The Weimar Inflation Revisited

Authored by Jeffrey A. Tucker via The Epoch Times (emphasis ours),

Lots of thinking these days about Rome and its fall. Maybe we should be thinking about Weimar and the inflation that wrecked Europe.

Following the Great War, now known as World War I, the victorious allies forced the abdication of Kaiser Wilhelm II, who would be the last German emperor, and thus ending a 300-year dynasty that had ruled Prussia. The Weimar Republic was born as a new experiment in democracy. The result was utterly catastrophic for the country and the world. The trigger was war reparations and the means by which they were paid.

“The depreciation of the mark of 1914–23,” wrote the brilliant economist Lionel Robbins in 1937 (therefore two years before World War II) “is one of the outstanding episodes in the history of the twentieth century. Not only by reason of its magnitude but also by reason of its effects, it looms large on our horizon. It was the most colossal thing of its kind in history: and, next probably to the Great War itself, it must bear responsibility for many of the political and economic difficulties of our generation.”

“It destroyed the wealth of the more solid elements in German society,” he wrote, “and it left behind a moral and economic disequilibrium, apt breeding ground for the disasters which have followed. Hitler is the foster-child of the inflation. The financial convulsions of the Great Depression were, in part at least, the product of the distortions of the system of international borrowing and lending to which its ravages had given rise. If we are to understand correctly the present position of Europe, we must not neglect the study of the great German inflation. If we are to plan for greater stability in the future, we must learn to avoid the mistakes from which it sprang.”

Consider the prescience here. It was not possible for Robbins or anyone to anticipate the ghastly scale of destruction of Europe that would follow in the coming years. The costs of the Nazi political movement were very apparent. The full implications were inconceivable.

What is this inflation to which he refers? Sadly, it is hardly understood today, even though, as Robbins said, it was then “the most colossal thing of its kind in history” until that point.

My first exposure to the historical incident came when looking through the bookshelf of my college roommate. He had a book called “The Age of Inflation” by Hans Sennholz. The chapter on this episode is precisely what led me to study economics. It made the point: economics is a technical science but with profound implications on all of human societies and life.

Since then I found this masterwork: “The Economics of Inflation,” by Constantino Bresciani-Turroni, professor of economics at the University of Milan, published in 1931 and later translated into English. It’s a hugely important book, the first and probably still the most definitive work on the topic. What he covers in some technical detail is a turning point in the history of civilization.

Let’s back up before the Great War when this all began. Enamored of the prospects for scientific economic planning and the rise of new technologies, governments of the West created what were called central banks. They began in Germany but were quickly copied by England and finally the United States. The idea of the central bank was to end the banking crisis, smooth out the business cycle, and, if you can believe it, finally conquer the problem of inflation.

The trouble was that central banking gave governments a new tool they had never had in the modern age: the ability to print their way out of new levels of spending without having to resort to taxation. The tariff had fallen out of favor as a revenue stream and the income tax was then very low, so the printing press offered quite the temptation. Or we might just say it: it was a moral hazard.

The traditional way of settling conflicts between nations was diplomacy. War was and is costly, and the citizens won’t shell out unless they are convinced it is essential to national security. In the 1910s, with central banks available to make up the difference, new national conflicts could too easily turn to a shooting war. The old multinational monarchies had broken down in any case, and the burning question of what would replace them was everywhere present. In addition, government had other new tools: new forms of munitions, the potential for air combat, larger guns and bombs, and even poison gas. There was an itch in politics to try them out, and the central banks stood in wait to make it all possible.

During the Great War, every major power resorted to the printing press but Germany even more than the others. Upon defeat, the German currency was already weak. Once presented with the rough peace terms of Versailles in 1919, which required that Germany pay reparations in hard currency, gold, or gold-backed marks, the temptation to run the presses proved too great.

This is when the action really began. German industry and agriculture were seriously in debt, and the post-war government was in constant negotiations with war victors. As a result, they turned to the printing press, and ultimately drove the full demise of the currency and the society behind.

