Futures Slide, Oil Jumps After Trump Declares Iran Ceasefire Over

Markets are on the backfoot this morning with equity futures and macro credit under pressure, bond yields spiking, the USD higher, and oil jumping after President Trump thrust geopolitical risks back into focus by declaring the ceasefire between the US and Iran to be over calling it “a waste of time” after the US launched strikes against Iran in response to attacks on ships transiting the Strait of Hormuz. As of 8:00am, S&P 500 futures slid 0.7% and Nasdaq futures slumped 1% dragged lower by memory and chip stocks after the latest kinetic volley. The latter takes place in the context of mixed tech trade in Asia with the Hang Seng Tech Index up 5%, whilst the South Korean Kospi lost 5.4%. Pre-market semis and Mag7 are being sold as Energy and Staples are the two best sectors; everything else is flat to down. The drawdown in momentum and the broader AI infrastructure trade (~85% correlation between these two cohorts) remains heavily in focus, with the GS High Beta Momentum basket (GSPRHIMO) now surpassing -20% over the past 5 days. This morning, global price action is pointing towards “more of the same” with the primary Momentum tone-setters (Hynix -6% in Korea, SNDK -6%, MU -5%) lower across the board. Brent crude advanced 5% to around $78 a barrel while WTI breached $75/bbl (+6%) before declining as the Energy complex leads commodities higher. Precious metals are getting hit with mixed bids to Ags and Base metals. Treasury yields are up around 2-3bps across the curve (10Y yield rising to 4.56%) with the market needing to digest a $39bln 10 year note auction ahead of the FOMC minutes. USD is higher. Higher energy prices feed into inflation expectations and Fed minutes this afternoon take on added significance in the tighter-lipped Warsh era. Gold fell and the dollar wavered.

In premarket trading, all Mag 7 stocks are lower (Meta -1.8%, Nvidia -1.6%, Microsoft -1.4%, Amazon -1.7%, Tesla -1.6%, Alphabet -1.3%, Apple -0.4%).

Chipmakers and other AI-linked names are set for more declines on Wednesday as traders continue to rotate out of the sector.

Energy stocks rally, while airlines and cruise lines slide, after Trump said a tentative ceasefire with Iran is “over,” raising the prospect of an end to peace negotiations and a potential renewal of fighting between the two countries. Chevron (CVX) climbs 2%, while Exxon (XOM) gains 2%.

Alibaba ADRs (BABA) surge 8% after investors turned optimistic on its earnings and shifted capital into major Chinese internet companies.

Bath & Body Works (BBWI) falls 4% after Goldman Sachs analyst Kate McShane cut her recommendation on candle and soap retailer to sell. Sentiment on the company is “trending below historical levels,” including Reddit trends and with younger consumers, Goldman’s analyst writes.

Beazer Homes USA (BZH) climbs 12% after Dream Finders Homes said it has submitted a revised all-cash proposal to acquire the company.

FuelCell Energy (FCEL) falls 21% after the company priced its upsized underwritten public offering of 10.7 million shares of its common stock.

MasTec (MTZ) inches 2% higher after the construction company entered into a pact to buy Electrical Specialists for about $1.65 billion, consisting of about $475 million in MasTec stock and about $1.175 billion in cash.

Navitas (NVTS) is down 7% after Wolfspeed filed a patent infringement lawsuit against the company in the US District Court for the District of Delaware, alleging that a broad range of Navitas products infringes multiple Wolfspeed patents.

Universal Health Services (UHS) slips 2% after Barclays downgraded the hospital operator to equal-weight, saying the fundamental and regulatory backdrop is turning more negative.

Overnight sentiment was hammered when a retaliation by the US on Iranian targets overnight was followed up by remarks just after 4am ET from US President Trump that the ceasefire with Iran is over, saying that “as far as I’m concerned it’s just a waste of time.” The dollar and yields spiked, while WTI crude jumped back above $75 a barrel, Trump’s comments, made on day two of the NATO summit in Turkey, followed the US revocation yesterday of a waiver allowing sales of Iranian oil and subsequent strikes against more than 80 targets. Trump meets Ukraine’s Zelenskyy later. A handful of oil carriers appeared to transit through the Strait of Hormuz early Wednesday, even after a spate of strikes on ships rattled owners and prompted at least one supertanker to turn around midway through its crossing.

Trump’s declaration “marks the most serious rupture yet in an agreement that has been fraying for weeks,” said Violeta Todorova, senior research analyst at Leverage Shares. “Markets had been treating the June memorandum of understanding as a durable de-escalation. That complacency now looks fragile.”

Trump overnight also slammed Spain for not contributing enough to NATO and threatened to cut off all trade with the country.

