Prospective Homebuyers Face Another Year Without Affordability Relief

Goldman economist Ronnie Walker has some bad news for prospective homebuyers: while the housing market appears soft but broadly stabilizing, affordability pressures are unlikely to abate anytime soon.

Walker expects mortgage rates to remain elevated through next year, while national home prices are still forecasted to rise modestly. That means buyers waiting for a price correction or lower rates may be disappointed, as the market remains locked in an ultra-low-turnover environment where high borrowing costs, limited affordability, and sticky prices keep many folks on the sidelines.

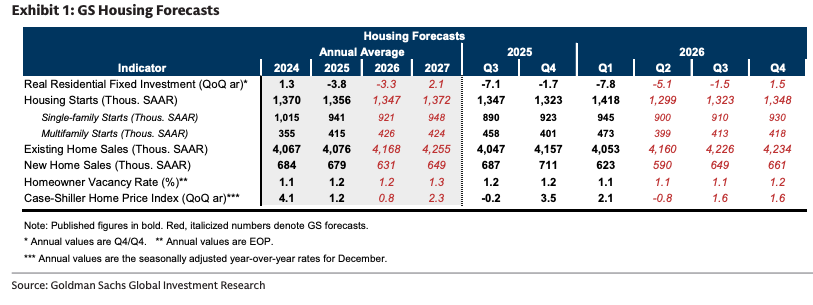

“We expect housing demand to remain tepid,” Walker wrote in the note. He pointed out that the 30-year fixed mortgage rate is likely to fall marginally to 6.43% by year’s end and hover around 6.3% for 2027.

Here’s more context from Walker about the US housing market and his mid-year outlook into next year:

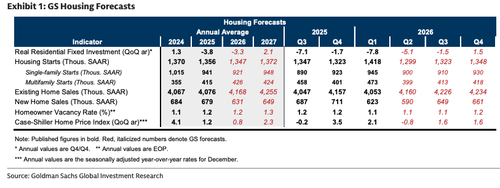

Residential investment faltered in the first half of the year on the back of particularly poor weather and a sharp rebound in mortgage rates: after declining 8% annualized in Q1, residential fixed investment fell 5% annualized in Q2, we estimate. In this Analyst, we review our key forecasts for the housing market for the rest of the year.

No Keys for Golden Handcuffs

The outlook for the economy’s most interest rate sensitive sector is largely a function of the outlook for mortgage rates. Exhibit 2 shows that mortgage rates rebounded in March in response to the Iran War, higher oil prices, and the prospect of Fed hikes. Our strategists expect mortgage rates to remain elevated for the foreseeable future, remaining around current levels (6.43%) through yearend before moderating slightly next year (6.3%), reflecting our dovish forecast for the Fed.

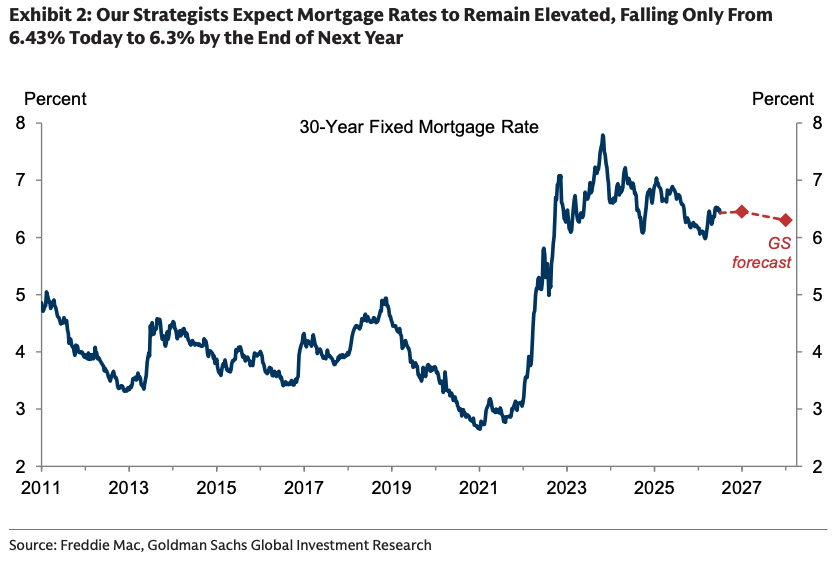

Sustained higher mortgage rates will continue to have their most pronounced impact on housing turnover. The left panel of Exhibit 3 shows that almost 80% of mortgage borrowers have interest rates below current market rates, and almost 60% have rates more than 2pp below market rates. The combination of mortgage borrowers refinancing at low rates en masse in 2020 and 2021 and the high current level of mortgage rates has created a significant financial cost to moving, as buying a new home would require homebuyers to prepay their current mortgage and take out a new mortgage at a significantly higher rate. As a result of this “lock-in” effect, we expect existing home sales to total just 4.2mn in 2026, 22% below 2019 levels but a touch above the pace of the last two years. Next year, we expect existing home sales to edge up to roughly 4.3mn, reflecting both modestly lower mortgage rates and the natural decay of the lock-in effect that comes from, for example, borrowers paying down their mortgage.

