Latest News

“No Change In Middle East Policy”: Biden Deliver Unscheduled Remarks Over Campus Protests

“No Change In Middle East Policy”: Biden Deliver Unscheduled Remarks Over Campus Protests

Update: Sure enough, it is about the protests, which apparently have had zero impact on anything as expected:

*BIDEN: RULE OF LAW, FREEDOM OF SPEECH MUST BOTH BE UPHELD

*BIDEN: DISSENT MUST NEVER LEAD TO DISORDER, DENIAL OF RIGHTS

*BIDEN: RIGHT TO PROTEST DOESN’T MEAN RIGHT TO CAUSE CHAOS

*BIDEN: NATIONAL GUARD SHOULD NOT INTERVENE ON CAMPUS PROTESTS

*BIDEN: NO CHANGE IN MIDDLE EAST POLICY OVER CAMPUS PROTESTS

* * *

The White House has announced that President Biden will deliver unscheduled remarks at 10:30am ET (so he is already about 30 minutes late). It is unclear what Biden’s handlers will feed the teleprompter but it is a very safe bet that the university protests around the country will be a key topic… pause.

Tyler Durden

Thu, 05/02/2024 – 11:03

Hurt / The Downward Spiral

Hurt / The Downward Spiral

By Michael Every of Rabobank

Hurt / The Downward Spiral

“I hurt myself today; To see if I still feel; I focus on the pain; The only thing that’s real”

Post-Fed, equities closed slightly lower yesterday (S&P -0.3%), 2-year Treasury bond yields dropped 10bps before rising slightly from that floor, and 10-years were down 11bp before ending at 4.63%, or 5bp on the day, while the US dollar dropped back below 105.5 on the DXY, with JPY seeing sharp moves. However, many are likely to emerge feeling ‘Hurt’ from what the Fed had to say.

“I wear this crown of thorns; Upon my liar’s chair; Full of broken thoughts; I cannot repair”

Notably, Fed Chair Powell said the US isn’t making sufficient progress on getting inflation back to 2%, so the FOMC will keep Fed Funds at 5.50% “for longer” until this happens: and yet he eased policy anyway. First, the Fed tapered QT more than expected, from $60bn to $25bn a month; that’s not QE, but it’s a $35bn step towards the argument made here that you can have high rates and QE simultaneously. Second, Powell downplayed inflation upside surprises –our Fed watcher Philip Marey noted acerbically, “Powell said he doesn’t see the stag or the flation”– to make clear there’s little risk of a rate hike: yet by removing that gun from the table, yields fell and equities rallied, albeit briefly. Third, if inflation ticks higher and nominal rates stay the same, as suggested, then we are going to see a lower real rate of interest at a time when financial conditions are objectively already loose, not tight.

“Beneath the stains of time; The feelings disappear; You are someone else; I am still right here”

Nominal wage growth via the Atlanta Fed was 4.7% y-o-y in March and 5.2% for job switchers, and yesterday’s ADP report said job changers got a 9.3% y-o-y pay hike vs. 5.0% for job stayers; so while some other data are more dovish, in Philip’s eyes, we are still dealing with a decelerating wage-price spiral, where the feedback between prices and nominal wages is slowing down the decline in inflation. Maybe more of the same (and easier policy?!) will work in time, but “for now, inflation seems to have a life of its own.”

Worse, Philip underlines that while he still expects two Fed cuts this year, in September and December, they won’t be cutting because of inflation, but because of rising unemployment. So, Powell will see the “stag”, not the “flation”. If markets don’t like that, and they shouldn’t, then they will be clutching their pearls at Philip also pointing out Powell has a personal incentive to cut before Election Day since Trump is not going to extend his tenure as Fed Chair; that he has acted in a political manner before; and that his current baseline scenario remains a Trump win, and an inflationary universal tariff in 2025 that stop the Fed’s cutting cycle in its tracks.