That said, JPM tried to calm nerves with comments this morning, writing that the situation has not materially changed with neither US / Iran showing a desire for an extended conflict. On the US side, Trump had argued that the ceasefire paused the 60-day limit before he is required to get Congressional approval to extent military hostilities. He was facing resistance to secure additional funding for the war and next year’s military budget during the ceasefire, so another spike to fuel prices adds to that political headwind. On the Iran side, they want legal control of SoH but likely want higher oil prices to pressure Trump and to maintain revenue given the lack of demand for their unsanctioned oil.

“My first read is that investors will not immediately price this as a full return to war, but they also cannot go back to the clean ‘peace dividend’ trade,” said Charu Chanana, chief investment strategist at Saxo Markets. “The bigger point is that any path from ceasefire to durable peace now looks much longer and much more fragile.”

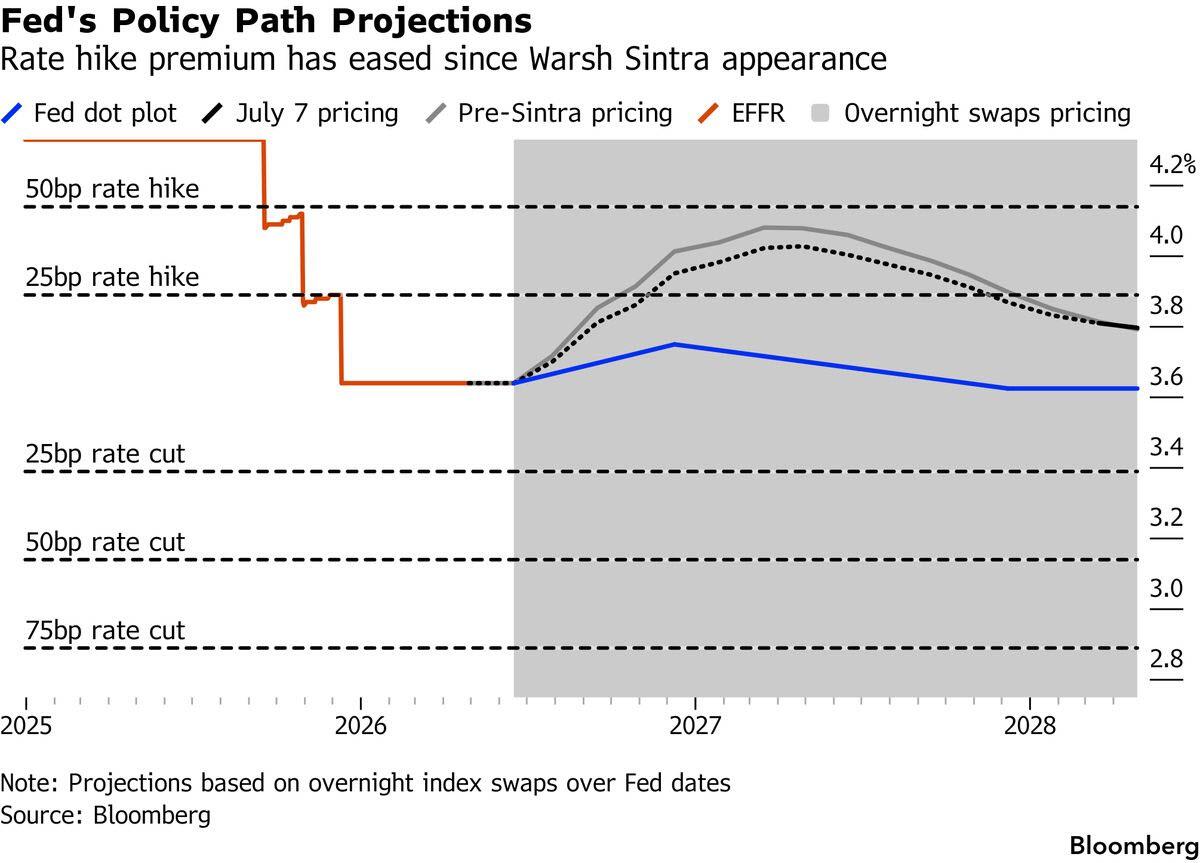

Today’s 2 p.m. ET release of the Fed’s June meeting minutes takes on added significance after Warsh shortened the policy statement and declined to contribute to rate forecasts. Bloomberg Economics’ Andrew Sacher expects the account to reinforce the committee’s focus on above-target inflation and its preference to preserve the option of further tightening. The options market is signaling that investors may be overestimating how much the Fed will raise rates this year. Since Warsh said last week that inflation risks have eased, flows in options linked to the Secured Overnight Financing Rate have tilted toward positions that would benefit if the swaps market pares back expectations for further rate hikes.

