On Verge Of Credit Shock: Credit Card Debt Posts Biggest Drop Since Covid Crash As Rates Hit Record High

On a day when an early attempt by the BOJ to kickstart the global carry trade by capitulating on Japan’s recent mistimed foray into rate hikes, has crashed and burned with stocks tumbling, amid renewed concerns that the US economy is slowing (at least until next week’s “surprising” CPI beat), moments ago the Fed poured gasoline on the rising flames when it reported June consumer credit data that was atrocious, and confirmed our worst fears: the consumer has hit a brick wall.

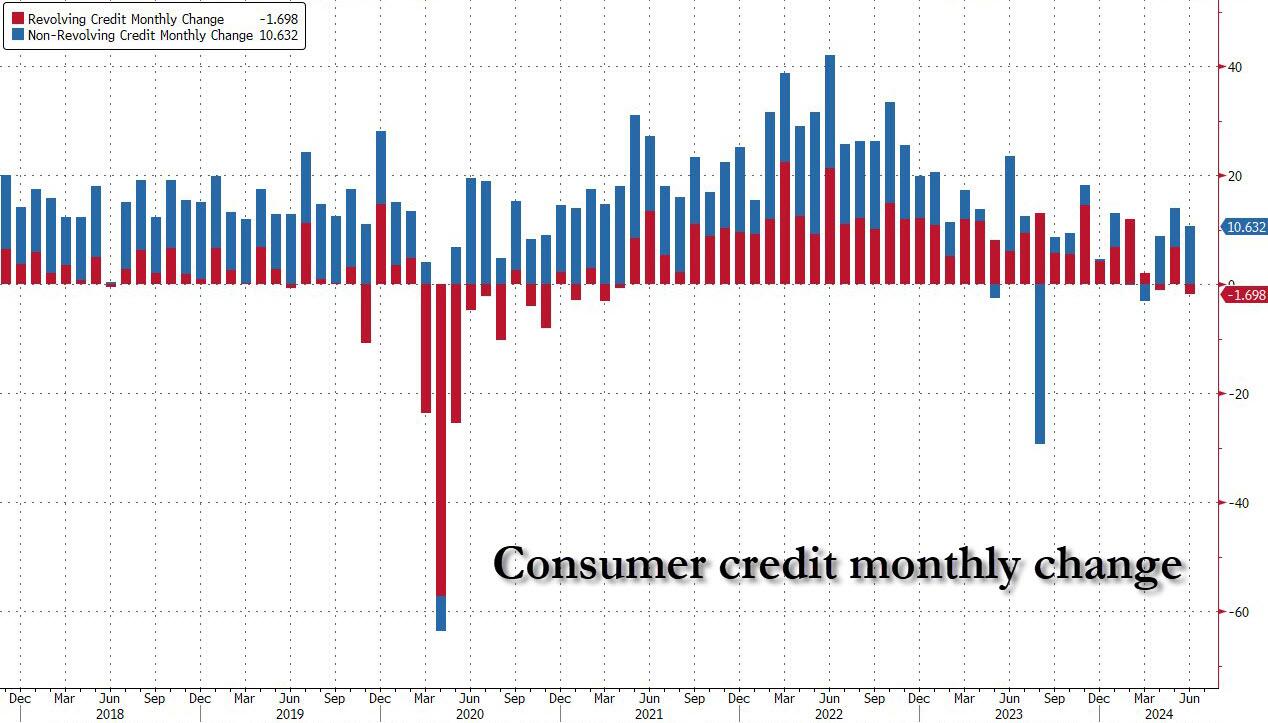

According to the Federal Reserve’s monthly consumer credit report, in June total consumer credit rose just $8.9 billion, below the median estimate of $10 billion, and a material drop from the upward revised May print of $13.9 billion.

But while the total number was not shocking, if confirming the recent declining trend which always signals economic contraction (since without credit, US consumers simply can’t spend), it was the composition that was a big surprise.