“The needle tears a hole; The old familiar sting; Try to kill it all away; But I remember everything”

Meanwhile, we saw more JPY intervention and market chatter of just how destructive it would be if CNY followed JPY lower. Yet even if Jay Powell is acting like Arthur Burns wearing a Halloween mask of Paul Volker as he tries to please the White House, US markets, and the publisher of his inevitable post-office autobiography, that only increases the flow of global capital into the US dollar and US assets. King Dollar is Johnny Cash. Those with historical market memories rightly see worrying echoes of past periods of extreme systemic stress and global volatility in that set-up. But the Fed is gonna Fed regardless, as it always does, and most especially in an election year.

“And you could have it all; My empire of dirt; I will let you down; I will make you hurt.”

That on-the-edge-of-something atmosphere is of course matched by shifts in geopolitics.

Recent news suggests that the Houthis were not boasting when they stated that they are now capable of hitting vessels as far away as the Indian Ocean. What that means is shipping opting to go round Africa rather than via the Red Sea and Suez is also vulnerable to attack. That is going to mean higher insurance premiums, and then higher freight rates, and then higher inflation. And, at worse, it could mean far worse disruption to all Asia-Europe cargo flows – or at least that on behalf of the West and Israel.

The US Congress is pushing ahead with a ban on Russian uranium imports; US graphite miners are lobbying for tariffs on Chinese exports of the same; the US, in collaboration with Australia and Japan, announced it is to work with the Philippines to reduce China’s dominance in that industry; and South Korea suggested it would like to help with AUKUS alongside Japan, so AUKUS > JAUKUS > JAUKUSK?

Ukraine is still losing key ground before new weapons arrive, and hitting Russian oil refineries in response, as Russia hits Ukraine’s gas and electricity facilities.

In the Middle East, today we should hear if Hamas accepts the latest ceasefire-for-hostages deal, with suggestions Hezbollah may then agree to retreat from parts of southern Lebanon for quiet on that front. However, the risks are clear that Hamas could walk away, Israel could walk into Rafah, and Hezbollah and Israel could stumble into war. Indeed, the latest rumor is that Hezbollah has surreptitiously relocated hundreds of key officers’ family members out of Lebanon, which bodes as well geopolitically as western airlines cancelling normal flight routes.

There’s also a signal that Saudi Arabia has agreed to normalize relations with Israel: the only question –as with Powell– being if they want to help the White House in moving before the election. This is also tied to Israel’s commitment to working towards a framework for a Palestinian state. Yet at the very least, the US is prepared to agree a NATO-style defense guarantee for Riyadh, and to transfer nuclear technology without local uranium processing. That would cement the Saudis and the UAE into the US camp, as well as to the US dollar to which their currencies are pegged. However, to think that this would end all instability in the region is naïve. One would have to be a National Security Advisor to predict such things.

Here’s the key question: can you see the sides in this new Cold War, its fault lines, and its gradual upstream-to-downstream global fragmentation of trade and capital flows?

“If I could start again; A million miles away; I would keep myself; I would find a way”

Here’s another key question: where does Europe, 20 years after it expanded to include 10 Central and Eastern European nations, sit as:

Russia advances in Ukraine and once again it was the US who stepped in to act when needed;

the Houthis threaten the Asia-Europe shipping route via Africa;

the US uses its defense umbrella to get access to nickel, and influence in Asia and the Middle East; and as the US taps its own domestic potential in graphite and uranium (at a price)?

“Closer to a 25bp rate cut in June” is nice, but not a relevant answer to this kind of ‘Hurt’ or the EU’s realpolitik downward spiral.

