BlackRock Private Credit Fund Cuts Asset Values By 5%, As Golub Gates After 8.5% Redemptions

Just another day in private credit paradise… er, hell.

One day after Gundlach repeated his warning that the private credit crisis will end in tears for bagholders, Blackrock cut the value of its publicly-traded private credit fund by about 5%, as it – like most of its peers – struggled under the weight of troubled loans, markdowns and lower returns.

BlackRock TCP Capital Corp., a publicly traded middle-market lending fund, said markdowns totaled $35 million in the quarter ended March 31, according to a statement on Thursday. Amusingly, and in hopes of redirecting attention, the $1.5 billion fund highlighted “improving credit quality,” and said it invested more in senior debt and strengthened its balance sheet. The fund said its dividend, which was cut to 17 cents a share last quarter, would remain flat.

The fund has been a challenge for BlackRock, the world’s largest asset manager with about $14 trillion in assets, which is expanding aggressively into private credit. BlackRock acquired specialist manager HPS Investment Partners last year for about $12 billion, aiming to significantly expand its existing capabilities and legacy funds, including TCPC.

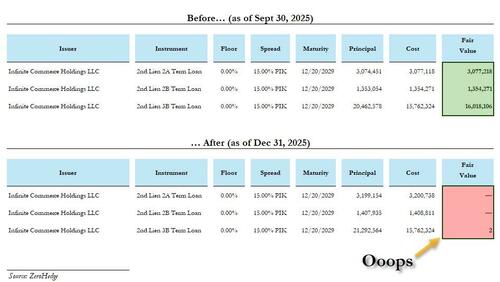

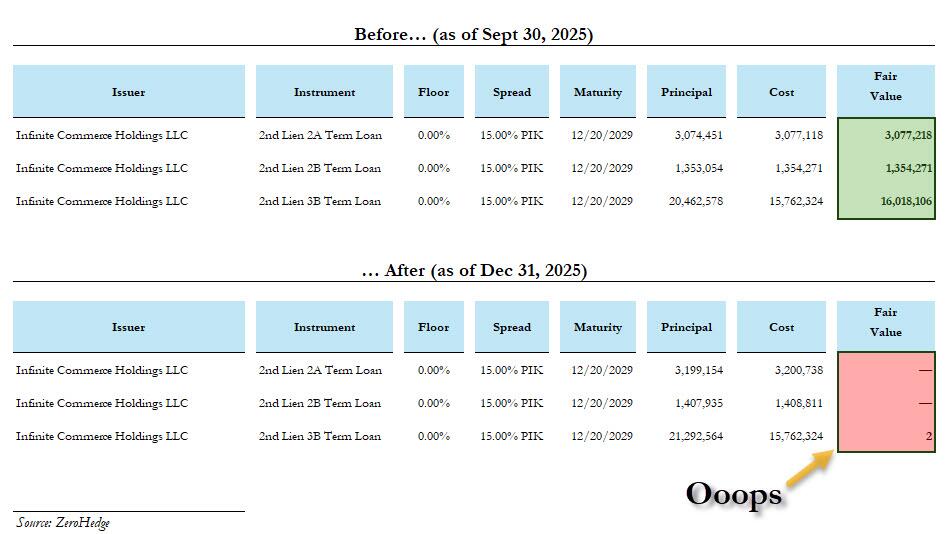

The TCPC fund said in January that it cut the net asset value of its assets by 19%, which sent shares tumbling. The fund has struggled in part due to exposure to e-commerce aggregators – companies that buy and manage Amazon.com Inc. sellers – as well as troubled home improvement company Renovo Home Partners, which filed for bankruptcy. Back in March, we reported that Blackrock slashed the value of one of its private loans from par to 0 in just months, Infinite Commerce Holdings, sparking a selloff in the shares as the market was stunned by how quickly a loan from the world’s most iconic asset manager can go from par to 0 in just days.

“While we have made meaningful progress, we recognize there is more work to do and we remain focused on disciplined execution,” Chief Executive Officer Phil Tseng said on a call with analysts.

Loans on non-accrual status – typically meaning borrowers have missed their debt payments – declined to 7.6% on a cost basis, compared with 9.7% in the prior quarter. That’s because one of its portfolio loans was sold, and two were restructured. Investments in 13 portfolio companies were on non-accrual status.

Tseng said the largest driver of the markdowns was an investment in Job and Talent, a staffing and recruitment company that suffered from weak performance in the quarter. Almost a third of the markdowns came from software-related investments, he said.

Lenders in the $1.8 trillion private credit market have been under scrutiny as advancements in artificial intelligence threaten to upend their bets on software, an industry that makes up a significant portion of lenders’ portfolios.