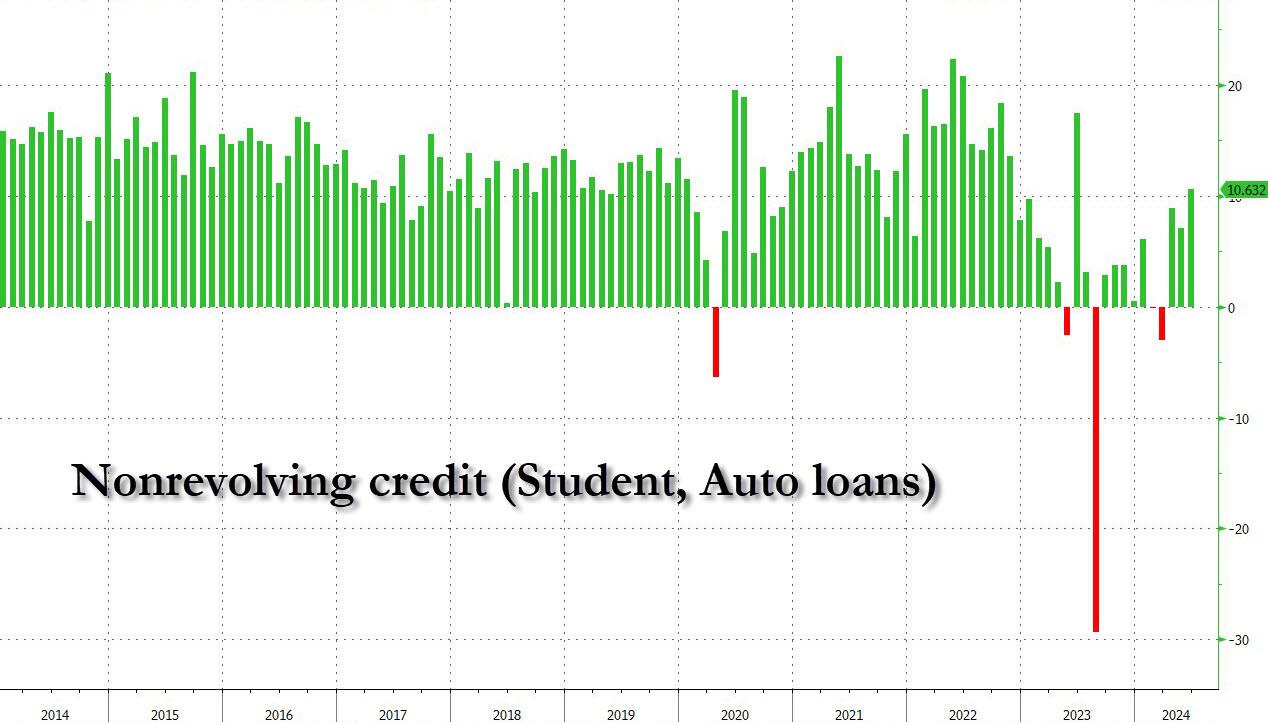

On one hand, non-revolving credit – which consists of student and auto loans – rose by $10.6 billion, which was the biggest monthly increase since last June.