Tyler Durden

Thu, 05/02/2024 – 10:55

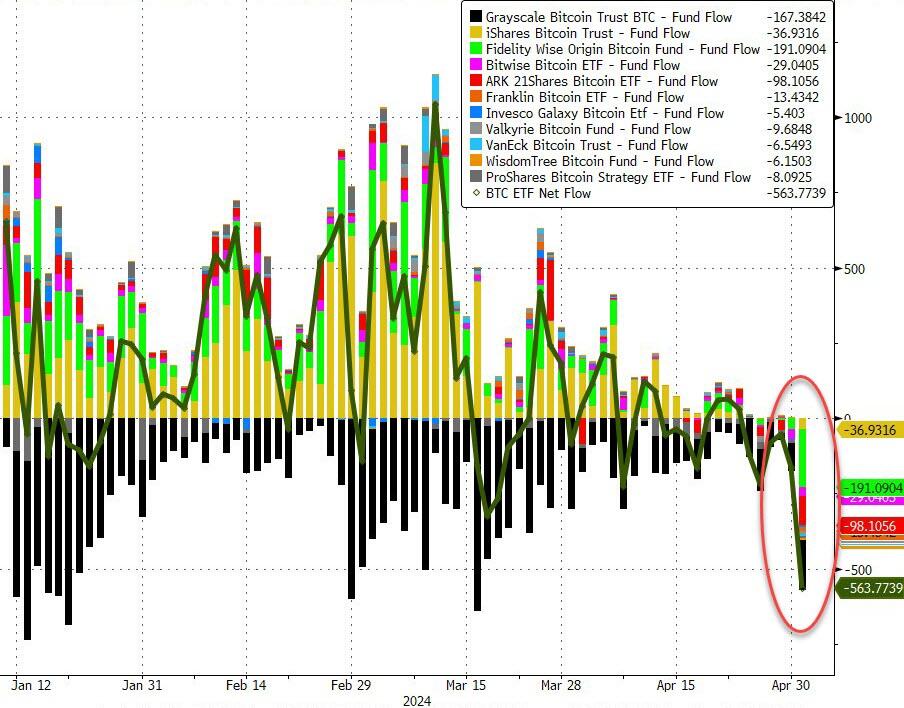

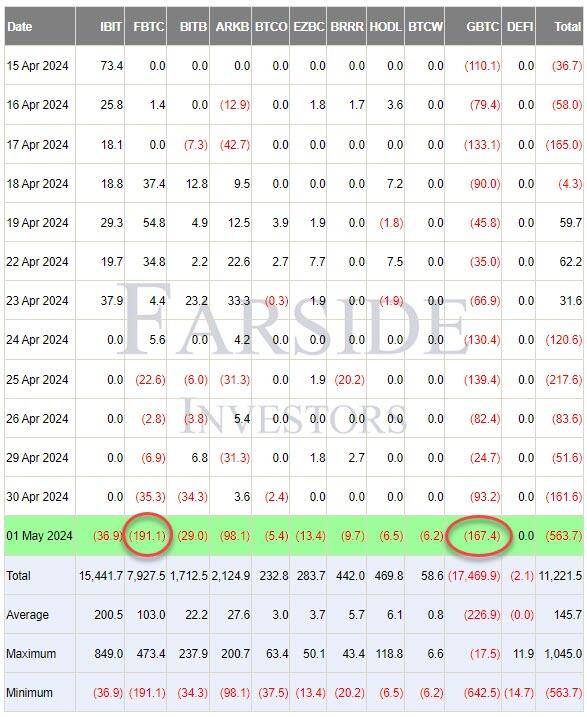

Bitcoin ETFs Suffer Worst Day Ever

Bitcoin ETFs Suffer Worst Day Ever

Despite the lack of total carnage in spot bitcoin prices, yesterday was an ugly (nay the ugliest) day for the newly minted ETFs (although bitcoin is down over 10% this week).

{kind=link}

Most notably, BlackRock’s ETF saw around $37 million in outflows for the first time, while the remaining spot Bitcoin ETFs collectively notched over $526.8 million in outflows.

{kind=link}

The largest outflow for the day was the Fidelity Wise Origin Bitcoin Fund, which saw $191.1 million in net outflows. The Grayscale Bitcoin Trust took the second spot with outflows of $167.4 million.

