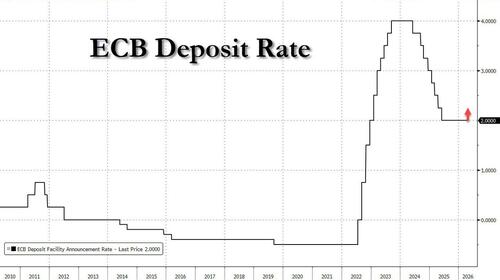

ECB Preview: First Rate Hike Since 2023

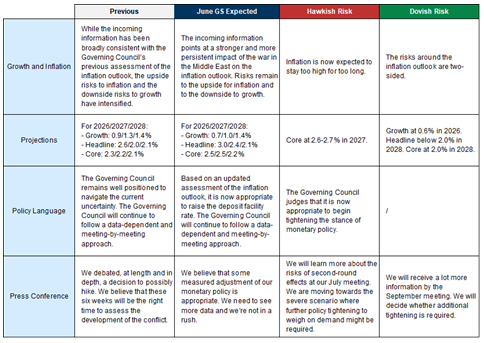

Markets expect the ECB to hike by 25bps, the first rate hike since 2023, but do not look for explicit guidance on the path ahead, with the Council likely pledging in the statement to set monetary policy in a data-dependent and meeting-by-meeting fashion. Lagarde is likely to highlight that tightening is appropriate, for example, by repeating that the energy shock requires “some measured adjustment” in the policy stance. Goldman does not expect her to provide any specific guidance on next steps but look for her to reiterate that the Council wants to see more data and does not need to rush

SUMMARY (courtesy of Newsquawk)

The ECB is expected to hike by 25bps, taking the Deposit Rate to 2.25%. Justified by the assessment that the ECB is past the March baseline and is closer to the adverse scenario.

Alongside this, inflation forecasts will likely be upgraded and growth downgraded across 2026. The cut off date will have influence on the 2026 inflation view, with a later date likely to see less hawkish projections. For growth, any signs of or commentary around a technical recession being possible.

Guidance from the statement will be non-commital with the ECB to perhaps stress a vigilant approach to policymaking, which could be interpreted as a hawkish-nod. Lagarde may be somewhat more explicit vs the statement, in an attempt to stop inflation expectations from becoming unanchored.

OVERVIEW: Recent developments place the ECB somewhere between the baseline and adverse scenarios outlined in March. An assessment that chimes with expectations for a 25bps hike and supports keeping options open for the remainder of the year. However, the balancing act between growth and inflation means that pre-committing to further tightening is not necessary at this point. Instead the ECB, whether via the statement and/or President Lagarde, will likely emphasize that it will be vigilant, or words to that effect, in safeguarding against price pressures in the EZ while acknowledging the deteriorating growth environment.

{kind=link}

EUR/USD and the German 10yr yield approach the meeting around 1.1550 and 3.05% respectively. The market basecase, of a 25bps hike, elevated inflation forecasts and downgraded growth forecasts alongside no firm commitment to further tightening, would likely see a modest hawkish reaction in the above. If the ECB is more direct and places less emphasis on growth and more on inflation, alongside opening the door more explicitly to further tightening, ING looks for EUR/USD and the 10yr yield to rise to 1.1650 and 3.10%; levels we last traded at on the 2nd of June and 21st of May respectively. A more hawkish outcome, particularly a statement/press conference that signals the start of a tightening cycle, could see 1.1700 and 3.15%.

HAWKISH RISK: The projections could show a bigger core inflation overshoot in 2027, with greater concern around the inflation outlook in the monetary policy statement and a clearer signal that additional tightening is coming. For example, the Council could note in the statement that it judges it appropriate to “begin” tightening monetary policy (hinting at a process rather than a one-time adjustment) and Lagarde could open up July by emphasizing that the Council will have important data on second-round effects by then (provided by its corporate telephone, wage and inflation expectations surveys).

DOVISH RISK: The Council could return to a two-sided assessment of the risks around inflation, show an inflation undershoot in 2028 (more similar to the March adverse scenario) and emphasize patience in the press conference (e.g., by stressing that it will receive a lot more data by the September meeting).

{kind=link}

PREVIOUS MEETING: In April, the ECB held the Deposit Rate at 2.00% as expected. The statement emphasized that the US is well positioned to navigate the current period of uncertainty, and as such they were not pre-committing to a particular rate path, sticking to a data-dependent and meeting-by-meeting approach. No new forecasts in April, but the commentary emphasised that upside inflation risks had “intensified”, while longer-term expectations remained “well anchored”. On the growth side, downside risk had “intensified”. The statement sparked a mild dovish reaction, as outside calls for a more hawkish shift were unwound. The subsequent press conference saw President Lagarde unveil that the ECB debated a rate hike, but the decision to hold rates was unanimous. A press conference that sparked a hawkish reaction in European assets. The hawkish skew was added to by subsequent sources, suggesting that a June hike was seen as very likely, Reuters reported.

PRICES: Mayʼs inflation data had a headline rate of 3.2%, ticking up from the 3.0% in April. Pertinently, the ECBʼs HICP Y/Y forecast for 2026 is 2.6% in the baseline, 3.5% in the adverse and 4.4% in the severe scenario. As such, the May print took the bloc further away from the baseline and towards the adverse projection, a point that factors firmly in favour of tightening monetary policy; though the gap to the severe scenario means a 50bps move or pre-committing to tightening post-June are not warranted yet. Within the May series, the internals saw further upside in the energy component and pertinently a jump in Services, to 3.5% from 3.0%. Continuing with May, the Final S&P PMIs showed price pressures intensifying “to their most worrying for over three years, hinting at inflation potentially running close to 4% in the coming months.”. A view that, if shared among policy setters, could see some in favour of more explicit guidance than the statement and/or Lagarde are likely to give. From the ECB itself, the latest Consumer Expectations Survey for April (released in June) vs March, showed one- and five-year consumer expectations remain the same at 4.0% and 2.4% respectively. While the three-year view moderated to 2.9% (prev. 3.0%). Figures that are all above the 2% long-term target, however, the unchanged view shows that expectations were not unanchored in April and, while somewhat dated, provides policymakers with further scope to take an “insurance” hike, given the clear price pressures, but not commit to anything further at this stage.

