Futures Rise As Tech Rebound Extends While Oil Drops

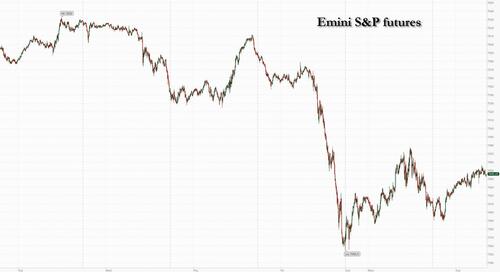

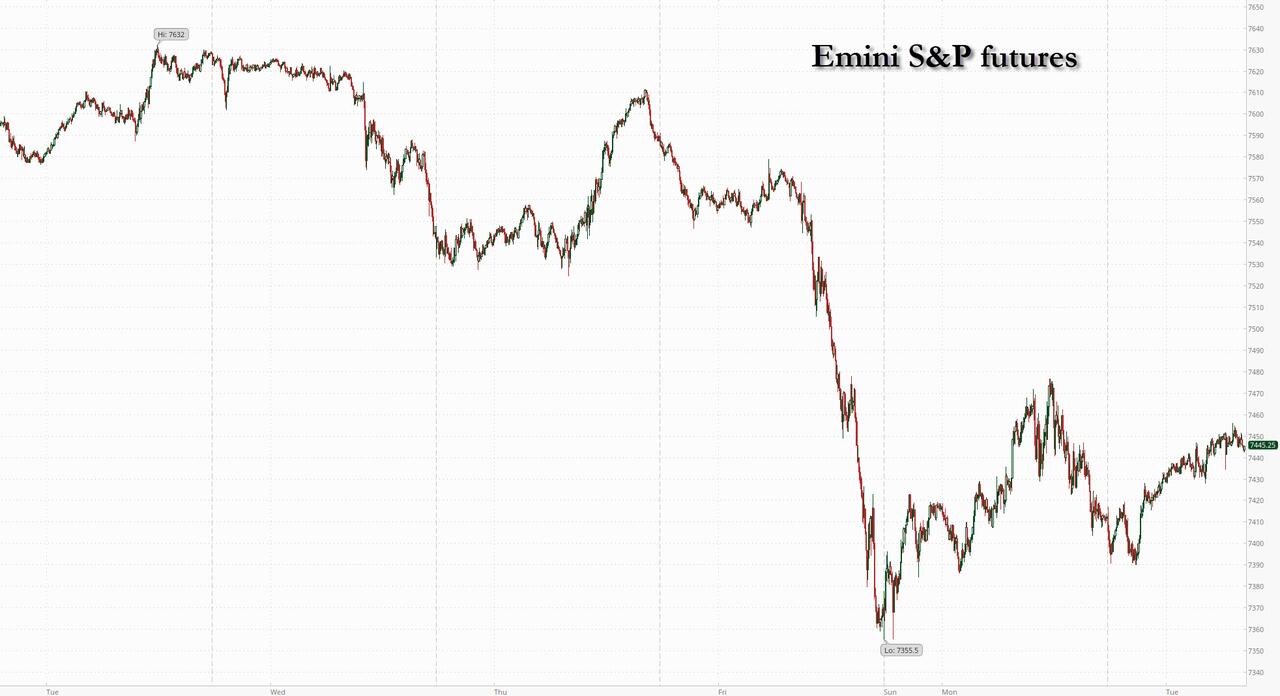

US equity futures are higher as Monday’s US stock gains extend into today’s trading with both tech and small caps outperforming as the AI theme resumes its global surge and US/Iran deal optimism is back (on the back of the now daily optimistic comments from Trump) broadening the rally. As of 8:00am ET, tech enthusiasm is on display with Nasdaq 100 futures up 0.8% as chipmakers including Marvell Technology Inc. and Micron Technology Inc. posted strong premarket gains, while S&P500 futures gain 0.4%. In premarket trading, Mag7 names are mostly higher; cyclicals ex-energy are leading defensives ex-HC. A similar theme played out in APAC, with the tech-laden Kospi soaring 8.2%. Europe’s Stoxx 600 is rising alongside weaker energy prices with gains driven by financials and consumer names. Oil dipped after Trump said a framework of deal “within the next 2 days,” though it is unclear what has changed from previous claims over the last 2 months. Commodities are reacting to headline risk with Brent down 2.1% as Israel and Iran halt attacks and Chinese oil imports declined, and WTI below $90/bbl. The downside in energy prices has provided a mild support for global fixed income markets, with US yields 1-2bps lower across the curve ahead of the US 3-year note auction. The Bloomberg Dollar Spot index is down 0.2%. Downside in USD/JPY from a report that the BOJ could hike in June and October proved fleeting. Precious metals are steady. Bitcoin sheds 1.3%. The macro data focus will be on weekly ADP, the NFIB Small Biz Survey where the Hiring sub-index may give add’l evidence for the labor market acceleration. Keep an eye on the 3Y bond auction today