{kind=link}

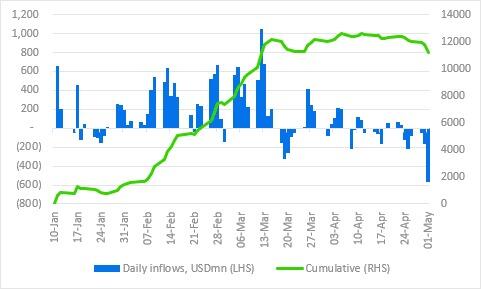

This means the total net inflow since inception has fallen to USD11.2bn.

{kind=link}

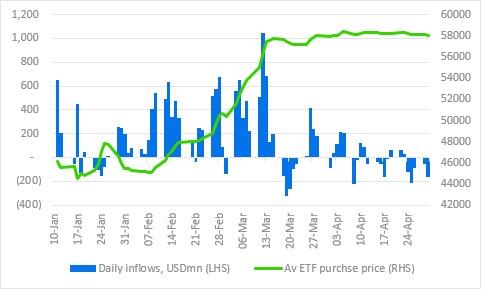

On the crypto-specific we have now had 6 days in a row of outflows from the US spot ETFs and, as importantly, we are now below the average ETF purchase price of around 58k…

{kind=link}

Source: Geoffrey Kindrick

Bloomberg ETF analyst James Seyffart noted that the Bitcoin ETFs are still “operating smoothly across the board” and that “inflows and outflows are part of the norm in the life of an ETF.”

Coinglass data shows that there has been around $200mm in ‘long liquidations’ in the last coupled of days…

{kind=link}

“Bitcoin is our favorite canary,” ByteTree Asset Management Chief Investment Officer Charlie Morris wrote in a note.

“It is warning of trouble ahead in financial markets, but we can be confident it’ll bounce back at some point.”

But this is not a time to panic, as CoinTelegraph reports, ETF Store president Nate Geraci pointed out that the iShares Gold ETF and SPDR Gold ETFs have had $1 billion and $3 billion in outflows so far this year.

Yet, gold is up 16% year-to-date, Geraci noted in a May 2 X post.

{kind=link}

As CoinDesk reports, the current lull is likely to be followed by a new wave from a different type of investor, said Robert Mitchnick, head of digital assets for BlackRock, the world’s largest asset-management company.

The coming months will probably see financial institutions such as sovereign wealth funds, pension funds and endowments start to trade in the spot ETFs, Mitchnick said in an interview. The firm is seeing “a re-initiation of the discussion around bitcoin,” which turns on the topic of allocating to bitcoin (BTC) and how to think about it from a portfolio construction perspective.

“Many of these interested firms – whether we’re talking about pensions, endowments, sovereign wealth funds, insurers, other asset managers, family offices – are having ongoing diligence and research conversations, and we’re playing a role from an education perspective,” Mitchnick said.

And finally, Geoffrey Kendrick – who correctly predicted $4k in ETH few months ago – is sticking with his 150k target for year-end 2024 and 200k for year-end 2025 (with chance of overshoot to 250k).

“The next three to four months will be less bullish and more risk-oriented, with the market closely monitoring inflation, employment and economic data for any unexpected shocks or to gain confidence about potential rate cuts,” said Youwei Yang, chief economist and vice president of crypto miner BIT Mining Ltd.

But, Kendrick notes, the next leg higher may take some time and require us to be closer to the US election.

{kind=link}

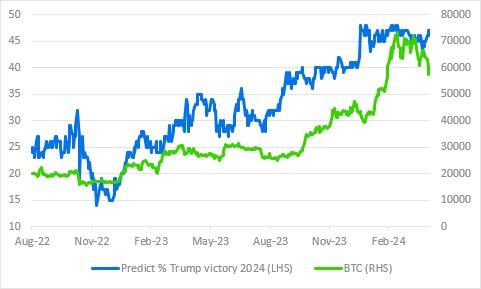

At that time we would expect BTC to rally into year-end, particularly if a Trump presidential election victory becomes more likely, as a Trump administration will be more crypto friendly than a Biden one.