For the new macroeconomic projections, the above points to an upgrade of at the very least the baseline view, but likely also one or possibly both of the alternative scenarios. Specifically, Nordea expects the 2026 baseline to lift to 3.0% (prev. 2.6%). One point of nuance in the forecasts, particularly for prices, is the cutoff date. In March, the ECB used an exceptionally late cut-off date and a very small date range for the assessment. The above is based on that being repeated and an early June cut-off being used. If not, then the technical assumptions around energy will be significantly higher and as such the near-term inflation view would be more hawkish vs a later cut-off.

ECONOMY: Q1 GDP for the EZ stood at -0.2% Q/Q, after being subject to a marked downward revision in the 3rd estimate from 0.15%. However, some of this stems from a -12.1% print from Ireland, hit by the unwind of tariff and pharmaceutical related activity in the comparison. A more timely indication courtesy of the S&P PMI for May points to another -0.2% Q/Q print in Q2, bar any significant shift in June; if realised in the hard data, that would see the EZ enter a technical recession. Furthermore, the PMI showed a pick up in labour market losses. Unemployment data from member nations remains weak, with the EZ figure in April ticking up to 6.3% (prev. 6.2%). The most timely data available at the time of writing is the German GfK for June, which was bleak at -29.8 though it did improve slightly from -33.3 despite NIM outlining that the “negative impact of the conflict in the Middle East remains largely unchanged…”.

For the new macroeconomic projections, the data is indicative of a downgrade. In March, the 2026 baseline, adverse and severe scenarios were 0.9%, 0.6% and 0.4% respectively. Nordea looks for the 2026 baseline to be downgraded to 0.7%. Taking the ECB closer but not to the adverse scenario from March, and as such chimes with the narrative for an insurance hike and while it does not aid the argument for further 2026 tightening, it does not shut the door to a post-June move.

COMMENTARY: Overall, commentary chimes with consensus for a 25bps hike in June, given recent economic developments, but that it is too soon to commit to any tightening thereafter. Recently, Schnabel (26th May) outlined that prices are between the baseline and the adverse scenario, adding that “in terms of persistence, we have actually moved beyond the adverse scenario, which assumed a rapid normalisation of oil prices.”. Prior to that, on the 26th of May, Schnabel said that they should hike in June irrespective of the peace proposal. Simkus (29th May) described a near term move as an insurance hike, but also downplayed the impact of even 50bps of tightening over 2026, noting that the timing for a second move is less clear. In terms of forward guidance, Lane (26th May) remarked that they will not be pre-commiting to a particular path after June.

TRADES: Goldman likes to receive July/September meeting switch at ~18bps (72% chance). The bank thinks that you can have both a (near term) hawkish path to no hike in September, as well as a dovish path. The (near term) hawkish path would involve no near-term resolution on Iran, with the SOH continuing to be closed by the time of the July meeting, leading to a second ECB hike in July. Subsequently, you could then either have a resolution between July and September, or signs of further economic weakness and limited wage pass through, meaning that, by the time of the September meeting, and with policy rates at the upper end of neutral, the ECB decides to skip a rate hike at the September meeting. The dovish path is one of a near term resolution and a glut of oil from ships stuck in SOH hitting the market, pushing down energy prices and inflation and inflation expectations. In this scenario, it is very feasible, that the ECB will not hike rates again after the June meeting.

THOUGHTS FROM GOLDMAN’S TRADING DESK:

Jari Stehn (Head of European Economics): We expect the ECB to hike by 25bp but do not look for explicit guidance on the path ahead, with the Council likely pledging in the statement to set monetary policy in a data-dependent and meeting-by-meeting fashion. Lagarde is likely to highlight that tightening is appropriate, for example, by repeating that the energy shock requires “some measured adjustment” in the policy stance. We do not expect her to provide any specific guidance on next steps but look for her to reiterate that the Council wants to see more data and does not need to rush.

George Cole (Head of European Rates Strategy): Our bias is for terminal rate pricing lower and flatter curve. Key for today’s meeting will be the signal on July, currently priced not far off 50/50. If the message is that July is more of a tail outcome then market can shift towards pricing one and done, particularly given leak lower in energy prices on view that SoH is more impaired than fully shut with increasingly more oil transiting (though obviously a lot of headline risks with waR). Ultimately September is a long way off with ample time for resolution and/or the lower growth impacts of the war to come through. Specifically we will be watching:

Core inflation forecasts and whether they show persistence – GS econ are 2.5% both for 26/27; would be dovish if lower/inverts

Whether Lagarde emphasizes that tomorrow’s move buys time to watch the data and that currently little signs of 2nd round effects in the labour market

Jan Scheffel (Global Co-Head of Short Term Macro Trading): Given the high level of uncertainty we expect the ECB to keep full optionality on the future policy rate path, neither pre-committing or ruling out a move at the July meeting. We would expect Lagarde to use communication along the line of: “In assessing the timing and extend of further policy adjustments, the governing council will take a data-dependant, meeting by meeting, approach. We are not pre-committed to any policy path.”

Tyler Durden

Thu, 06/11/2026 – 07:45

https://www.zerohedge.com/markets/ecb-preview-first-rate-hike-2023