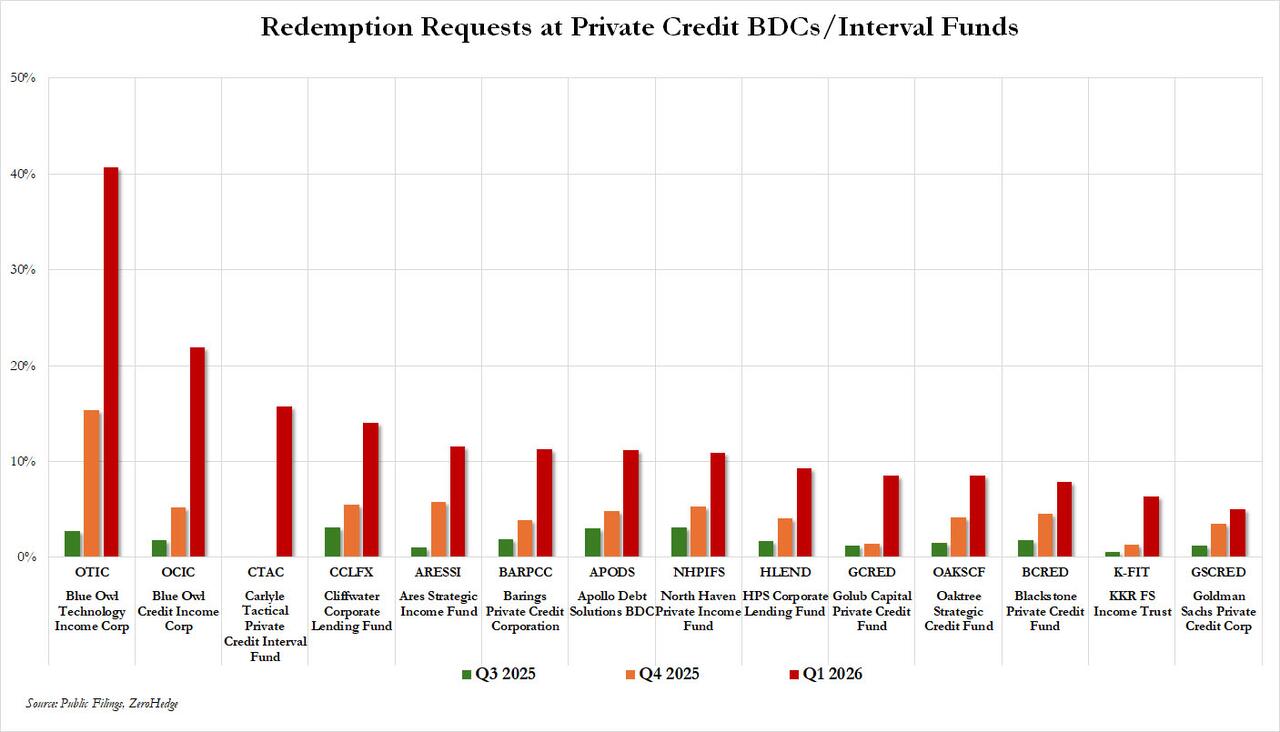

Elsewhere, the last big private credit fund we were waiting to report its redemption gates, did just that: Golub Capital announced it was capping withdrawals from its private credit fund after investors sought to pull 8.5% of shares, the latest instance of a money manager restricting outflows amid a wave of redemption requests.

Golub Capital Private Credit Fund, or GCRED, plans to enforce the quarterly withdrawal limit of 5% of common shares outstanding, according to a letter to shareholders on Thursday. The roughly $9.9 billion fund intends to fulfill repurchase requests for 8,891,200 shares.

The credit manager told investors that the redemption requests “were concentrated in a small subset representing approximately 5% of GCRED’s more than 12,000 shareholders.” Golub also cited roughly 14 million in new share subscriptions this year through the end of April.

GCRED has a liquidity cushion of approximately $4.1 billion and its portfolio consists of nearly $10 billion in total investments at fair value, the firm said. As of the end of the first quarter, less than 0.1% of GCRED’s investment portfolio was on non-accrual status.

None of that mattered in the, and Golub has now joined every single one of its BDC peers in gating its investors. The silver lining, unlike such disasters as the two big Blue Owl BDCs (OTIC and OCIC), which saw investors try to pull 41% and 22% of their capital respectively – and were obviously gated – Golub’s tally was only 8.5%, which in this age where double digit redemptions requests are the normal, is downright respectable.

d

Tyler Durden

Fri, 05/08/2026 – 00:08

{kind=link}

{kind=link}