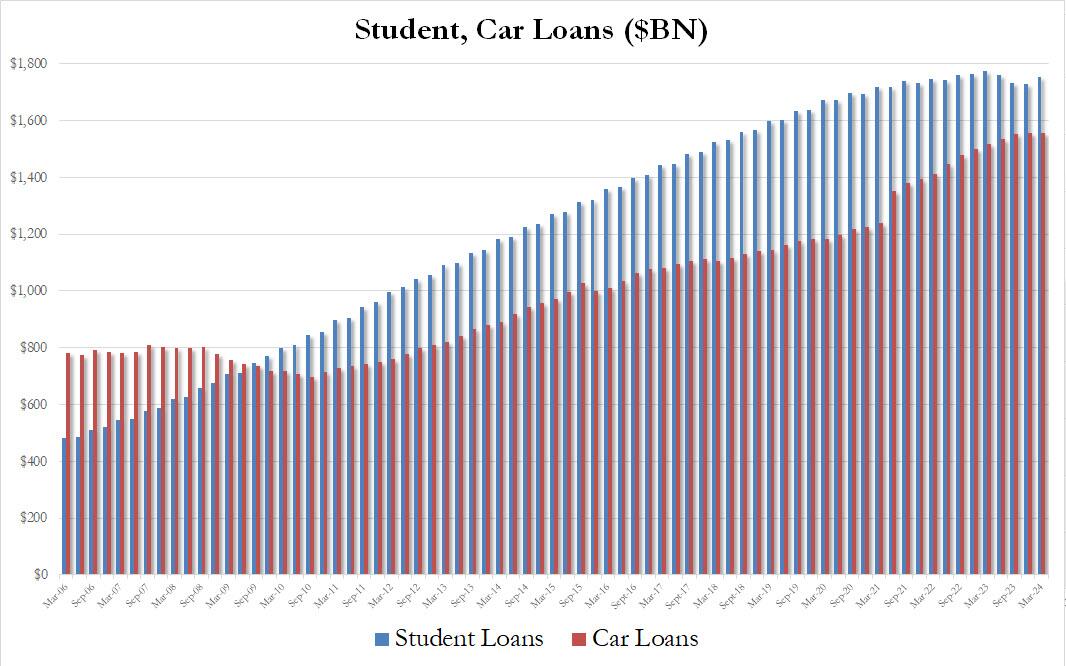

However, a closer look here reveals that the entire increase here was due entirely to student loans, which are once again being repaid after the Biden repayment moratorium ended in late 2023. Meanwhile, car loans which are critical to keep the US automotive industry in gear, has flatlined. As shown in the chart below, in Q2, student loans increased by $10.7 billion, the biggest quarterly increase since Q3 2023, while car loans actually declined by $9.0 billion, the biggest quarterly decline since Q3 2023.