While a modest rebound in the pace of existing home sales would boost the gross supply of available homes, it would have limited implications for net housing supply and the longstanding—but moderating, as discussed below—nationwide housing shortage, as households are often simply switching between housing units and no housing units are created or destroyed. Still, turnover has meaningful implications for GDP, as more existing home sales boost residential fixed investment via brokers’ commissions (which hold a 15% weight in RFI).

Single-family Homebuilding: Slightly Less Support From the Shortage

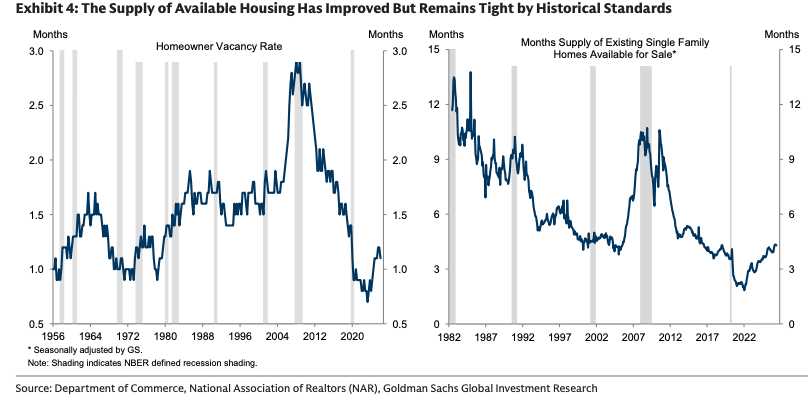

The longstanding housing shortage has kept single-family homebuilding extremely resistant to higher interest rates. The elevated pace of homebuilding in recent years has improved supply-demand balances, albeit they remain at levels that are still historically tight (Exhibit 4).

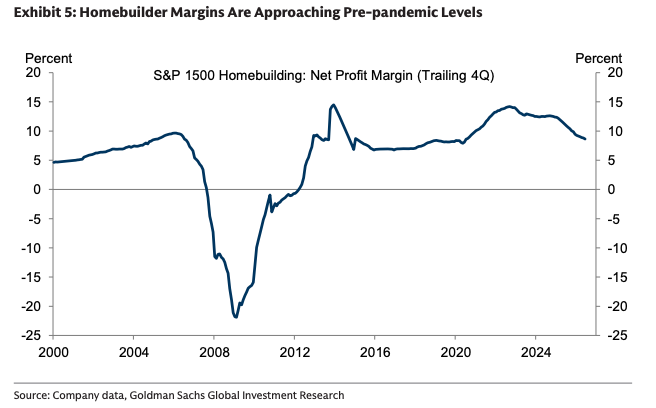

That improvement, along with the corresponding compression of margins for homebuilders back to pre-pandemic levels (Exhibit 5), has contributed to a moderate slowdown in single-family housing starts. Single-family starts have declined by 2% so far this year compared to last year but because of the still-tight housing market have averaged 4% above 2019 levels despite 3pp higher mortgage rates today. Looking ahead, we expect single-family housing starts to total 0.92mn this year (vs. 0.94mn in 2025) and to end the year around a 0.93mn annualized pace. This view is similar to the signal from equity analyst expectations, a proxy for corporate guidance, for units delivered by homebuilders this year.

We expect housing demand to remain tepid. On the positive side, domestic demographic trends remain supportive and survey-based measures of purchase intentions (such as the measure from Conference Board that asks respondents whether they plan on purchasing a home within six months) have improved over the last year.