{kind=link}

In premarket trading, Mag 7 stocks are mostly higher (Nvidia +0.4%, Amazon +0.6%, Meta +1.1%, Alphabet +0.6%, Tesla +0.6%, Apple -0.4%, Microsoft -0.3%).

Chipmakers, opticals and storage firms rise, on track to extend gains, as the group rebounds in the wake of Friday’s sharp selloff.

Lithium stocks rise as Citi remains bullish on the metal, seeing a recovery in prices after the recent selloff.

Applied Digital (APLD) is up 11% after the neocloud company said it signed a 15-year take-or-pay lease with a US-based artificial intelligence hyperscaler, for 210 megawatts of critical IT load at its Delta Forge 2 campus.

CECO Environmental Corp. (CECO) gains 13% as the manufacturer of water treatment equipment updated its full year outlook after closing Thermon Group Holdings acquisition.

GDS Holdings ADRS (GDS) rise along with other Chinese cloud providers as people familiar with the matter said that China is preparing to spend around $295 billion over the next five years to build data centers across the country.

Mission Produce (AVO) falls 2% after the avocado supplier reported adjusted earnings per share for the second quarter that missed the average analyst estimate.

Nuvalent (NUVL) is up 39% after GSK agreed to acquire the company for $10.6 billion. The transaction will accelerate GSK’s entry into the lung cancer space and could help offset the looming patent expiry of its HIV drug dolutegravir, Barclays analyst James Gordon wrote in a note.

Perrigo (PRGO) slips 1% after the company’s CEO Patrick Lockwood-Taylor resigned from both roles and from the board, following a determination that certain personal conduct was inconsistent with the company’s code of conduct and core values.

SailPoint (SAIL) falls 13% after the software company’s quarterly results and outlook isn’t enough to extend recent strength in the stock, which is up nearly 70% off an April low as of last close.

Vail Resorts (MTN) is down 4% after the ski resort operator cut its net income guidance for the full year, attributing the reduction to “historically challenging” weather conditions in the western US.

In other corporate news, executives overseeing Oatly’s Chinese operations are said to be considering buying out the business. Apple’s iOS 27 and related software updates offer signs the of the company’s upcoming foldable iPhone. GSK agreed to buy clinical-stage biopharmaceutical company Nuvalent in a deal valued at $10.6 billion to expand in oncology treatments.

After a brief pause in the rally that propelled equities to record highs, traders are returning on expectations that corporate profits will give stocks further room to run. OpenAI’s confidential filing for an initial public offering and the oversubscription of SpaceX’s share sale served as reminders of the vast demand for AI – before attention turns to Wednesday’s CPI print. Overnight sentiment was also boosted from lower energy costs, with Brent sliding 1.5% to below $93 a barrel. Israel and Iran agreed to end their tit-for-tat attacks, while President Donald Trump renewed his claims that a US peace deal with Tehran was nearly done.

From SpaceX’s IPO being oversubscribed ahead of books closing late Wednesday, to OpenAI filing confidentially for an IPO and said to be planning a tender sale of its shares to provide liquidity to employees, “there’s a real race for capital that’s going on,” notes CPR Asset Management’s Julien Daire, perhaps to get ahead of the moment of realization that much of this SPV chip-backed rollout is funded by American retirees putting their money in “safe” annuities.

And the biggest investor: unwitting retirees through “safe” annuities purchased from Apollo’s Athene insurance company https://t.co/UhtWzj59ia

— zerohedge (@zerohedge) June 9, 2026

Meanwhile in China, the country plans to spend around $295 billion to fund a nationwide AI buildout of data centers, signaling its ambition to propel the domestic AI sector and rely on local suppliers for at least 80% of technology such as AI chips.