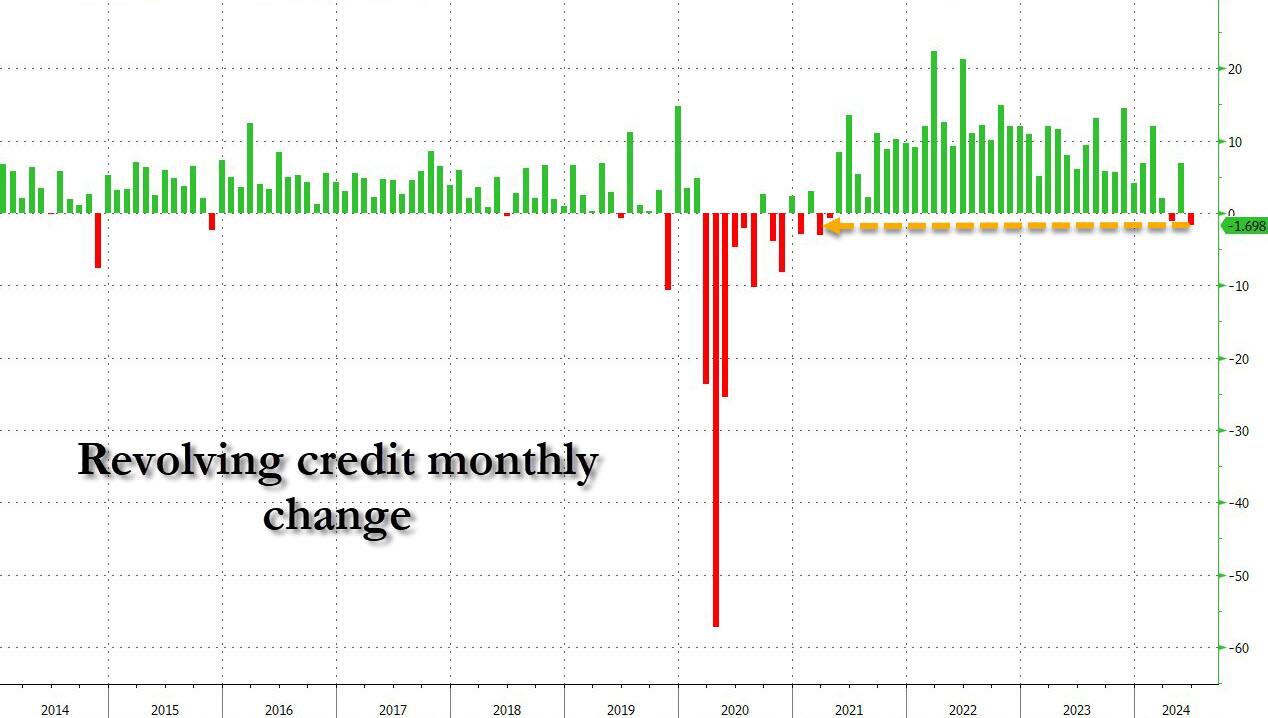

But while non-revolving credit saw a sizable increase, if entirely due to student loans finally catching up to where they should have been 3 years ago, it was revolving credit (i.e., credit card debt) that was the real shocked, because in June, revolving credit unexpectedly tumbled by a whopping $1.7 billion, the biggest drop since the covid collapse…

… and more ominously, every time there is a sizable drop in this category, some economic calamity either follows or has already started.

To get a sense just how rare it is to get a negative credit card debt monthly change, consider that in the six years prior to the covid crash, the US had recorded just 5 months of negative prints, and all tended to precede major drawdowns in the economy. We expect no less this time.

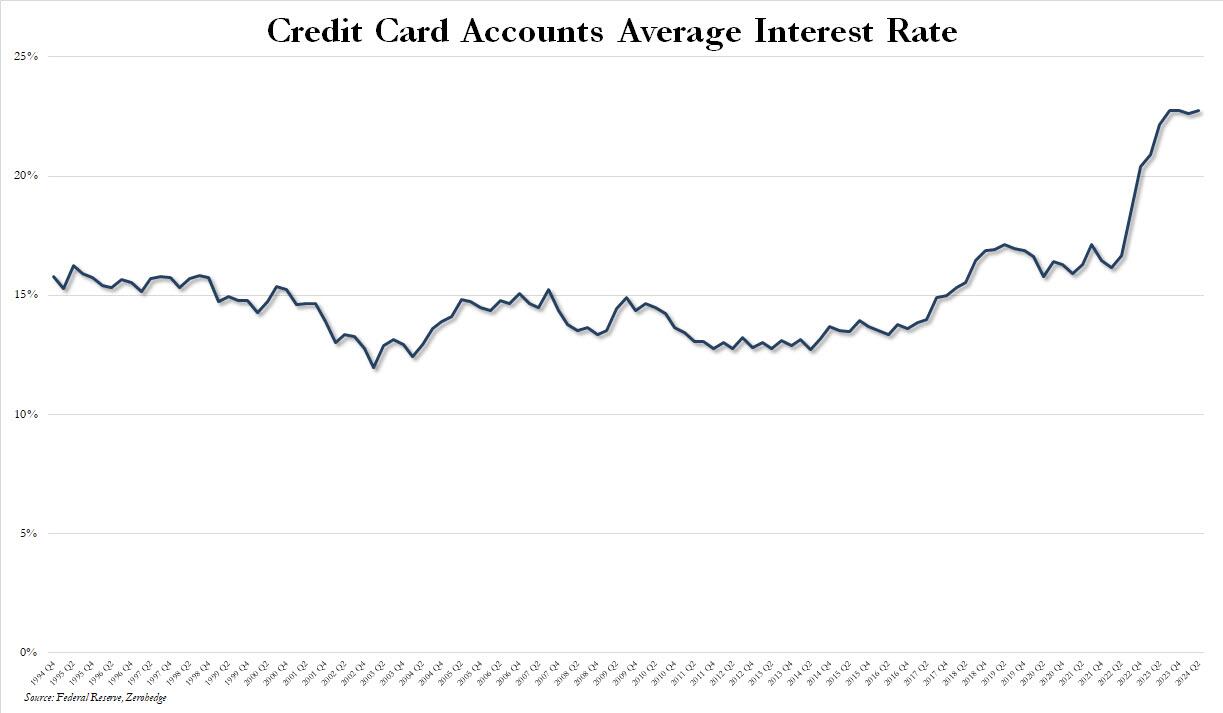

Of course with the Fed refusing to cut rates – for good reason – the brutal slowdown in new credit card debt is hardly a surprise because in Q2 the average rate interest-bearing credit card accounts just hit a new record high of 22.76%, which is a vivid reminder that while banks are happy to hike credit card rates, they rarely if ever cut them.