Elsewhere, China lifted refined fuel export restrictions for the rest of July and allowed a private refiner to resume shipments after a four-month halt. In New Zealand, the RBNZ raised rates by 25bps (expected) with guidance still leading toward hikes, though with a softened tone. Looking ahead, we will receive wholesale inventories for May and the June FOMC meeting minutes.

In Europe sentiment was hammered with the Stoxx 600 down 1.9% and all sectors ex-energy lower. Energy is the only rising sector, while autos and construction fall the most. Here are some of the biggest movers on Wednesday:

Jet2 shares surge as much as 17%. Analysts see strong booking momentum amid ebbing geopolitical risks and lower jet fuel prices.

TGS shares rise as much as 9.6% after the Norwegian geophysical consulting and services firm reported better-than-expected 2Q results.

Repsol shares gain as much as 4.8% after the Spanish oil company reported a stronger refining margin in 2Q.

Hikma Pharmaceuticals shares rise as much as 6% after a Betaville report regarding possible takeover interest in the UK pharmaceutical company.

Kuros Biosciences gains as much as 12% after Berenberg initiated coverage on the stock with a buy recommendation, saying the Swiss company’s growth is “poised to reach an inflection point.”

Lufthansa drops as much as 6.4% after Citi downgraded the stock to sell from neutral, saying the valuation seems “less compelling” following the recent rally.

Man Group shares drop as much as 3.4% after UBS downgraded the investment management firm on valuation grounds following strong gains.

Rio Tinto falls as much as 3.6% in London to its lowest since March after Morgan Stanley cut the stock to underweight from equal-weight, saying the miner’s valuation is stretched given weaker iron ore fundamentals and limited copper exposure.

Castellum shares drop as much as 4.9% after UBS downgraded the Swedish property firm to neutral from buy, saying “much of the near-term value creation is now reflected in the share price.”

Vistry shares fall as much as 12% after the homebuilder warned of first-half losses.

Boku shares plunge by a record 35%, slumping to their lowest level since 2022, after the payments company warned its results for 2026 will be below market expectations.

Belimo shares fall as much as 7.4% after the Swiss maker of heating, ventilation and air conditioning equipment was cut to sell at Van Lanschot Kempen, which sees a potential increase to guidance as already priced in.

Asian equities fell further after the US President Donald Trump declared the ceasefire between his country and Iran over, escalating geopolitical tensions in the Middle East. The MSCI Asia Pacific Index fell as much as 1%, after swinging between a loss of 1% and gain of 0.4%. Indian stocks reacted adversely to Trump’s comments, with the benchmark Nifty 50 gauge dropping over 2% and a gauge of volatility spiking 30%. Stocks also extended their decline in Indonesia, which relies heavily on oil imports, while futures on Japanese stocks fell 1.3%. The fresh bout of weakness follows a selloff in technology stocks in South Korea, where Samsung Electronics and SK Hynix were among the major drags. South Korea’s benchmark Kospi fell 5.4%, taking its drop from last month’s all-time high to about 20%. Shares also fell in Japan and Australia, while those in Hong Kong and Singapore advanced. Bucking the trend, a key gauge of Chinese shares listed in Hong Kong climbed 4% earlier in the day, as the AI rotation trade gathered pace in Asia. Investors are pulling money from the chipmakers that powered this year’s rally and hunting for cheaper ways to play the technology boom. Elsewhere, Indonesian equities fell after S&P Dow Jones Indices signaled the country could eventually lose its emerging-market status if concerns over its stock market persist. New Zealand stocks fell as the central bank raised its key interest rate for the first time in three years.

In FX, the Bloomberg Dollar Spot Index is up 0.1%. However, performance versus peers is mixed with Kiwi dollar near the top of the leaderboard after a hawkish hike from the RBNZ

In rates, treasuries extended their late-Tuesday selloff as oil prices mounted sharply after US President Donald Trump said the tentative ceasefire with Iran is over. 2-year yields topped 4.20%, approaching this year’s high, while 10-year exceeded 4.58%, cheapest since May 22. US front-end and belly yields are 2bp-3bp higher on the day, flattening 5s30s spread by around 1bp. 10-year, higher by 2bp, trails steeper increases for German and UK counterparts as they catch up with Tuesday’s US yield surge that occurred after European markets had closed. European bonds tumbled as traders added to wagers that central banks will have little choice but to raise interest rates this year. The yield on 10-year gilts jumped 10 basis points to 4.95%, the highest level in nearly a month. This week’s Treasury auctions continue with $39 billion 10-year reopening at 1pm New York time and conclude with $22 billion 30-year reopening Thursday. Demand was strong for Tuesday’s 3-year new issue, which stopped through by 0.6bp and had a record low dealer allotment. WI 10-year yield near 4.575% is ~4bp cheaper than the June auction, which stopped through slightly in a solid result. Focal points of US session include a 10-year reopening auction and publication of minutes of June FOMC meeting. IG dollar issuance slate includes a KfW $6 billion 2-part offering. Amazon’s $25b offering headlined a six-issuer US investment-grade new issue session Tuesday. Issuers paid about 10bps in new issue concessions on deals that were 2.8 times oversubscribed.