And speaking of China, the AI supercycle showed up in macro data overnight as well, with Beijing’s export sales of semiconductors soaring 111% year-on-year in May, the fastest expansion since 2013. Elsewhere, the massive PJM power grid region is expected to see a 26-fold increase in energy storage over the next decade on the back of data-center driven load growth and lagging supply strain reliability and affordability.

There are red flags: bond-yield levels don’t look encouraging for stocks, but it will likely take greater rate volatility to trigger another leg lower, according to Bloomberg Senior Strategist Michael Msika. Risks are mounting into a tricky June, but portfolio rotation seems to be the preferred approach, rather than cutting exposure altogether. The bond market is running ahead of the Fed policy rate, with a clear message for Kevin Warsh that rates need to be higher, and prompted Citi to lower its short-term price target for gold.

While AI “has driven a strong rally so far, it also carries a high risk of pullbacks, which are bound to occur given the dynamic nature of the sector’s development,” said Guillermo Hernandez Sampere, head of trading at MPPM.

Warnings that a push higher in stocks could prove choppy still abound. Citigroup Inc. strategists said traders are aggressively building short-selling positions in US equities, while bullish wagers on the tech sector remained stretched. Friday’s near 5% selloff in the Nasdaq 100 has only partially reset exposure among investors, the Citi team led by David Chew noted.

The next few weeks hold major risk events, with inflation data due Wednesday and the first Federal Reserve interest-rate decision under Chairman Kevin Warsh on June 17.

“If inflationary risks continue to rise, a more aggressive repricing of the Fed could easily challenge current valuations and derail equity markets,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin.

In politics, the race for California governor is on track for a two-person runoff in November between veteran Democratic politician Xavier Becerra and Republican Steve Hilton, a British-born television personality endorsed by President Trump. The Pentagon has accused some of China’s biggest companies of supporting the Chinese military, including Alibaba, Baidu and BYD.

In Europe, the Stoxx 600 is rising alongside weaker energy prices with gains driven by financials and consumer names. Health care stocks were dragged lower by GSK, which shed as much as 3.9% after announcing it would acquire US firm Nuvalent for $10.6 billion. The energy subindex was the biggest laggard as Brent crude dropped below $93 a barrel. Here are the biggest movers Tuesday:

Demant advances as much as 5%, to the highest since August 2025, after a BofA double-upgrade to buy removes the only negative analyst rating on the hearing aids manufacturer

Givaudan rises as much as 5.9%, the most in almost two months and taking the stock to the highest since late February, as Deutsche Bank upgrades the Swiss fragrance and flavor maker to buy and JPMorgan adds a positive catalyst watch

WPP leads European advertising firms higher after Berenberg said the sector is poised for a rerating because investors have overestimated the threat posed by artificial intelligence. Analysts initiated coverage of WPP, Publicis Groupe and Havas with buy ratings

Seraphim Space Investment Trust shares rise as much as 26%, their biggest jump in almost three years, after the fund said the fair value of Iceye, its largest holding, had doubled after a funding round

Breedon Group shares gain as much as 6.6%, the largest intra-day rise in two months, after the building materials supplier announced the $120 million acquisition of a limestone quarry near Missouri

Fever-Tree shares rise as much 8.2% to the highest in a month after the company said it was on track to meet expectations and extended its buyback program

El.En. shares climb as much as 6.3% to the highest since November 2021, after Stifel initiated the laser equipment firm with a buy rating, predicting profits to more than double over the next five years

GSK shares slip as much as 3.9% as Barclays analysts noted the British drugmaker will gain access to two experimental medicines in late-stage trials through its planned purchase of Nuvalent, but that upside is capped

K+S shares fall as much as 5.6% to their lowest since January as the German agricultural chemicals firm launches an offering of convertible bonds worth around €300 million to finance the previously-announced purchase of Qemetica’s salt business

Trigano shares drop as much as 7.5%, the most in over nine months, after analysts at Oddo BHF cut their price target on the maker of recreational vehicles and removed it from their list of top picks within the European mid-cap space

Rusta falls as much as 7.7% after the Swedish discount retailer reported its latest earnings. DNB Carnegie says the print shows a weaker-than-expected end to 2025/2026, with added headwinds from “very tough” comparables

Asian stocks rose, as bargain hunters dipped back in to buy technology stocks after a sharp selloff. The MSCI Asia Pacific Index climbed as much as 2.8%, on track to snap a three-day losing streak. The information technology sector led gains among sub-indexes, with SK Hynix and Samsung Electronics contributing the most to the advance. South Korea and Indonesia led the region’s rebound, just a day after ranking among the worst performers. The rally follows a steep pullback triggered by concerns over overheating in artificial intelligence stocks. While broader concerns about the sector’s momentum remain, the recent drop has made valuations more appealing and steady earnings are helping to support sentiment. Easing tensions in the Middle East added to the positive tone, after Iran and Israel agreed to scale back strikes following a flare-up that had threatened to derail peace efforts and drew calls for de-escalation from President Donald Trump.

