Key Events This Week: First Warsh FOMC, Iran Deal Signing, Retail Sales And More

After 107 days and a seemingly endless number of false dawns, we finally have a deal between the US and Iran to end the war and open the Strait of Hormuz. It was announced on Sunday afternoon – Trump’s birthday, shortly before futures opened for trading and ahead of today’s Iran game in the World Cup – and the MoU will be signed in Switzerland on Friday.

According to statements carried by Iranian state-affiliated media, the agreement includes a phased lifting of US sanctions on Iranian oil exports, the unfreezing of roughly $12bn in overseas assets, and a commitment to reopen the Strait of Hormuz within 30 days (after mine clearing) alongside the removal of the US naval blockade. The deal also sets out a 60-day negotiation window on a broader accord, including constraints around Iran’s nuclear programme, where Tehran is expected to commit to maintaining its current status and not pursuing nuclear weapons. The US hasn’t been so explicit and whilst the deal is very good news for markets it looks like tough conversations will have occur in the 60-day window to ensure the peace is sustainable. As an example, the Senate needs to approve any extensive sanction relief for Iran.

The other major story is the decision late on Friday from the US government to issue an export control directive forcing Anthropic to restrict access to its most advanced models, Fable 5 and Mythos 5, released to great global acclaim last week, to US nationals only, citing undefined national security concerns. In practice, because it is operationally difficult to separate users by nationality, Anthropic opted to suspend access to these models entirely on a global basis. The move marks one of the first instances of the US applying export controls not just to AI hardware (e.g. semiconductors) but directly to frontier models themselves, reflecting a growing view of AI as a strategic, dual use asset.

Clearly the export control may only be temporary as the cited jailbreak risk is examined and rectified quickly. This is probably the most likely outcome. However, if it longer-term, and more strategic from the US government, it’s not great news for US tech firms or for those assuming breakneck speed of AI adoption. US tech firms require a global marketplace to justify their huge investments so far. In addition, global enterprise would want to ensure any models they purchase are usable, especially for business-critical operations. You can’t rely on something that could be switched off. So all eyes on what Anthropic and the US government agree as the next step.

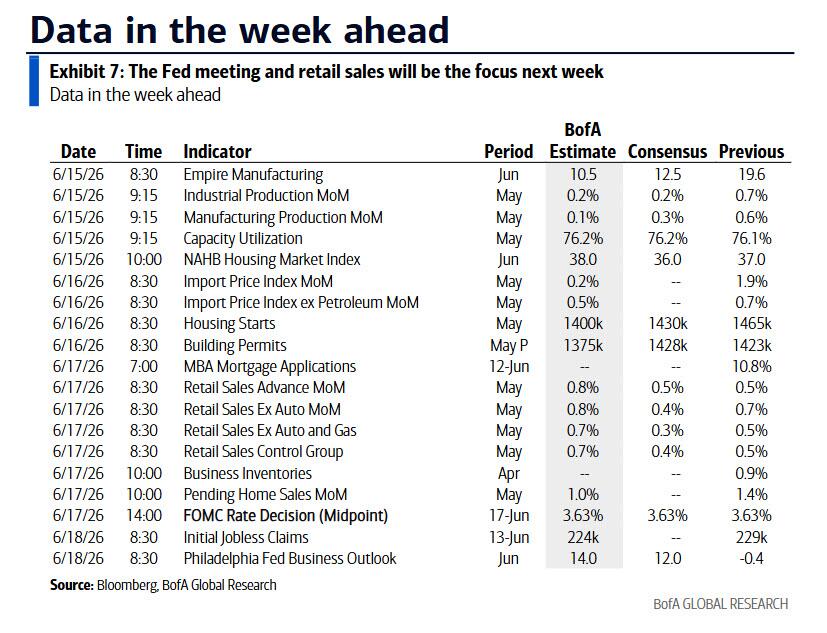

Outside of Iran and AI, central banks will dominate the global agenda in the coming week, with key policy decisions across the Fed, BoJ and BoE alongside important inflation and activity data.

The primary focus will be the United States and Wednesday’s FOMC meeting, which marks the first under new Fed Chair Kevin Warsh. The leadership transition introduces a higher-than-usual degree of uncertainty around both policy signalling and communication style. While an immediate policy shift is unlikely, the meeting will be closely scrutinized for early indications of how Warsh intends to reshape the Fed’s framework, particularly given his stated ambition for a broader “regime change”.