In commodities, Brent crude futures are higher by 6.7% and just above the $79/bbl mark as tensions in the Middle East ratchet higher. Oil extended its gains on renewed US-Iran tensions, raising the prospect of a fresh round of conflict in one of the world’s most important energy-producing regions. This came after the US military launched fresh air strikes in Iran and revoked a waiver that allowed it to sell oil globally. Precious metals are on the back foot with spot gold and silver down 1.2% and 2.5% respectively. Bitcoin has slipped over 3%.

US economic data calendar includes May wholesale inventories (10am) and consumer credit (3pm). Fed calendar empty for the session apart from FOMC minutes release at 2pm

Market Snapshot

Top Overnight News

US President Donald Trump said a tentative ceasefire with Iran has ended, raising the prospect of an end to peace negotiations and a potential renewal of fighting between the two countries. “For me, I think it’s over. As far as I’m concerned it’s just a waste of time.” BBG

President Trump slammed Spain for not contributing enough to NATO or spending enough on defense. “Spain is a terrible partner in NATO. They don’t participate. They don’t pay. I don’t want anything to do with Spain. Cut off all trade with Spain,” Trump said at a press conference in Ankara, Turkey. CNBC

South Korean stocks have entered a technical bear market as investors raise concerns about the long-term prospects of the AI chipmakers that have driven a world-beating rally. The Kospi index is down more than 20 per cent from its record high in June after slipping more than 5 per cent on Wednesday. FT

China has lifted refined fuel export restrictions for the rest of July and allowed a private refiner to resume shipments after a four-month halt, trade sources said on Wednesday, as the world’s biggest refiner returns towards normal after disruptions from the Iran war. BBG

The AI rotation trade is gathering pace in Asia as investors pull money from chipmakers and hunt for cheaper ways to play the technology boom. Investors are rotating into one of Asia’s most unloved markets, with Alibaba Group Holding Ltd. and Tencent Holdings Ltd. rising after the Kospi Index was pushed to a technical bear market. BBG

The Reserve Bank of New Zealand raised interest rates Wednesday in what appeared to be a tentative move by policy makers to combat nagging inflation pressures. The official cash rate was raised by 25 basis points to 2.5%. WSJ

OpenAI said its new AI model GPT-5.6 will be made available to the public tomorrow. The White House lifted restrictions on the model after government-approved entities were given a preview. Axios

Nvidia’s stock is the cheapest it’s been since before the AI boom, after losing roughly $1 trillion in market value in under two months. BBG

Wildcatters are racing to secure oil deals in Venezuela, moving faster than Big Oil despite earthquake damage and political uncertainty. Whether the country’s vast reserves can overcome the current challenges remains an open question. BBG

South Korea’s Foreign Ministry said they have signed an MoU with the US and Japan on cooperation to deploy small modular reactors: RTRS.

The sell off in the Goldman High Beta Momentum (GSPRHIMO) has now surpassed 20% over 5 days, exceeding short term expectations for a summer slump in the factor. This magnitude of sell off at such velocity has not been seen since 2020 when the stay-at-home vs go outside narrative shifted meaningfully towards reopening. It is notable that the current drawdown does not have the same strength of catalyst. Fingers have pointed towards SK Hynix raising and META cloud business.

Iran War

Trump stated he “thinks” the ceasefire with Iran is “over”: Trump said the Iran ceasefire is over “I think”; as far as I am concerned, it is a waste of time dealing with Iran. On the MoU, “think it is over”. Adds, “I do not want to deal with Iran”, they are a “bunch of liars”.

US President Trump said (on Iran) he will allow US negotiators to continue to talk if they want. But, “I think this is a waste of time”.

US CENTOM announced that it completed a new round of offensive strikes, hitting over 80 targets with precision munitions. CENTCOM added that forces remain postured and prepared to hold Iran accountable when the agreement is not adhered to or obeyed.

Several explosions have been heard in Bushehr, Iran, according to Mehr news; Mehr’s journalist on Kharg Island denies reported of an attack on Kharg, despite some reported of an incident being published.

In response, Iran’s IRGC said they hit 85 important US military installations in Port Salman, Bahrain’s 5th Maritime Zone and Kuwait’s Ali Salem Air Base.