In FX, the dollar headed for its biggest two-day retreat in a month. Indonesia’s central bank raised its benchmark rate ahead of its next scheduled meeting to reverse a market selloff and support the rupiah.

In rates, treasuries rose modestly as traders dialed back bets on US interest-rate hikes, led by short-dated notes as oil continued its decline after Israel and Iran agreed to stop attacks, following a flare-up in violence. US yields are richer by up to 2.5bp across front end of the curve with long end richer by around 1bp, steepening 2s10s and 5s30s spreads by 1bp and 1.5bp vs. Monday close. US 10-year yields trade around 4.545%, down 1.5bp on the day with bunds lagging by 1.5bp in the sector, gilts slightly outperforming. Bull steepening move comes ahead of this week’s first Treasury auction of $58 billion 3-year notes at 1pm New York. Treasury auction cycle resumes at 1pm New York with $58 billion 3-year notes, before $39 billion 10-year and $22 billion 30-year reopenings Wednesday and Thursday. The WI 3-year trading around 4.205% is 24bp cheaper than the May stop-out, which tailed the WI by 0.6bp.

In commodities, Brent has continued to slip, down 2.1% as Israel and Iran halt attacks and Chinese oil imports declined. Bitcoin sheds 1.3%. Precious metals are steady. Gold held steady near $4,340 an ounce. The appeal of the precious metal has steadily faded from a peak above $5,400 in January after the war in the Middle East upended expectations for US monetary policy, shifting bets from rate cuts to possible hikes.

Today’s US economic data calendar includes ADP weekly employment change (8:15am), April trade balance (8:30am), May existing home sales, April wholesale inventories (10am)

Market Snapshot

{kind=link}

Top Overnight News

President Trump asked Prime Minister Benjamin Netanyahu of Israel to pull back from escalating his country’s strikes against Iran during a call on Monday morning, telling the Israeli leader that the United States and Iran were within days of a breakthrough clearing the way for talks on a long-term nuclear deal. NYT

Trump Says Peace Talks on Track After Israel-Iran Clash Ends: BBG

USTR Greer said to be heading to Silicon Valley to promote onshoring this week: Semafor

China’s exports surged last month on demand for AI-related goods as the world’s second-largest economy shook off the impact of energy shortages from the Middle East. Exports expanded 19.4 per cent in May on a year earlier in dollar terms, exceeding expectations. FT

A sharp fall in China’s oil imports is keeping global prices in check despite a supply crunch lasting more than 100 days due to disruptions in the Strait of Hormuz. China’s int’l oil purchases fell to the lowest level in more than 8 years in May. Nikkei

The BoJ will consider maintaining the current pace of bond purchases beyond next fiscal year, sources said, pausing a taper process that would mark a turning point in its quantitative tightening (QT) plan. But the decision could be a close call as the nine-member board is seen as split between those who want to focus on soothing investor nerves and others who see the need to steadily slow purchases to reduce the BOJ’s large balance sheet. RTRS

Japanese policymakers said on Tuesday they stood ready to act decisively against excessive yen falls while remaining vigilant to rising bond yields that could hurt the economy, highlighting the dilemma they faced in countering unfavorable market moves. RTRS

German industrial production grew for the first time since war broke out in Iran, fueling hope that Europe’s largest economy is weathering the jump in energy costs. Output increased 0.4% in April from the previous month, driven mainly by construction. BBG

China is preparing to spend around 2 trillion yuan ($295 billion) over the next five years on building data centers across the country, fueling Beijing’s ambition to propel the domestic AI sector and surpass the US in a potentially game-changing technology. BBG

The $31 trillion Treasury market has an unequivocal message for Kevin Warsh’s Fed: Interest rates aren’t high enough. Yields on two-year notes hovered near their highest level in more than a year. BBG

