The Yield Curve & Christine Lagarde Agree… Don’t Expect A “Soft Landing”

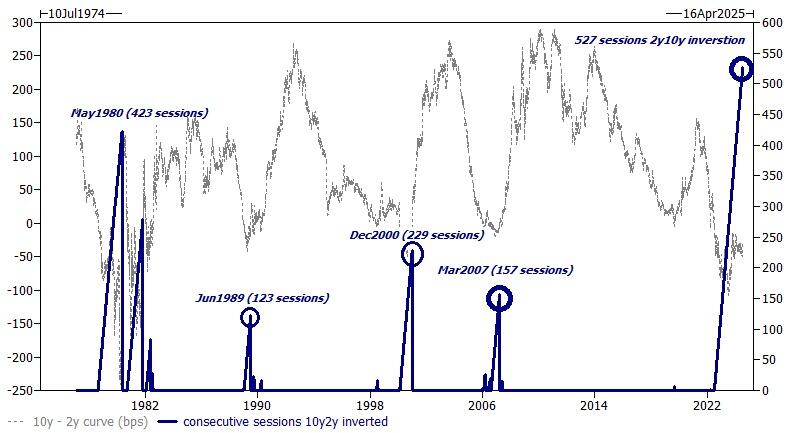

An inverted Treasury yield curve has historically been associated with economic downturns, preceding every recession since the late 1960s.

Earlier this year, it set a new record for remaining inverted for more than 527 days, which was the 1980 record.

The curve has inched slightly back up but remains stubbornly inverted, and now even the Wizards of Global Finance themselves like European Central Bank President Christine Lagarde are warning against assuming a “soft landing” is anything but assured for the global economy.

10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity

In fact, a crash is feeling more likely by the day.

The yield curve hasn’t remained this inverted overall since the Great Depression. Recessions reliably follow this trend, but pundits are saying that this time it’s different, because it doesn’t signal a contraction in credit as it has in the past, and stocks have rallied since the inversion began. They also say that markets have become more aware of the yield curve and priced it in, reacting with cutbacks before the “real” recession sets in and forces more pain.

With a massive wave of commercial mortgage loans set to mature between 2024-2025, and record numbers of empty office buildings in American cities with little hope of finding occupants, there are at least $1.2 trillion dollars worth of reasons to be concerned.

It’s not just the US, either. The yield curve on Canadian bonds has been inverted as well, with persistent inflationary pressures remaining despite Canada’s central bank recently making the decision to cut rates. In the UK, the yield curve just recently flattened out after being inverted for over a year.

Historic inversion of the yield curve is not just a US phenomena.

Canada Yield Curve also at historic levels. No, 25 bps does not fix this 👇 pic.twitter.com/WRpabxfiuP

— James E. Thorne (@DrJStrategy) July 10, 2024

Unsurprisingly, Jerome Powell just ruled out a summer rate cut, citing “modest progress” on inflation. “Higher for longer” monetary policy won’t be enough to bring prices back down, but the Fed will defy expectations if it still doesn’t cut at its FOMC meeting in the fall since industries like commercial real estate and, by extension, banking itself, can’t handle elevated interest rates without imploding under the pressure of even a slightly elevated cost of borrowing. Rate cuts will then make inflation worse as the dollar tanks.

The yield curve ticked up after Trump debated with Biden, which shook up the 2024 race and fueled expectations that a Trump win was possible, leading to higher demand for yield on long-term bonds. That’s because investors expect larger fiscal deficits from a theoretical Trump administration, with anticipated tax cuts and spending increases.

Meanwhile, central banks and governments do everything they can to paint a rosy economic picture, hoping their words can override reality.

As Peter Schiff recently said about cooked economic reports like CPI and the recent jobs numbers:

“The real statistics— if we measured the economy the way we did prior to 1994— you can see why so many people are so miserable.”

Still, the spin masters of finance always have a fresh set of mental gymnastics to explain away the horrors and hubris of central planning.

The inverted yield curve, and still no official recession? It must be that central planners and markets have become so wise that the yield curve no longer means anything.

But just wait a little bit longer, and then we’ll see if the pattern ultimately holds.

Tyler Durden

Sat, 07/13/2024 – 10:30

https://www.zerohedge.com/markets/yield-curve-christine-lagarde-agree-dont-expect-soft-landing

{kind=link}

{kind=link}

{kind=link}