A more detailed look at global markets courtesy of Newqsuawk

Asia-Pac stocks traded mixed, with Chinese indices the only region in the green amid multiple IPOs and strength in China’s tech space. Sentiment from the US session carried over in the Asia-Pac session, as energy prices surged amid the re-escalation of US-Iran tensions. ASX 200 continued to be weighed on by metals, with the Metals & Mining sector the worst performer, with Materials followed. Energy topped the sector pile Nikkei 225 started on the softer side, briefly returned to the unchanged mark before returning to the downside. KOSPI traded choppy, as the initial weakness briefly reversed to print modest gains. However, weakness returned as the session continued, resulting in the Korea Exchange activating the sidecar on the KOSPI and KOSDAQ. As a result, the KOSPI extended its losses from June peak to 20%, indicating a bear market. Shanghai Comp. and Hang Seng. were the only indices printing gains, with outperformance in the Hang Seng following strength in tech names. The strength can be attributed to two reports: 1) From Reuters, DeepSeek developing its own chip to power AI systems, and 2) from the Information, Zhiphu considering designing its own AI chip.

Top Asian News

China’s MIIT has issued a risk warning regarding the potential security backdoors in the AI programming tool Claude Code.

South Korean Government said companies with consolidated assets of over KRW 10tln will be required to disclose information on their ESG performance and risks, starting 2028.

South Korean Finance Minister said they are to watch risk factors around stock market volatility, will enhance FX monitoring system to respond to night-time volatility.

Japan is considering a change to monetary policy wording in the Honebuto, Asahi reported.

European bourses (STOXX 600 -1.8%) began the session lower amid renewed US-Iran developments which spurred energy benchmarks higher. The move then extended after US President Trump suggested that he thinks the ceasefire with Iran is “over”.

European sectors in Europe are entirely negative (excl. Energy +2%) as they react to elevated energy prices.

Top European News

US President Trump said he is not happy with NATO when it comes to Greenland. Spain is a wasted cause, they do not want to do trade. Cutting off all trade with Spain and all visits. “Do not want to do any more trade with them (Spain)”. Treasury Secretary Bessent has been told to cut off all trade with Spain. US is paying too much into NATO. UK and Italy were both terrible in not allowing the US to use military bases. Greenland is not important to Denmark.

FX

G10s are mostly lower against the Buck excl. commodity exporters CAD and NOK, which are resilient vs. the USD.

USD rose throughout the morning in reaction to energy strength alongside sour equity sentiment after US President Trump said he thought the Iran ceasefire was over. To briefly summarise developments, yesterday the US Treasury revoked the June 21st Iran-related waiver, General License X, which had allowed Iran to produce, deliver and sell its oil; and US President Trump’s remarks this morning accelerated the move higher in USD/oil with “Iran ceasefire is over “I think” the kicker.

Kiwi was the clear outperformer post RBNZ, but reversed gains against the Buck after the aforementioned Trump remarks. To briefly recap, the RBNZ hiked rates by 25bps in a unanimous decision, signalling further hikes to bring inflation to the 2% target mid-point; this saw some participants unwind bets for a hold. AUD/NZD appears the preferred vehicle to express the in-line/hawkish decision, now the Buck has picked up.

JPY continues to underperform amid carry/Terms of Trade implications. USD/JPY remains on a 162.00 handle and has essentially pared that downside seen on potential intervention fears last week having risen throughout the London morning. Reporting overnight via Asahi and Nikkei noted that the Japanese government may tweak a reference to monetary policy in its annual policy agenda to avoid the appearance that it is putting pressure on the BoJ.

Fixed Income

Fixed income started on the backfoot, as benchmarks gradually moved lower as energy continued to move higher overnight given the US revoked Iran’s oil waiver and then conducted strikes on 80 Iranian targets in retaliation to Iran targeting various cargo vessels on Tuesday.

The early morning saw modest additional pressure, with Bunds and USTs lower by roughly 40 and five ticks, respectively, at first. The scheduled docket ahead featured supply and a few data points, but we were primarily awaiting comments from the US and/or Iran after the overnight action.

US President Trump then spoke in Ankara, in a relatively short but packed interview where he said the ceasefire with Iran is over “I think” and specifically on the MoU said, “think it is over”. An update that sparked a marked and continuing move higher in energy, with crude firmer by over 6% and Dutch TTF by over 5%. As such, yields across the curve have jumped, benefiting the short-end most, and curves are bear-flattening globally, though with the US belly faring almost the same as the short-end.

USTs down to a 108-29 base, lower by 13 ticks. We now look to the US 10yr note auction after Tuesday’s 3yr, and thereafter Fed Minutes for June, which will be scoured for further insight into how the first meeting led by Warsh went and how any discussions/disagreements among the board were presented; with particular reference to any mention around Warsh’s view on forward guidance.

Bunds went down to around 125.30 following the above energy action and Trump language, lower by over 80 ticks. Energy-related action aside, the main focus point was a dismal first tap of a 2036 Bund, drawing a b/c of just 1.03x. Results of this sent Bunds lower by nearly 10 ticks, to a 125.23 base.