An index of US small business optimism fell last month to the lowest level since October 2024, erasing almost all of the gains seen since Trump was elected for a second term. BBG

A more detailed look at global markets courtesy of newsquawk

APAC stocks traded somewhat mixed, albeit with a mostly positive bias as indices rebounded from yesterday’s losses, with sentiment helped by Israel and Iran halting their strikes, while participants also reflected on the better-than-expected Chinese trade data. ASX 200 declined as the prior day’s losses caught up with the index on return from a long weekend. Nikkei 225 fluctuated and briefly wiped out all its opening gains before rebounding to print fresh intraday highs. Hang Seng and Shanghai Comp were mixed with the mainland kept afloat following the stronger-than-expected Chinese trade data, although gains were capped after the US Pentagon posted a list of Chinese military companies, which included Alibaba, Baidu, BYD, Tencent, NIO and Cosco among others.

Top Asian News

Chinese Balance of Trade (USD)(May) 105.4B vs. Exp. 91.5B (Prev. 84.8B).

Chinese Exports YY (May) 19.4% vs. Exp. 14.3% (Prev. 14.1%).

Chinese Imports YY (May) 27.4% vs. Exp. 25% (Prev. 25.3%).

Taiwan Balance of Trade (May) 17.91B vs. Exp. 15.2B (Prev. 14.35B).

Taiwan Exports YoY (May) Y/Y 51.7% vs. Exp. 37.9% (Prev. 39%).

Taiwan Imports YoY (May) Y/Y 54.90% vs. Exp. 37.4% (Prev. 29.2%).

Australian Westpac Consumer Confidence Index (Jun) 80.6 (Prev. 83).

Australian Westpac Consumer Confidence Change MM (Jun) -2.9% (Prev. 3.5%).

Australian NAB Business Confidence (May) -14 (Prev. -24).

Australian NAB Business Conditions (May) 3 (Prev. 3).

European bourses (STOXX 600 +0.5%) start Tuesday’s trade on a positive footing with geopolitical updates quiet. FTSE MIB (+1.6%) is the clear outperformer helped by gains in Banks, while FTSE 100 (-0.3%) is the only index in the red as miners and healthcare giants fall. European sectors hold a positive bias. Insurance (+1.3%) tops the pile, with Retail (+1.0%) and Banks (+1.2%) rounding out the top 3. To the downside are Basic Resources (-0.3%), Health Care (-0.5%) and Energy (-0.4%).

Top European News

CBI warned around 200k more Britons are on track to become unemployed, with unemployment forecast to rise to 5.5% this year, while it cut UK GDP growth forecasts to 1.1% in 2026 and 0.9% in 2027 from prior expectations of 1.3% and 1.5%, respectively.

No breakthrough in discussions on finalising the Defence Investment Plan on Monday but it could still come this week, POLITICO reported citing sources.

FX

G10s are nearly entirely firmer against a modestly softer Buck, which remains towards recent post-NFP highs. Kiwi and sterling outperform, NOK is the laggard with Brent Aug’26 -1.5%.

USD a touch lower and well within post-payrolls ranges. The general risk environment has improved since Friday’s strong Payrolls, and Monday’s bid in crude. Overnight saw Kospi rise near 8%, optimism which has travelled through to European hours with bourses/US futures firm. The next inflection point, aside from geopolitics, will likely be US CPI and PPI on Wednesday and Thursday, respectively. Today sees the release of NFIB small business optimism data, weekly ADP jobs, and Trade metrics. Technicals, to the upside is the 100 mark, where DXY typically loses steam, and downside is 99.80 which provided support on Monday.

GBP is one of the best G10 performers. A strong BRC retail sales showed consumer spending had steadied from a weak April figure with food and non-food sales accelerating sharply in May. Pantheon Macro estimates the BRC survey in isolation is consistent with a 0.6% month-to-month rise in official retail sales volumes in May. Cable took a hit on Friday’s Payrolls and continues to trade below levels seen before the data (c. 50pips), carry remains in focus into the slew of Central Bank meetings this, and next week. BoE pricing steady, still only pricing one full hike this year (c. 45bps by year-end), consistent with recent levels.

Antipodeans outperforming with Kiwi benefitting to a greater extent after strong Chinese trade data beat expectations across the board thanks to robust tech-related Imports and Exports. Australian NAB business confidence was out overnight, remaining negative though faring better than April’s figure. AUD/NZD dipped from a 1.2136 peak, to mark a session trough of 1.2083, AUD/USD +0.1%, NZD/USD +0.3%.

