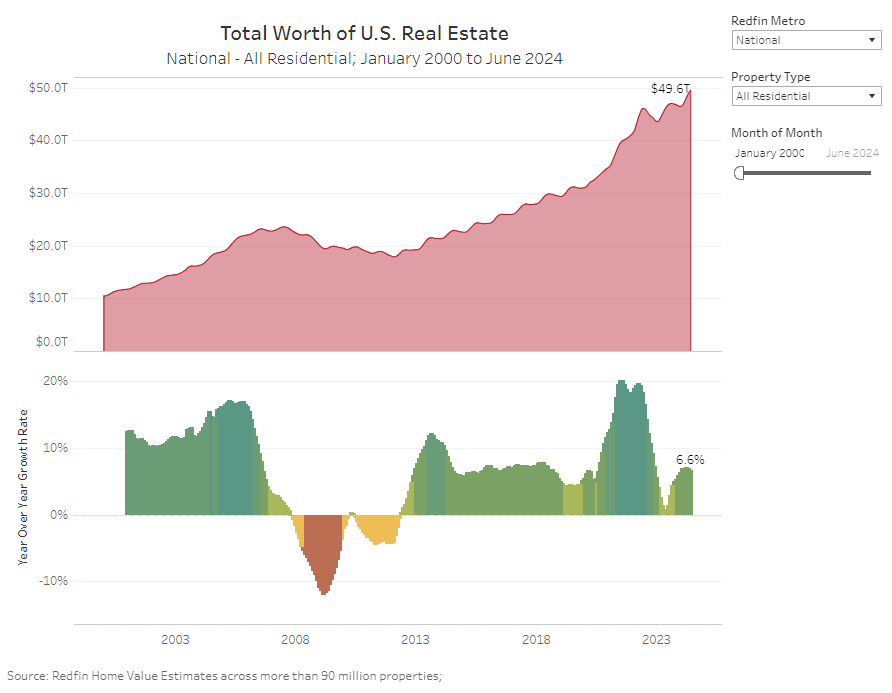

Value Of US Housing Hits Record $50 Trillion, Up 7% In Past Year, Just In Time For Fed Rate Cuts

The Fed’s rate hikes were supposed to slow down the economy and, thanks to soaring interest rates, lower prices and make housing more affordable. That did not happen, and instead housing is now the least affordable it has been in US history.

And while an entire generation of potential buyers will be forced to rent indefinitely, the flip side is that anyone who has been lucky enough to buy a house, is celebrating on a day real-estate brokerage Redfin reports that the total value of U.S homes gained $3.1 trillion over the past 12 months to reach a record $49.6 trillion.

In percentage terms, the total value of the US housing market grew 6.6% year over year, laughing in the face of a Fed chair who kept on hiking rates in hopes of lowering prices. Zooming out further, the total value of U.S. homes has more than doubled in the past decade, climbing nearly 120% from $22.7 trillion in June 2014.

“The value of America’s housing market will likely cross the $50 trillion threshold in the next 12 months as there are not enough homes being listed to push prices down,” said Redfin Economics Research Lead Chen Zhao. “Mortgage rates have started falling, but many potential sellers and buyers are waiting to make a move, meaning we are likely to continue seeing a pattern where prices slowly tick up. That’s great news for the millions of American homeowners who see their equity rising, but first-time buyers are going to keep finding it tough to find an affordable home.”

That, of course, is an understatement: what Zhao meant is that for millions of Americans, the dream of owning a home is now gone for ever, because if they couldn’t afford to buy a house during the most aggressive rate hike cycle since Volcker, the coming rate cuts will certainly not make it easier.

The number of metros where the total value of homes topped $1 trillion grew to eight—doubling from four a year ago—with Anaheim, CA, Chicago, Phoenix and Washington, DC, joining New York, Los Angeles, Atlanta and Boston in the trillion-dollar club. San Diego and Seattle look like they will join them in the next 12 months if home values keep increasing at a similar pace.

It’s worth noting that while San Francisco’s aggregate home value is roughly $700 billion, when combined with neighbors Oakland, CA, and San Jose, CA, the combined Bay Area housing market is worth nearly $2.5 trillion. Likewise, the combined Dallas ($734 million) and Fort Worth, TX ($294 million) metro area also surpasses the $1 trillion mark.

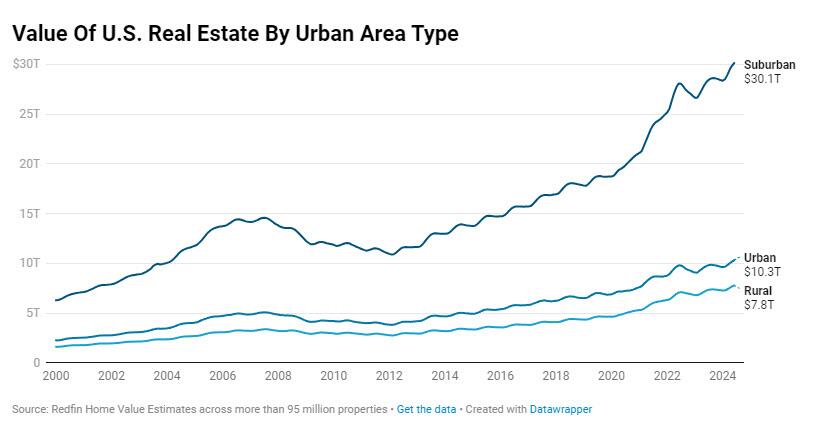

Rural home values outpaced those in urban areas and the suburbs, jumping 7% year over year to $7.8 trillion. The total value of homes in urban areas rose 6% to $10.3 trillion, while the value of homes in the suburbs cracked the $30 trillion mark for the first time, increasing 6.8% to $30.1 trillion.