Gilts opened lower by 57 ticks, acknowledging the US waiver removal yesterday and the tit-for-tat strikes overnight. Thereafter, as Trump spoke, further downside was seen, sending Gilts lower by 130 ticks in total to an 87.16 base. As usual, Gilts underperform amid periods of pronounced energy upside given the sensitivity of the UK market to global benchmarks.

Germany sold EUR 3.902bln vs exp. EUR 6bln 3.00% 2036 Bund: b/c 1.03x, average yield 3.09%, retention 35%.

UK sold GBP 1.5bln 0.125% 2028 Treasury Gilts via Tender: b/c 4.97x (prev. 4.28x), average yield 3.989% (prev. 4.219%), tail (prev. 0.3bps).

Jefferies (JEF) to sell EUR-denominated 7yr noted; guidance seen +175bps to MS.

Spain has reportedly proposed the EU issue an annual EUR 850bln in bonds to save countries billions of euros in interest costs, POLITICO reported.

Australia sold AUD 900mln 4.25% 2036 AGBs: b/c 4.55x (prev. 3.86x), average yield 4.8745% (prev. 4.9735%).

Commodities

Following Iran’s decision to hit Saudi and Qatari tankers, the US struck various sites in Iran. As a result, Iran then hit regional partners, including Bahrain and Kuwait.

US President Trump, who was speaking at the NATO Summit in Ankara, berated the Iranian regime. He stated that it is a waste of time dealing with Iran, and ultimately stated that he thinks the ceasefire and MoU is “over”. The mention of he “thinks”, gives the US a little bit of optionality on whether the deal is actually over; he stated that he will allow US negotiators to continue to talk. Nonetheless, the risks of a wider escalation remain; markets now await clarification on whether the MoU has officially ended, the Iranian response and also how Qatari/Pakistani mediators react to the comments made by Trump.

WTI and Brent started the European session with gains in excess of 2%, but surged higher following the Trump comments; currently +5.6%. WTI Aug’26 holds at the top end of a USD 71.75-75.30/bbl range, whilst Brent Sept’26 sits near peaks of USD 75.44-79.26/bbl range. The latter remains well below the levels seen following the initial signing of the Islamabad MoU (USD 85/bbl), which signals some hopes that a) the Strait will remain open, b) the current MoU holds. On this theme, markets remain in backwardation, with front-month Brent prices still higher than second-month; should this flip, it would indicate that traders expect another large-scale supply glut.

Spot gold (-1.2%) trades lower this morning, and at the bottom end of a USD 4,050-4,133/oz range. Much of the pressure came following the Trump comments, given the USD strength and the inflationary implications of the ceasefire being over. Base metals are broadly lower, given the risk-tone; 3M LME Copper trades at USD 13,190-13,396/t range.

Kuwait’s Ministry of Electricity said power lines were damaged by shrapnel in recent attacks.

European Commission, on the ETS revision, said they are still considering how and whether to add international carbon credits. Revision will include permanent domestic carbon removal. Will propose further investment.

Russia’s Gazprom said Ukraine attacked facilities of gas exports to Turkey; supplies not affected.

China reportedly lifts restrictions on refined fuel exports for the rest of July, according to sources.

China purchases at least 5 more US soybean cargoes, Bloomberg reported.

Japan aluminium premiums for Jul-Sep shipment set at USD 395/t, +12-13% Q/Q.

US Private Inventory Data (bbls): Crude -0.399mln (exp. -1.5mln), Distillates -1.801mln (exp. +1mln), Gasoline -2.929mln (exp. -1.55mln), Cushing -0.069mln.

Trade/Tariffs

Spanish PM Spokesperson said the trade comments from US President Trump are business as usual.

USTR Greer said Canada and Mexico have not lived up to everything.

Geopolitics: Iran Commentary

Iranian Parliament Speaker Ghalibaf said the US has violated major parts of the MoU, citing US attacks on southern Iran, reinstating oil sanctions and threats of further strikes as MoU violations.

Iran’s Foreign Ministry states that the US activity overnight has “rendered important and fundamental parts of the Memorandum of Understanding on the End of the War ineffective”.

Iranian President Pezeshkian said the US, whether as World Cup host or in its foreign policy, manipulates the rules and resorts to deception, and that Iran rejects such tactics.

Iran’s top joint miliary command said Iran will give a crushing response to America’s aggression and terrorist action, and under no circumstances will they allow them to interfere in the affairs of the Strait of Hormuz and its management.

Advisor to Iran’s Supreme Leader said US President Trump intends to attack again and we are fully prepared.