Fixed Income

Global fixed benchmarks are mildly firmer this morning, benefiting from lower energy prices as recent geopolitical tensions ease for the time being. In brief, Israel and Iran have agreed to halt their strikes, though recent reports have suggested that Southern Lebanon remains under fire. Trump has continued to talk up the mood, stating that a total victory will be declared in two weeks. For reference, this marks the 37th time he has suggested that a deal is imminent, CNN reported.

USTs (+2 ticks) are slightly firmer and trade within a 108-27+ to 109-03 range. As above, action is facilitated by lower energy prices, but with trade tentative amidst the uncertain environment. Also clouding the picture is the hawkish economic picture, with the recent NFP report pointing towards a solid labour market. US CPI and PPI (Wed/Thu) will play key roles for policymakers heading into next week’s policy decision. As for today, traders will digest US ADP Weekly Change, Exports/Imports, Atlanta Fed GDP, and Wholesale Inventories (Apr).

Bunds (+10 ticks) and Gilts (+15 ticks) also trade modestly higher, but with price action rangebound. In Germany, Industrial Production increased from the prior, but still remains at low levels; trade data displayed a mixed picture.

Over in the UK, BRC Retail Sales in May topped expectations (3.4% vs exp. 0.6%), indicating that consumers have remained resilient despite the Iran conflict; though, some of that spending may be related to the good weather experienced in the region. As for politics, UK PM candidate Burnham is reportedly poised to delay any Labour leadership bid until after the battle to retain the Greater Manchester mayoralty. Gilts trade in a 87.53 to 87.69 range.

Germany sells EUR 1.756bln vs exp. EUR 2.0bln 1.80% 2053, 2.50% 2035 and 2.30% 2033 Green Bund.

The Netherlands sells EUR 2.5bln vs exp. 2.5bln 2.50% 2035 DSL: Average yield 3.102% (prev. 2.810%).

Commodities

Crude futures are softer, continuing from Monday’s afternoon sell-off, as Israel and Iran seemingly hold onto their promises to halt attacks on each other. Despite this, there have been reports of strikes in Lebanon but benchmarks were unreactive. Late in Monday’s session, Axios reported that in a call with Israeli PM Netanyahu, US President Trump warned that if the Israeli leader went back to war with Iran, he might be fighting alone. Further on the US-Iran deal, CNN reported, citing a top Iranian official, said a deal being imminently reached is doubtful due to persistence of major roadblocks regarding Iran’s nuclear programme and uranium enrichment. However, these reports have failed to damper the risk tone. WTI Jul trades at the lower end of a USD 88.80-91.55/bbl range while Brent Aug hovers around the USD 92.00/bbl mark (USD 92.00-94.42/bbl).

Precious metals have steadied since Friday’s selloff, with spot gold hovering above the USD 4300/oz handle (USD 4313-4352/oz). Spot silver has regained the 200-SMA, trading at the upper end of its USD 67.46-68.86/oz range.

3M LME Copper gains, along with the broader base metal space, amid the positive risk tone. The red metal trades at the top end of its USD 13.55k-13.77k/t range.

Vale said it has not seen any significant destruction in global metals demand from the Iran conflict, with strong demand for critical minerals and tighter raw material flows helping support commodity prices and margins.

Trade/Tariffs

US asked China to resume rare earth exports to Japan, with Washington concerned regarding impacts on global high-tech supply chains, according to Nikkei.

China Foreign Ministry, on the US adding Chinese firms to Pentagon list, said China always opposes US overgeneralising the concept of national security.

Central Banks

BoJ is reportedly prepared to raise rates by 25bps at its June meeting, Nikkei reported. The hike is to prepare for the risk of an upward revision of inflation. Also, to begin discussions around the discontinuation of its quarterly reduction in government bond purchases from April 2027 onwards.

Geopolitics: Iran

US President Trump said they are negotiating regarding Iran and a victory will happen very soon, while he stated they will declare total victory in two weeks and oil prices will come down post-Iran. Trump separately commented that he could have an idea on an Iran deal in one or two days, and stated the blockade continues to hold, as well as stated that they are very close to having a good, strong, powerful deal. On the Iran-Israel front, he said that Israel and Iran agreed to leave each other alone for another week.