But that was not the first effect. The first effect was a wild economic frenzy of 1920 in which the stock market boomed 70 percent over the course of one year. There was no shortage of jobs, no shortage of chances to make money, no limits to speculative opportunities. It seemed at that time like money itself would save Germany when everything else had failed.

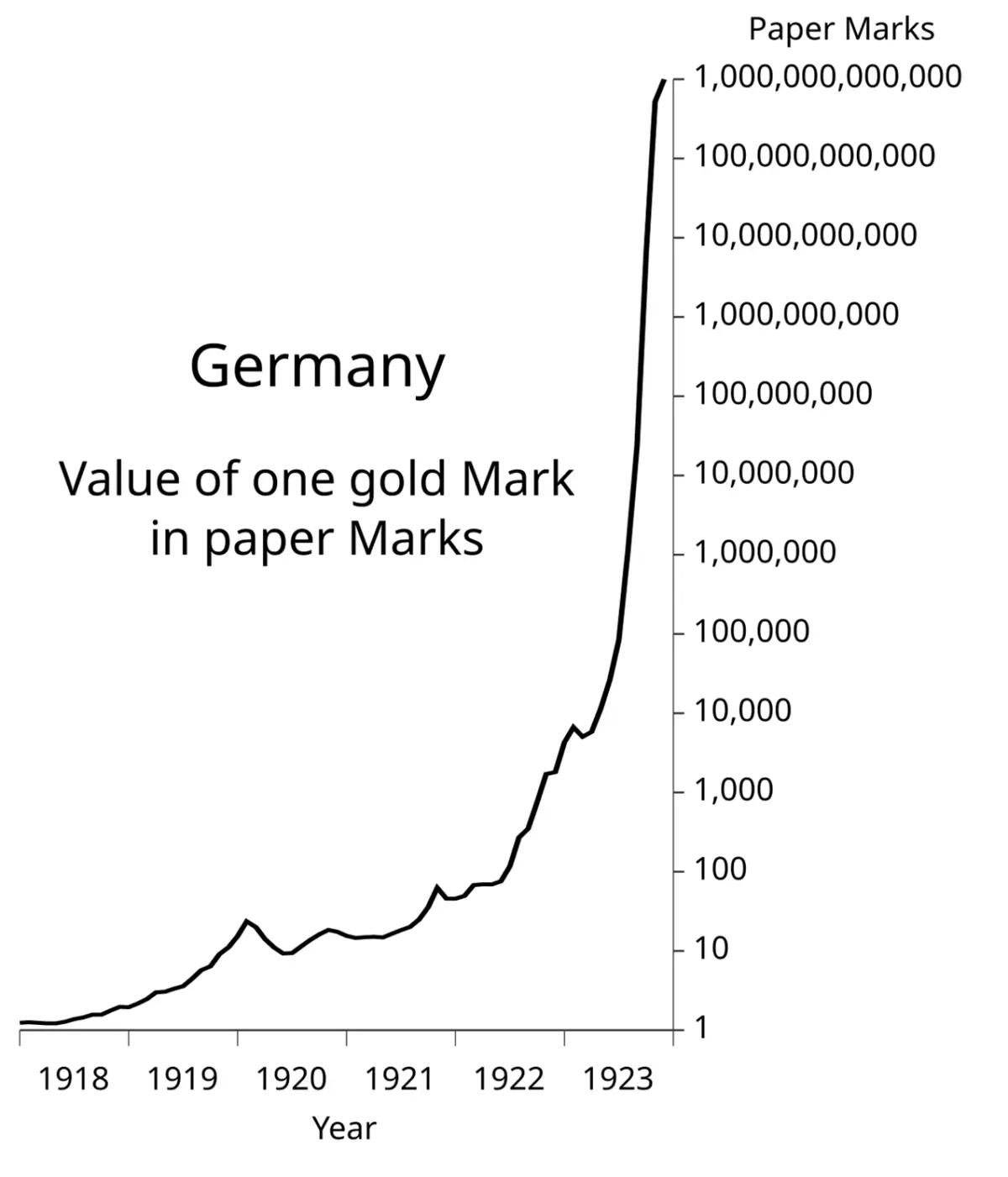

That sense of frenzy and excitement did not last as monetary depreciation set in, slowly at first and then with a fury never before seen in modern times. It picked up in 1921 but raged through all things in 14 months between late 1922 and the end of 1923, during which time a loaf of bread went from 160 marks to 200 billion marks. That is to say, the currency was worth less than the paper on which it was printed.