In terms of the statement, a modest upgrade to the labor market assessment appears likely, reflecting steady job growth and a broadly stable unemployment rate. More importantly, the guidance language could shift meaningfully. Warsh has been openly critical of heavy reliance on forward guidance, so the Committee may lean towards a more neutral, data-dependent formulation. This would effectively remove any residual easing bias and reopen the possibility of further tightening should inflation dynamics warrant it. Any such adjustment would be interpreted as a recalibration towards optionality rather than a firm directional signal.

Beyond the headline statement, attention will turn to the Summary of Economic Projections. The distribution of rate expectations may shift upwards, with 4 or 5 policymakers signalling the potential for hikes into 2026 and beyond. This would likely nudge the median path higher across the projection horizon and reinforce the idea that the Fed is not yet comfortable declaring victory on inflation. DB’s economists note that Warsh may not submit dots which would reflect his views on forward guidance. Revisions to inflation forecasts, particularly for the outer years, will also be closely examined for evidence of more persistent price pressures. At the moment DB economists expect core PCE for 2027 to be raised by a tenth to 2.3%.

However, the most revealing element of the meeting may be Warsh’s press conference. His prior remarks suggest he will likely place less emphasis on near-term data fluctuations and explicit forward guidance, instead favoring a broader narrative around structural forces such as productivity and technological change. While this could temper the immediate hawkish interpretation, markets may test whether this framing is sufficient to justify patience in the face of still-elevated inflation. Just as important will be any early signals on communication reform—whether through changes to the dot plot, adjustments to the SEP, or a broader rethink of how the Fed conveys uncertainty. So a fascinating meeting to look forward to.

In terms of US data, the focus will be on May retail sales due Wednesday, and our US economists expect a +0.5% MoM rise in the headline (same as in April). Industrial production is due today (DB forecast is a +0.1% MoM increase, down from +0.7% in April) and there will be several housing indicators out this week as well. US markets will be on holiday for the Juneteenth National Independence Day on Friday.

{kind=link}

Outside the US, central bank activity remains heavy. In Europe, decisions are due from the Riksbank and a cluster of Thursday meetings including the Bank of England, Swiss National Bank and Norges Bank. In the UK, the BoE is expected to keep rates unchanged, with attention focused on the vote split (expectations for 7-2) and any evolution in guidance against a backdrop of still-sticky inflation. Incoming UK data, particularly CPI (Wednesday), labour market indicators (Thursday) and retail sales (Friday), will provide important context for the policy outlook. Meanwhile, euro area attention will also be shaped by ongoing commentary from ECB officials and sentiment indicators such as the German ZEW survey (tomorrow).

Political developments will also be in focus, with the G7 leaders meeting early in the week (today through Wednesday) followed by the European Council summit (Thursday-Friday).

In Asia, the Bank of Japan meeting (tomorrow) stands out, with expectations for a further rate increase as part of its gradual normalization process. Japanese inflation data later in the week (Friday) will help gauge whether underlying price momentum continues to justify policy tightening. In China, their monthly activity data tomorrow covering industrial production and retail sales will provide an updated read on the growth trajectory, with expectations for a modest improvement after recent softness.

Elsewhere in the region, the Reserve Bank of Australia is likely to remain on hold (tomorrow), while New Zealand’s GDP release (Wednesday) will offer further insight into the strength of its economic recovery.

Courtesy of DB, here is a day-by-day snapshot of key events

Monday June 15

Data: US June Empire manufacturing index, NAHB housing market index, May industrial production, manufacturing production, capacity utilisation, Germany May wholesale price index, Italy April trade balance, general government debt, Eurozone April industrial production, trade balance, Canada May housing starts, April manufacturing sales

Central banks: ECB’s Lagarde, Cipollone, Nagel, Pereira and Kocher speak

Other: G7 leaders’ summit (through June 17)

Tuesday June 16

Data: US May housing starts, building permits, import price index, export price index, June New York Fed services business activity, China May retail sales, industrial production, investment, home prices, Germany June Zew survey, Eurozone June Zew survey, Canada May existing home sales, April international securities transactions

Central banks: BoJ decision, RBA decision, ECB’s Lane, Sleijpen and Escriva speak

Auctions: US 20-yr Bond (reopening, $13bn)