US VP Vance said a potential Iran deal will be a home run for the American people and that the US will need to verify over the long-term that Iran is living up to the agreement, while he also stated that the US’s interest lies in a deal with Iran, whether Israel likes it or not. Vance also commented that the primary goal is to prevent Iran from acquiring a nuclear weapon, and stated that a military option is not ruled out if diplomacy with Iran fails.

Iran’s UN envoy hopes for US-Iran talks conclusion by the end of June, and stated the US and Iran are exchanging views via Pakistan.

Iranian official said no agreement can be reached unless its frozen funds are released and sanctions are lifted, while the official added that Washington made changes to the draft MoU and that this was unacceptable, according to Al Jazeera. It was separately reported that a top Iranian official casted doubt on a deal being imminently reached between the US and Iran, while the official said major roadblocks persist on issues like Iran’s nuclear program and uranium enrichment.

Iranian Parliament member said that if Israel attacks Lebanon or Iranian soil, then both Israel and US military bases will be legitimate targets.

A military source familiar with the Houthis suggest that they are “preparing major military surprises, and that the weapons that will be used in the naval or aerial conflict will be of high quality”, Kan’s Kais reported.

Two new airstrikes have reportedly been undertaken by Israel, targeting Southern Lebanon, Tehran Times reported.

Tasnim news agency reported air raids by Israel on two settlements in the city of Tyre in southern Lebanon.IRNA reported continuation of attacks by Israeli regime on southern Lebanon.

Geopolitics: Ukraine

Russia’s Deputy Foreign Minister said Russia and Belarus are constantly ready to use all available means, including nuclear, to ensure security, according to an interview with Izvestia newspaper.

Drone strike reportedly hit Sevastopol in Russian-annexed Crimea.

US Event Calendar

6:00 am: May NFIB Small Business Optimism, est. 96, prior 95.9

8:30 am: Apr Trade Balance, est. -56.1b, prior -60.3b

10:00 am: May Existing Home Sales, est. 4.07m, prior 4.02m

10:00 am: Apr F Wholesale Inventories MoM, est. 0.55%, prior 0.5%

DB’s Jim Reid concludes the overnight wrap

Morning from Istanbul. Please don’t tell my wife, but this extraordinary city was the backdrop to the greatest night of my life some five years before I met her. Even now, the memory is vivid of that special night of passion. The heat. The noise. The sweat. A pounding heart and hours of emotional turbulence. By late evening it felt inevitable that it simply wasn’t going to happen, and that I’d leave exhausted, disappointed and slightly broken. Then, just after midnight, against all logic and expectation, came a sudden, frantic and utterly euphoric release. Yes after being 3-0 down at half-time, the “Miracle of Istanbul” arrived and Liverpool fought back and ultimately won the penalty shoot out and, with it, the Champions League back in 2005. A night I will never forget but with the way Liverpool played this past season I’m not sure when that will be next repeated.

Talking of repeats, it seems the cycle of “near a deal, not near a deal, escalation, de escalation, maybe back near a deal” continues. However for now we’re back in the “a deal is still possible” camp and in addition the AI trade has continued to bounce back this morning.

On that, the KOSPI (+7.35%) is sharply higher after its 9th worst day in 45 plus years of history yesterday (-8.29%). The Nikkei (+2.19%) is also benefiting from a recovery in technology stocks after a decline of over -3.5% yesterday. Chinese stocks are up just over half a percent and other markets are broadly flat. S&P 500 (+0.26%) and NASDAQ 100 (+0.54%) futures are also continuing to recover after a decent session yesterday.

As I’m typing this this morning, President Trump has been speaking to reporters and has said that they are “very close to having a good strong powerful deal” and that they “could have an idea on Iran in one or two days now”. Of course we’ve been here a few times before but the weekend stresses are fading back a little for now.

Indeed markets swung around yesterday as we faced an array of geopolitical headlines. Initially, it looked like another rough session, with Brent Crude up over +5% in the European morning amidst the strikes between Israel and Iran we discussed this time yesterday. However, the mood soon began to turn more positive, with President Trump calling on both sides to dial things down which to be fair he tried to do late in the weekend. Then late in the European morning session, Trump posted that “Both sides, Israel and Iran, are looking to do an immediate CEASEFIRE! Final negotiations on “Peace” are proceeding, subject to ignorance or stupidity getting in its way. The Blockade will remain in place, and in full force and effect, until a “Final Deal” is reached. Things should move quickly.”