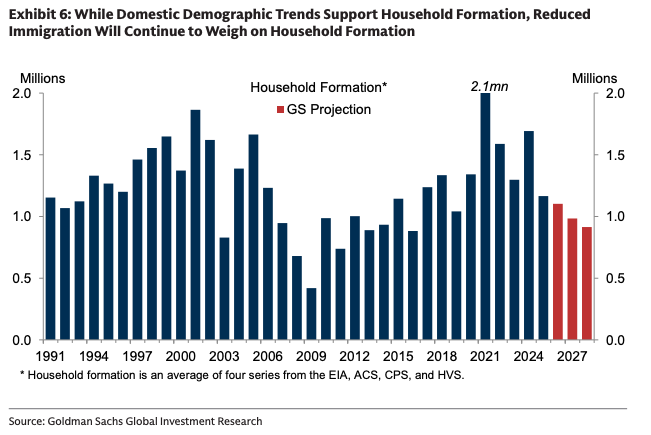

But on the negative side, income growth is poor and reduced immigration will continue to weigh on household formation. Exhibit 6 shows our model of household formation that combines projections of headship rates (the share of people who are heads of a household) by age group with Census projections of population growth by age group that we have then adjusted for reduced immigration. This approach yields an estimated rate of household formation of about 1.0mn per year for the next few years, below the recent trend.

The combination of still-elevated supply growth and slightly weaker demand should continue to push the homeowner vacancy rate higher, we estimate from 1.1% in 2026Q1 to 1.2% in 2026Q4 and 1.3% in 2027. Against the backdrop of an easing housing market, we expect national home prices to rise just 0.8% December-over-December this year and 2.3% next year.

What impact has the slowdown in immigration since 2025 had on housing supply, housing demand, and their balance

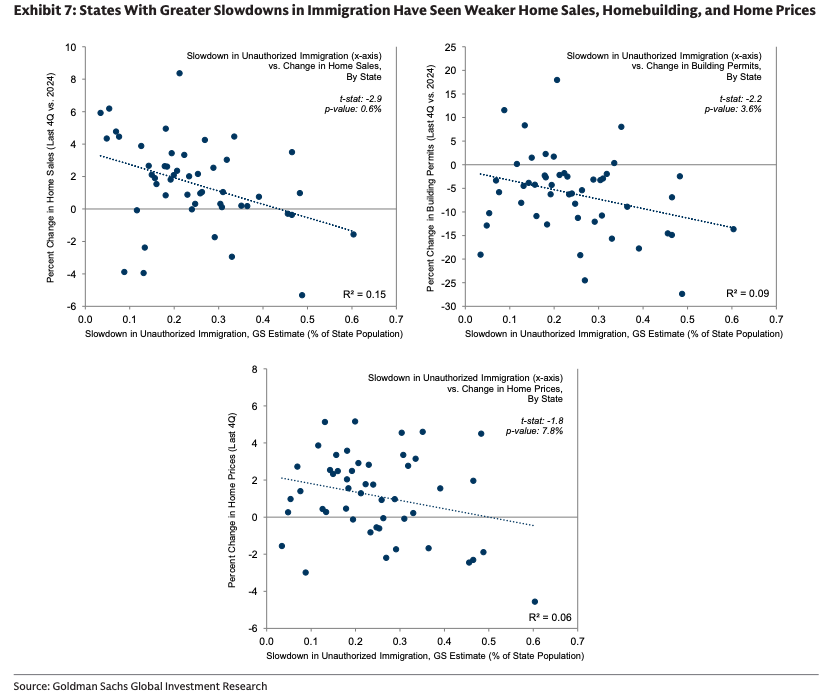

Combining our state-level estimates of unauthorized immigration based on court case data with state-level housing outcomes, we find that the states that experienced greater slowdowns in unauthorized immigration between 2024 and 2025 have had both weaker home sales and homebuilding (Exhibit 7, top panels). We also find that home price growth has been weaker in states with a greater immigration slowdown (bottom panel), suggesting a slightly greater hit to demand than supply. However, the relationship with home prices has only borderline statistical significance, and we did not find a meaningful relationship between slowdowns in immigration and changes in vacancy rates.

Separately, a Federal Reserve Bank of Dallas report adds another pressure point for many Americans already priced out of the housing market. The report suggests that the Biden-Harris regime’s open-border policies helped fuel a surge in illegal aliens, creating a housing-demand shock that contributed to faster home-price and rent growth nationwide.

Taken together, the message for prospective homebuyers is not encouraging. Goldman sees the housing market as soft but broadly stabilizing, yet mortgage rates and home prices are expected to remain elevated into next year. Meanwhile, the Dallas Fed’s findings suggest immigration-driven demand may have worsened affordability pressures.

All in, 2027 is shaping up to be another year in which affordability concerns keep millions of would-be buyers on the sidelines, delaying or denying participation in the American dream of homeownership.

Tyler Durden

Wed, 07/08/2026 – 06:55

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}