Stories include people carrying paper money in wheelbarrows to the store, only to have the wheelbarrow stolen and the money left on the table. In the winter of 1923–24, it was commonly used as heating fuel.

Bresciani-Turroni comments:

“There is no doubt that the paper inflation would not have assumed such vast proportions if it had not been favored in many ways by the people who drew a large profit from it. It is clear from the discussions held in 1922 and 1923 in the Economic Council of the Reich, that representatives of those classes used their influence on the Government to impede the reform of the public finances and to sabotage all proposals for the stabilization of the German exchange, which they only accepted when, at last, an economic catastrophe threatened Germany and it was evident that the consequences of the inflation would rebound against their authors. Without making the exaggerated statement that the depreciation of the mark was due to a conspiracy of the industrial classes, it is certain, nevertheless, that they contributed largely to it, aided by the agriculturists who saw the lightening of the burden of their mortgages, which before the war was very heavy, and by all the other people who prospered owing to the continued depreciation of the national money. Such obvious and conspicuous advantages for producers could be derived from this phenomenon, that naturally they became the most convinced supporters of monetary inflation.”

The effect on politics was devastating. The draft and war had already slaughtered many young men, and left wounded survivors with a demoralized sense of how the system works. No one believed anymore in much of anything. They had survived on patriotism for years but now that had collapsed in the face of evidence that the old regime had led the country to ruin. The moral compass of the country was largely shattered, and institutions of faith bankrupted, and the once-robust cultural infrastructure briefly replaced by a brief confidence in money-making.

The money failed, shockingly and abruptly. When that was gone, the culture was hungry for a new answer and a scapegoat for the terrible sufferings. Hitler easily stepped into the breach with a full story of the racial heroics of the Aryan race and a wickedly cruel demonization of Jews as a people. A full 15 years passed before the second world war broke out, leading to another and worse round of ruin for the country and the world.

The lesson from this experience in Germany brought about a postwar dedication to tight money and a strong German currency. With European monetary integration, even this began to fade, and the European Central Bank joined the Federal Reserve in the great money-printing bonanza of 2020–21, fully one hundred years following the trigger of the greatest calamity of the century.

Our author concludes as follows. The great German inflation “annihilated thrift; it made reform of the national budget impossible for years; it obstructed the solution of the Reparations question; it destroyed incalculable moral and intellectual values. It provoked a serious revolution in social classes, a few people accumulating wealth and forming a class of usurpers of national property, whilst millions of individuals were thrown into poverty. It was a distressing preoccupation and constant torment of innumerable families; it poisoned the German people by spreading among all classes the spirit of speculation and by diverting them from proper and regular work, and it was the cause of incessant political and moral disturbance. It is indeed easy enough to understand why the record of the sad years 1919–23 always weighs like a nightmare on the German people.”

The history and practice of monetary policy is not ancillary to history but central. The Weimar-Era inflation is Exhibit A. This is not ancient history.

It’s also true that many countries in the world experienced suffering from their wartime money printing, including the United States. From 1915 and following, the United States dealt with serious inflation and finally a recession from 1921 to 1923 that knocked 8.7 percent off the gross domestic product (GDP).

The Coolidge administration responded by letting the correction happen with no major fiscal or regulatory interventions. By the following year, economic recovery was underway. This is the model, the proper way to fix man-made economic problems: first stop making more problems.

Would that all governments followed this path, then and now.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Tyler Durden

Wed, 07/17/2024 – 05:00

https://www.zerohedge.com/geopolitical/weimar-inflation-revisited

{kind=link}

{kind=link}