That post from Trump led to an initial decline in oil prices, but the bigger move lower then came after Iran’s Fars said that the military operation against Israel had ended. Admittedly, they warned that further Israeli attacks would lead to “much harsher and more crushing actions than before”, but the end to the attacks was taken positively. Moreover, Israeli PM Netanyahu later said that Israel would hold fire in Iran for now. So it felt as though for the time being at least, the weekend flare-up in hostilities had been stopped, and there was still a path for peace talks to continue.

Given the end to the Israel-Iran strikes, Brent crude ultimately came down from an intraday peak above $98/bbl in the European morning, to $94.25/bbl by the close. Or in other words, it was only up +1.25% from its Friday close. That gap has narrowed further this morning with a -0.80% fall as I type.

Even with the pull back, concerns around inflation remained high yesterday, which cemented investor conviction that central banks would still be hiking rates in the coming months. Indeed for the Fed, markets raised the chance of a hike as soon as September to 53%, up from 44% on Friday. It’s ticked down to 50% this morning.

Given that backdrop, it was a tough session for sovereign bonds on both sides of the Atlantic. So Treasury yields rose across the curve, with the 2yr yield (+1.6bps) up to 4.16%, its highest since February 2025, while 10yr (+3.3bps to 4.56%) and 30yr yields (+4.0bps to 5.03%) saw larger increases. Notably, there were some big milestones for real yields, with the 10yr real yield (+3.7bps) closing at a one-year high of 2.20%. However, we didn’t have any Fed speakers as we’re now in the blackout period before next week’s meeting, so we don’t have much sense of how they’re thinking about the strong jobs report and whether it warrants a hawkish reaction.

Over in Europe it was a similar story, with yields on 10yr bunds (+2.2bps), OATs (+3.3bps) and BTPs (+3.4bps) all moving higher again. In fact, for 10yr OATs it took them up to a post-2009 high of 3.84%. And then in Germany, the 10yr real yield was at a 5-month high of 0.82%, despite some underwhelming data on factory orders, which showed a monthly decline of -3.8% in April (vs. -2.0% expected).

One relatively positive area yesterday was US equities, with the major indices stabilising after Friday’s slump. The recovery was particularly visible in segments that slumped the most on Friday, with the NASDAQ up +0.86%, whilst the Philly semiconductor index rose +5.61%, recovering about half of its -10.26% fall last Friday. However, the broader equity mood was more cautious, and the S&P 500 (+0.30%) recovered only a small fraction of Friday’s -2.64% decline. Indeed, almost two-thirds of S&P constituents were lower on the day, with tech and energy the only sectors to post clear gains. And the Mag-7 (-0.06%) struggled to follow the recovery in chipmakers, with Apple (-1.89%) leading on the downside amid a lukewarm reaction to the latest generation of its AI platform.

The equity weakness was clearer in Europe. In part, that was because they’d closed before the worst of the US losses on Friday, so there wasn’t the same bounce back potential. But they were also more exposed to the oil price increase, so the STOXX 600 (-0.15%) fell for a second consecutive session. There were similar moves across Europe, including for the DAX (-0.58%) and the CAC 40 (-0.23%), but Italy’s FTSE MIB (+0.63%) was the main outperformer.

Looking at the overnight data, in China both exports and imports grew at an accelerated rate in May, exceeding forecasts as surging demand for AI hardware mitigated the impact of disruptions caused by the war in Iran. Exports surged by +19.4% y/y in May, surpassing expectations of a +15% increase. This significant rise was partly fuelled by a weak performance last year, during the US-China trade war. Imports soared over +27% y/y in May, resulting in a trade surplus of $105.4 billion, the largest since January. Additionally, South Korea’s economy expanded by +1.8% in the January-March quarter compared to the previous three months, an increase from the 1.7% growth estimated in April. On an annual basis, Asia’s fourth-largest economy grew by 3.8%, revised upward from the earlier estimate of 3.6%.

Looking at the day ahead, data releases include German industrial production for April, the US trade balance for April, and US existing home sales for May. Otherwise from central banks, we’ll hear from the ECB’s Moulin

Tyler Durden

Tue, 06/09/2026 – 08:38

https://www.zerohedge.com/markets/futures-rise-tech-rebound-extends-while-oil-drops