Wednesday June 17

Data: US May retail sales, pending home sales, April business inventories, UK May CPI, RPI, PPI, April house price index, Japan May trade balance, April core machine orders, New Zealand Q1 GDP

Central banks: Fed decision, Riksbank decision, ECB’s Sleijpen speaks

Thursday June 18

Data: US June Philadelphia Fed business outlook, May leading index, April total net TIC flows, initial jobless claims, UK April average weekly earnings, unemployment rate, May jobless claims change, Italy April current account balance, ECB April current account, Eurozone April construction output, Canada May industrial product price index, raw materials price index

Central banks: BoE decision, SNB decision, Norges Bank decision, ECB’s Kocher, Nagel, Cipollone, Lane and Escriva speak

Auctions: US 5-yr TIPS (reopening, $24bn)

Other: European Council summit (through June 19)

Friday June 19

Data: UK June GfK consumer confidence, May retail sales, public finances, Japan May national CPI, Germany May PPI, Canada April retail sales

Central banks: ECB’s Lane, Escriva and Cipollone speak, BoJ minutes of the April meeting

Other: US Juneteenth holiday

* * *

Looking at just the US, the key economic data releases this week are the import prices report on Tuesday and the retail sales report on Wednesday. The June FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chairman Warsh’s press conference at 2:30 PM.

Monday, June 15

08:30 AM Empire State manufacturing index, May (consensus 13.2, last 19.6)

09:15 AM Industrial production, May (GS +0.1%, consensus +0.3%, last +0.7%); Manufacturing production, May (GS +0.1%, consensus +0.3%, last +0.6%); Capacity utilization, May (GS 76.1%, consensus 76.2%, last 76.1%): We estimate industrial production edged up by 0.1% in May, reflecting increases in auto and oil and gas production, but a decline in natural gas production. We estimate capacity utilization was unchanged at 76.1%.

10:00 AM NAHB housing market index, June (consensus 37, last 37)

Tuesday, June 16

08:30 AM Import price index, May (consensus +0.8%, last +1.9%); Export price index, May (consensus +0.6%, last +3.3%)

08:30 AM Housing starts, May (GS -1.5%, consensus -2.0%, last -2.8%) ; Building permits, May (consensus -0.2%, last +4.4%)

Wednesday, June 17

08:30 AM Retail sales, May (GS +0.4%, consensus +0.5%, last +0.5%); Retail sales ex-auto, May (GS +0.4%, consensus +0.5%, last +0.7%); Retail sales ex-auto & gas, May (GS +0.2%, consensus +0.3%, last +0.5%);Core retail sales, May (GS +0.2%, consensus +0.3%, last +0.5%): We estimate nominal core retail sales increased 0.2% in May (ex-autos, gasoline, and building materials; month-over-month SA), reflecting a continued solid signal from alternative data but potential payback after several months of outsized increases. On an inflation-adjusted basis, we forecast a 0.3% increase in the core; the relevant deflator in the PCE price index likely declined 0.1% in May. We estimate nominal headline retail sales increased 0.4%, reflecting higher gasoline prices.

10:00 AM Pending home sales, May (GS +2.0%, consensus +1.0%, last +1.4%)

02:00 PM FOMC statement, June 16-17 meeting: As discussed in our FOMC preview, at its June meeting, the first under new Chairman Kevin Warsh, the FOMC is likely to keep the funds rate unchanged at 3.50-3.75% and drop the previous forward guidance suggesting cuts. We expect the median dot to show no change to the funds rate in 2026, with three participants projecting a hike this year. We expect the median dot to still show two cuts eventually, most likely one in each of 2027 and 2028. We assume that Chairman Warsh will not submit dots in light of his past criticism of forward guidance, but we are not sure. The economic projections for 2026 are likely to show slightly lower GDP growth and unemployment, and much higher headline and core inflation, but we only expect a small increase in the inflation projections for 2027.

Thursday, June 18

08:30 AM Philadelphia Fed manufacturing index, June (GS 5.0, consensus 10.0, last -0.4)

08:30 AM Initial jobless claims, week ended June 13 (GS 225k, consensus 225k, last 229k); Continuing jobless claims, week ended June 6 (consensus 1,785k, last 1,795k)

Friday, June 19

Juneteenth National Independence Day. NYSE will be closed. SIFMA recommends bond markets also remain closed.

Source: DB, Goldman

Tyler Durden

Mon, 06/15/2026 – 10:00