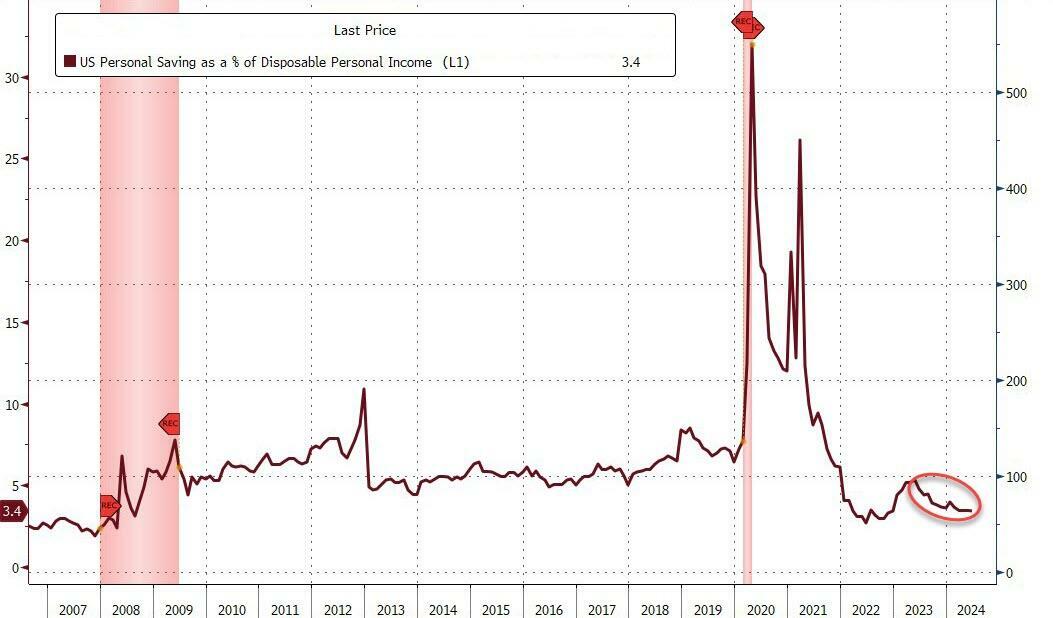

Yet with consumers ever more strapped for actual cash and equity, as the personal savings rate in the US has collapsed from over 5% to 3.4% – the lowest since 2022 – in just a few months…