Iran’s Foreign Ministry condemns the US Treasury’s move to revoke the temporary suspension of sanctions on Iranian oil sales, will take any measure it deems necessary to safeguard its interests and national security. Iran holds the US government responsible for the consequences of the breach of the Memorandum of Understanding.

Overnight Attacks

Several explosions have been heard in Bushehr, Iran, according to Mehr news; Mehr’s journalist on Kharg Island denies reported of an attack on Kharg, despite some reported of an incident being published. Elsewhere, sirens were reported in Bahrain once again.

Renewed explosions sounds heard around Iran’s Qeshm and Sirik, Mehr reported.

Iran’s army said it targeted the Sheikh Isa Base in Bahrain and warns of more attacks if the US repeats strikes on Iran, Mehr reported.

Iran’s IRGC said that, in response to the US aggression, they hit 85 important US military installations in Port Salman, Bahrain’s 5th Maritime Zone and Kuwait’s Ali Salem Air Base.

Iran’s IRGC said they downed a US Mq9 drone in the south of Iran, Press TV reported.

Iran fires several anti-ship missiles and drones towards US Navy warships in the Sea of Oman, Fars reported citing the Middle East Spectator.

A US official said the strike on Iran was a punitive action, not a proportional response, and that the operation will not end in the short term, CNN reported.

US Commentary

US President Trump said the Iran ceasefire is over “I think”; as far as I am concerned, it is a waste of time dealing with Iran. On the MoU, “think it is over”. Adds, “I do not want to deal with Iran”, they are a “bunch of liars”.

US President Trump said (on Iran) he will allow US negotiators to continue to talk if they want. But, “I think this is a waste of time”.

US President Trump said have had some great meetings; attacked very powerfully against Iran last night. Have wasted a lot of time with Iran. Iran does not know what it is doing. Iran shot rockets at the ships, which is why the US shot back. Iran is a “dirty” player, “are scum”.

US President Trump approved the Iran strike plan and ordered it while in Turkey, a US official tells Axios’ Ravid; the official said it is still unclear how long the strikes are going to continue.

US Secretary of Defence Hegseth has cancelled his visit to Israel, N12/Ynet report.

Others

Turkish President Erdogan said Europe must take more responsibility when it comes to NATO.

US President Trump said China is attempting to takeover the Panama Canal, will not let this happen. China has been treating the US right. Big fan of Chinese President Xi.

Ukrainian Armed Forces said Kyiv is under missile attack.

Israeli fighter jets carried out attacks in Barachit and Beit Yahoun in southern Lebanon.

A Pakistani Boeing (BA) plane flying to Karachi has crashed, with sources stating the plane was mistakenly targeted by the US, IRIB reported.

Chevron’s (CVX) Yasa Polaris oil tanker, used for CPC shipments, was attacked by drones off Russia’s Black Sea coast, according to sources.

Russia’s Gazprom said Ukraine attacked facilities of gas exports to Turkey; supplies not affected.

Ukraine’s Military said it struck two oil refineries, six tankers, bridges and the Borisoglebsk airfield; AIF-NK oil refinery in Nizhny Kamsk was also damaged.

US Event Calendar

7:00 am: United States Jul 3 MBA Mortgage Applications, prior 0%

10:00 am: United States May F Wholesale Inventories MoM, est. 0.3%, prior 0.3%

2:00 pm: United States FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Asian equity markets are largely lower this morning as investors digest a significant escalation in US-Iran tensions overnight. American forces launched strikes against more than 80 targets in Iran, including air defence systems, command-and-control networks, coastal radar installations, and anti-ship missile capabilities, in response to recent attacks on commercial shipping in the Strait of Hormuz. The strikes were accompanied by the US Treasury’s decision to revoke a waiver that had allowed new Iranian oil sales, a move that threatens to undermine the fragile US-Iran interim peace agreement reached last month.

The developments have reignited concerns about energy supplies and geopolitical risk, helping Brent crude rise more than 2% and trade near $76/bbl this morning after rising more than 5% yesterday, driven by the fresh attacks on ships in the Strait of Hormuz, with Monday seeing the most incidents since the US-Iran interim agreement came into effect on June 17. Iran has condemned both measures as violations of the agreement and vowed a response, raising concerns that the fragile peace process reached last month could unravel before negotiations on a permanent settlement are completed. While US officials have stressed that talks towards a longer-term accord continue, the latest escalation represents the most serious test yet for the ceasefire.

Against this backdrop, risk sentiment across Asia is weak but not as much as you may have imagined given the attacks. S&P, Nasdaq and Stoxx futures are all pretty much flat with the rest of Asia down or up depending on which side of the tech stack they sit on.

