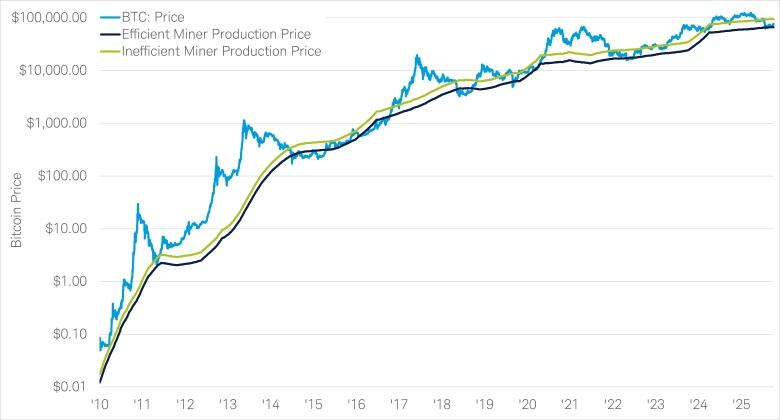

That bitcoin is in a bear market is not in dispute, but as BitcoinMagazine.com reports, Jim Ferraioli, Director of Digital Currencies Research and Strategy at Charles Schwab, argued last week on Bloomberg that this selloff has a measurable cost floor, and that floor is built not from sentiment or chart patterns, but from the physics of energy consumption.

{kind=link}

The numbers frame the drawdown in context. Bitcoin peaked at $126,000 in the fall before collapsing to roughly $60,000 in February — a 50% correction that, while brutal for recent buyers, falls far short of the 75%-plus implosions that defined prior Bitcoin bear markets.

Ferraioli’s core analytical framework centers on one question: what does it cost to manufacture Bitcoin? The answer creates a natural gravitational floor that has held across multiple cycles.

{kind=link}

For the most efficient miners — those operating at scale with next-generation ASIC hardware and access to the cheapest wholesale energy — the cost to produce one Bitcoin sits at approximately $60,000, Ferraioli said.

That figure is not arbitrary. It represents the all-in expense of powering a facility at roughly $0.07 per kilowatt-hour with the most advanced semiconductor fleets available.

The less efficient miners — those with older ASIC hardware, higher energy costs, and thinner operational margins — carry a production cost of approximately $95,000 per BTC, according to Glassnode data cited in Schwab’s May 2026 research report. That gap between $60,000 and $95,000 defines Bitcoin’s current valuation range.

Bitcoin’s energy floor: Why $60,000 may mark the bottom

Ferraioli argues that in deep bear markets, the cost of production for the best miners has historically served as the bottom. February’s low near $60,000 aligns almost precisely with that level, as well as BTC’s 200-week moving average.

The BTC selling pressure is not random. It is demographically specific. The investors driving forced liquidations are those who acquired Bitcoin during the past 18 months — buyers who rode the asset from sub-$80,000 up to $126,000 and then watched gains evaporate in full.

Schwab tracks two cost-basis metrics to quantify this pressure: the average acquisition cost for U.S. spot ETF and ETP holders, which stands near $83,000, and the active investor cost basis — excluding coins rewarded to miners — which sits near $78,000.

Both figures sit well above current spot prices, putting the majority of recent entrants into unrealized loss positions and reinforcing $83,000 as a ceiling of overhead supply rather than a floor of support.

Glassnode’s on-chain data corroborates this dynamic. Bitcoin’s latest attempted rally stalled at the aggregate ETF cost basis near $83,000, with total realized losses spiking to $1.35 billion per day and long-term holders capitulating from cycle-top positions. Hedge funds represent roughly 30% of spot ETP ownership but are operating market-neutral, executing basis trades rather than taking directional views — meaning they provide no natural bid when prices fall.

Here is where Ferraioli’s analysis turns constructive. Every major publicly traded Bitcoin miner has announced a pivot toward high-performance computing (HPC) for AI inference workloads. The economics on their face appear to favor abandoning mining: inference generates higher net revenue per megawatt-hour than Bitcoin mining during peak demand windows.

But demand for AI inference is not uniform across 24 hours. Models run hard during business hours and sit idle overnight and on weekends.

That creates a structural opportunity that does not displace BTC mining — it layers on top of it. Schwab’s analysis models Bitcoin as the optimal baseload monetization of power during off-peak hours, with inference overlaid during peak business-hour demand.

A data center operating this hybrid model maximizes utilization across the full 24-hour cycle rather than leaving capacity dark when inference demand falls away. For miners, this translates to more stable revenue, reduced forced BTC sales to cover operating costs, and lower structural risk across bear market cycles.

Bitcoin is backed by energy

The underlying thesis is one of energy economics. Bitcoin has no earnings, no free cash flow, and no CEO issuing guidance. Its value, in Ferraioli’s framework, derives from the energy cost required to produce it — a cost that is transparent, verifiable, and historically durable.

In commodity markets, price cannot sustainably trade below cost of production. Producers shut down, supply contracts, and equilibrium resets higher.

Bitcoin follows this same logic: when spot prices fall toward $60,000, the least efficient miners shut down operations, the network’s hash rate adjusts through Bitcoin’s difficulty mechanism, and the cost to produce each new coin falls.

As of May 2026, the average mining cost across all Bitcoin miners sits near $85,604, with the Bitcoin price trading in the mid-$60,000s — meaning the network as a whole is operating at a loss, a configuration that has historically preceded recoveries, not further collapse.

Tyler Durden

Mon, 06/08/2026 – 11:05

https://www.zerohedge.com/crypto/saylors-strategy-buys-dip-bitcoin-nears-mining-cost-floor