There are around 57 million homes in the suburbs, compared to 22 million in urban areas and 21 million in rural areas.

Thirteen major metros posted double-digit percentage gains in total property value over the last year, led by relatively-affordable New Jersey metros within commuting distance of New York, where property is more expensive. The value of properties in New Brunswick, NJ rose 13.3% to $582.6 billion, while Newark, NJ climbed 13.2% to $406.2 billion. Anaheim, CA (up 12.1% to $1.1 trillion), Charleston, SC (up 11.8% to $188.9 billion) and New Haven, CT (up 11.8% to $91 billion) rounded out the five metros with the highest gains.

Cape Coral, FL was the only metro to record a fall in total home value, dropping 1.6% to $204.2 billion. Sun Belt metros—especially those in Texas—grew slower than those in other regions, with New Orleans (up 0.8% to $128.2 billion), Austin, TX (up 1.9% to $392.8 billion), North Port, FL (up 2.1% to $251.8 billion) and Fort Worth, TX (up 2.3% to $293.7 billion) rounding out the bottom five metros.

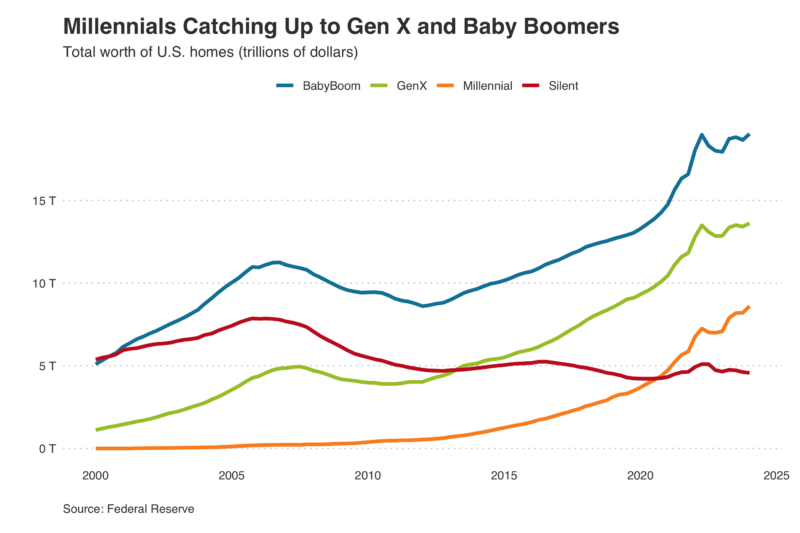

Broken down by age group, the total value of homes owned by millennials rose 21.5% year over year to $8.6 trillion in the first quarter of 2024—the most recent period for which generational data is available—nearly four times as fast as any other generation.

The increase is partly due to the overall growth in home prices, but also because millennials are now the largest generation by population and have reached an age and financial position where they make up a larger share of the homebuying market. Around two-thirds of the mortgages taken out in 2023 were issued to homebuyers under the age of 45.

Meanwhile, the total value of homes owned by the Silent Generation fell for the fifth straight quarter, dropping 1.6% to $4.6 trillion. The value of homes owned by baby boomers increased 6.1% to $19 trillion, while Gen X home values rose 5.9% to $13.6 trillion.

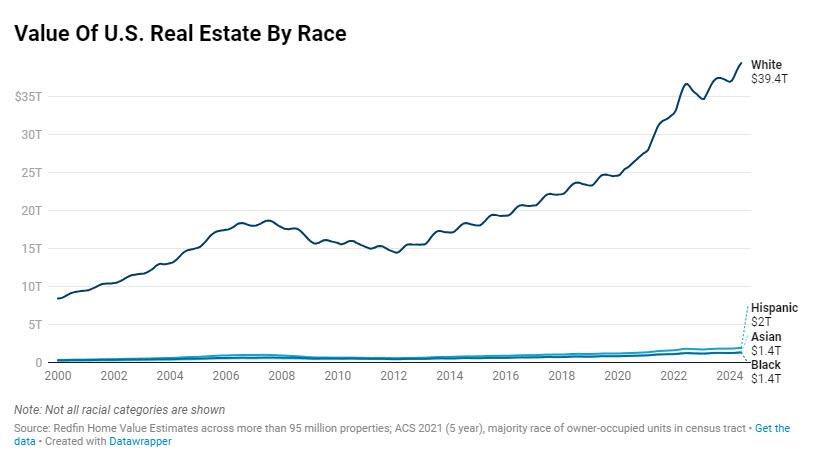

Finally, Asians once again made the best decisions, and after falling in 2022-2023, the total value of homes in neighborhoods that are majority Asian bounced back over the past 12 months, rising 9% to $1.4 trillion. The increased value is being caused by price growth in West Coast cities—where many Asian neighborhoods are located. In comparison, majority white neighborhoods experienced a 6.6% increase in value to $39.4 trillion, while majority Black neighborhoods saw a 5.4% increase in value to $1.4 trillion. The value of homes in majority Hispanic neighborhoods increased 6.4% to $2 trillion.

More in the full report available here.

Tyler Durden

Thu, 08/08/2024 – 19:40

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}