The KOSPI losses have accelerated as I’m typing, currently down -5.57% in what seem very fast markets with the Nikkei -0.96%, and the S&P/ASX 200 down -0.49%. In contrast, mainland Chinese equities are firmer ahead of tomorrow’s June inflation report, with the CSI 300 (+0.61%) and Shanghai Composite (+0.52%) moderately higher, whilst the Hang Seng (+2.38%) is outperforming as technology stocks there recover. However, they are just reopening after their lunchtime break as I type so given the vol elsewhere this could change by the time you read.

Ahead of the overnight moves, markets struggled to gain traction yesterday, as the jump in oil prices revived familiar fears about stagflation. That led to clear pain for US Treasuries. For instance, the 10yr yield was up +8.2bps on the day to 4.55%, whilst the 30yr yield (+7.13bps) closed above 5% for the first time in nearly a month, at 5.06%. And on top of the oil moves, those trends got a fresh push from the NY Fed’s latest Survey of Consumer Expectations. It showed 1yr inflation expectations up to 3.7%, the highest since September 2023, whilst 3yr expectations were up to 3.3%, the highest since June 2022. So that leant in a hawkish direction and meant investors dialled up their expectations for Fed rate hikes, with the amount priced by the December meeting up +5.1bps on the day to 34bps.

As all that was happening, there wasn’t much respite for equities either, as chipmakers saw a renewed slump that took the Philly semiconductor index (-4.65%) to its lowest in nearly a month. Indeed, the index is now -15.95% beneath its highs in mid-June, after just posting its best quarter ever in Q2. To be fair it wasn’t all bad news, and US equities saw a rotation into defensive sectors. Energy (+3.02%), healthcare (+1.55%), consumer staples (+0.99%) and utilities (+0.91%) all had a strong performance. Moreover, a majority of the S&P 500’s constituents were still higher, with 283 companies rising on the day. But the chip declines still dragged on the overall performance, with the S&P 500 ultimately down -0.45%.

Over in Europe, political developments were in focus yesterday in both France and the UK. In France, Marine Le Pen said she’d be a candidate in the 2027 French presidential election, after appeal judges shortened a ban on her running for office. The first round isn’t happening until April 18, with the run-off then two weeks later on May 2, but today’s news means that the outlines of the campaign are coming into view.

Meanwhile in the UK, Reform UK leader Nigel Farage resigned as an MP, forcing a by-election that Farage himself is going to stand in. His resignation follows questions around a £5m gift from a Reform UK donor, which had triggered a parliamentary standards probe. Moreover, last weekend the Sunday Times reported that he hadn’t declared benefits from a long-time ally, George Cottrell. So with Farage under growing scrutiny, calling a by-election was seen as a way for him to regain momentum, particularly after Reform UK underperformed polls in the recent Makerfield by-election won by Andy Burnham. However, all the main political parties have said they won’t stand a candidate, effectively calling it a political charade. So it’ll be interesting to see if it backfires. Tomorrow will also see nominations open for the Labour leadership contest that will decide the next PM, although former Greater Manchester Mayor Andy Burnham remains the only declared candidate.

Amidst all the political developments, there wasn’t too much of a market reaction in Europe, with bond yields moving higher across the board because of the oil price rise. So yields on 10yr bunds (+4.6bps), OATs (+5.6bps) and BTPs (+5.8bps) all moved higher on the day, with the STOXX 600 (-0.65%) also falling back as well.

The NATO leaders’ summit will continue for a second day today, with President Trump saying yesterday that the US “could remove all our soldiers out of Europe” and reiterated his desire for Greenland to be under US control. Otherwise, there were multiple reports of defence industry deals that had been agreed, with Bloomberg reporting that was over $50bn.

Shifting back to Asia to close, and the Reserve Bank of New Zealand (RBNZ) has implemented its first key interest rate hike in three years, raising the official cash rate to 2.50% from 2.25%. This move, which was expected, signals the central bank’s intention to transition to a less stimulatory monetary setting in an effort to curb inflationary pressures. The decision follows a split vote at the bank’s previous meeting in May, where Governor Anna Breman had used her casting vote to maintain the cash rate. Following the decision, the New Zealand dollar strengthened by +0.42% to just above 57 cents against the US dollar, with the yield on the policy-sensitive two-year notes increasing by +4.5bps, now trading at 3.37%, amidst reinforced expectations for additional rate hikes this year.

Looking at the day ahead, the highlights will include the minutes of the FOMC’s June meeting, along with remarks from the ECB’s Kocher, Moulin, Nagel and Dolenc. Otherwise there isn’t much data, although we’ll get Sweden’s CPI for June, France’s current account balance for May, and US consumer credit for May.

Tyler Durden

Wed, 07/08/2026 – 08:32

https://www.zerohedge.com/markets/futures-slide-oil-jumps-after-tump-declares-iran-ceasefire-over

{kind=link}

{kind=link}

{kind=link}