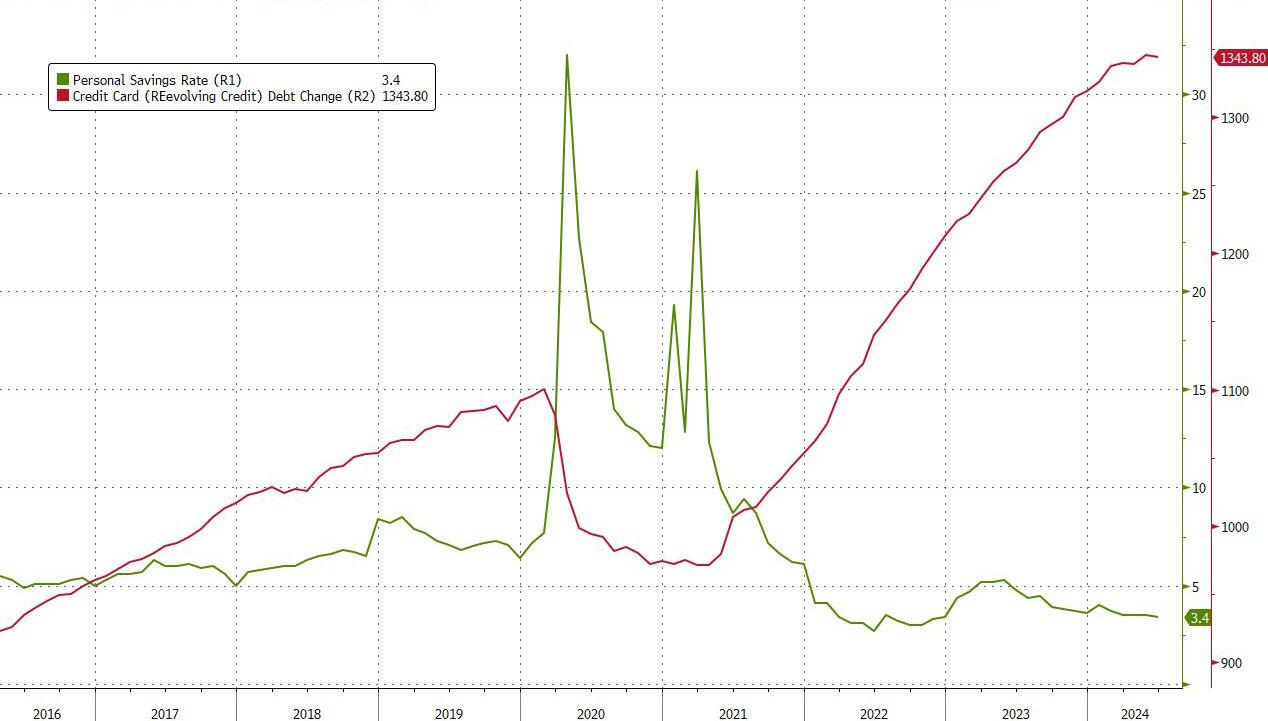

… there is only so much more credit card maxing out that can take place before reality finally sets in, as can be seen in the next and perhaps most striking chart yet: total credit card debt is at an all-time high while the personal savings rate is record low!

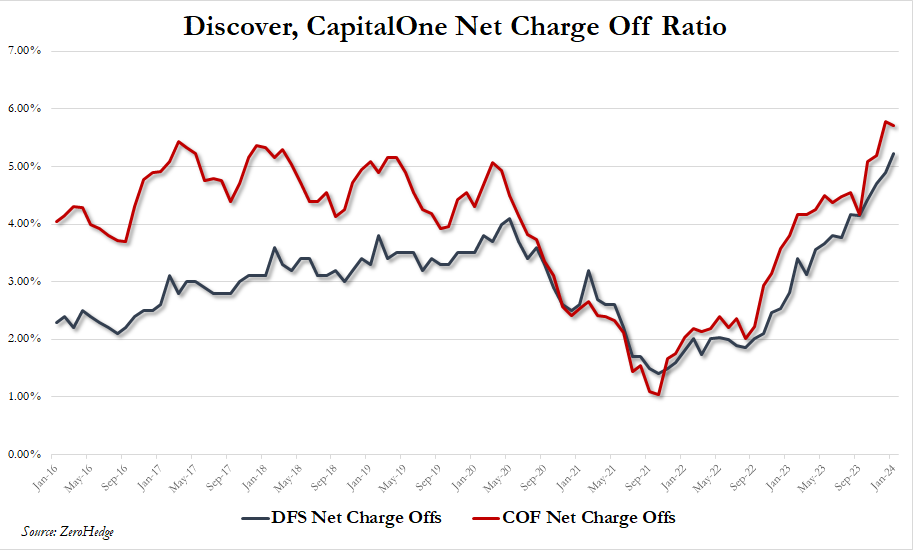

Then again, with an election on the horizon – one which ensures that any credit-card fueled spending must be encouraged – don’t be surprised if the White House directly orders banks to just ignore soaring delinquency and charge-off rates…

… only for the credit shock hammer to fall on the first day of Trump’s new presidency.

Tyler Durden

Wed, 08/07/2024 – 15:36

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}