Tyler Durden

Thu, 05/02/2024 – 10:35

“Safe Haven” Yen Trending Towards Zero Against Gold

“Safe Haven” Yen Trending Towards Zero Against Gold

The yen was once known as a safe-haven currency for investors to protect themselves when broader markets are shaky or other currencies are dropping, but those days are numbered. A stable government and consistent (and low) interest rates have been some of the driving factors, but it’s the unwinding of that ultra-low interest rate policy that will be the yen’s “safe haven” undoing as gold retains its protective characteristics and rockets upward.

{kind=link}

Both gold and yen have benefitted from investors looking to park their cash somewhere safe during times of high risk. But ZIRP policy in Japan has gone on for so long, that the economy can’t handle even modest upticks in the price of borrowing without triggering chaos. As seen below, the yen is currently in a freefall against gold as it hemorrhages purchasing power:

Gold’s Rise Against the Yen

{kind=link}

Source: Bloomberg

If this is what happens with 0-0.1% interest rates, imagine what would happen if they ticked up to even a modest 1%, much less the drastically higher rates that would be set by the free market if a central bank wasn’t pulling the levers.

And despite once being known as correlated with gold, since Japan began ticking interest rates up, the divergence between the two alleged “safe havens” has been decisive and dramatic:

#Gold Price in Japanese Yen vs Yen/USDollar Since 1970 (Apr. 23, 2024) – via https://t.co/NjtSzxxNhA pic.twitter.com/7SkCZ6wqM3

— 🇪🇺 🇲🇨🇨🇭Dan Popescu 🇫🇷🇮🇹🇷🇴 (@PopescuCo) April 24, 2024

Now at a 34-year low, the rumors are swirling that the Bank of Japan may intervene to prop up the yen. Stuck between a rock and a hard place, they’ll have to keep letting bond yields increase to attract foreign investment, which puts upward pressure on EU and US bonds as well. And even as it currently stands, neither the European Central Bank nor the Fed can afford their interest payments without borrowing even more money.

Since the start of the year, yields on 10-year Japanese bonds have kept going up.

Japan Government Bonds: 10-Year Yields in 2024

{kind=link}

Source: Bloomberg

Japan is also the largest holder of U.S. Treasury securities, to the tune of over $1 trillion, and may be forced to start selling its holdings to keep the yen from totally imploding. If Japan dumps Treasurys to save the yen, yields will tick higher and incentivize the yen carry trade. It won’t save Japan’s collapsing currency. And with high inflation that global central banks won’t be able to reign in, nothing will stop gold’s continuing upward trend against fiat money.

Of course, the US will do everything in its power to stop Japan from offloading US Treasurys — including firing up a new round of QE. With the Bank of Japan trapped, the only “solutions” they have, and the only responses foreign central banks can take, all lead to vicious cycles that will rip through the system and crush the global economy.

The collapsing yen is a set-up for a bond collapse doom-loop to finally begin in earnest. In the US, since the Fed would rather further devalue the dollar than have to raise interest rates enough to stimulate saving over borrowing, inflation has nowhere to go but up. Central banks in Japan and the US are both trapped, partially by themselves and partially by one another.

Rather than let Treasury yields go too high, the Fed would rather start printing money even as it acknowledges that inflation is far from under control. As Peter Schiff said in his recent interview with Anthony Crudele:

“…rather than a winning inflation fight that would cause a severe financial crisis and force the US government to default on its debts and cut spending, the Fed is going to monetize debt…to prevent those political choices from having to be made.”

The yen is beyond saving, and gold will outperform it even if the BoJ manages to narrow the gap in the shorter term. But both the yen and USD will be left in the dust as they ultimately trend toward zero in the long term relative to the yellow metal.

Tyler Durden

Thu, 05/02/2024 – 10:15

US Factory Orders Rise In March… But February Saw Yet Another Downward Revision

US Factory Orders Rise In March… But February Saw Yet Another Downward Revision

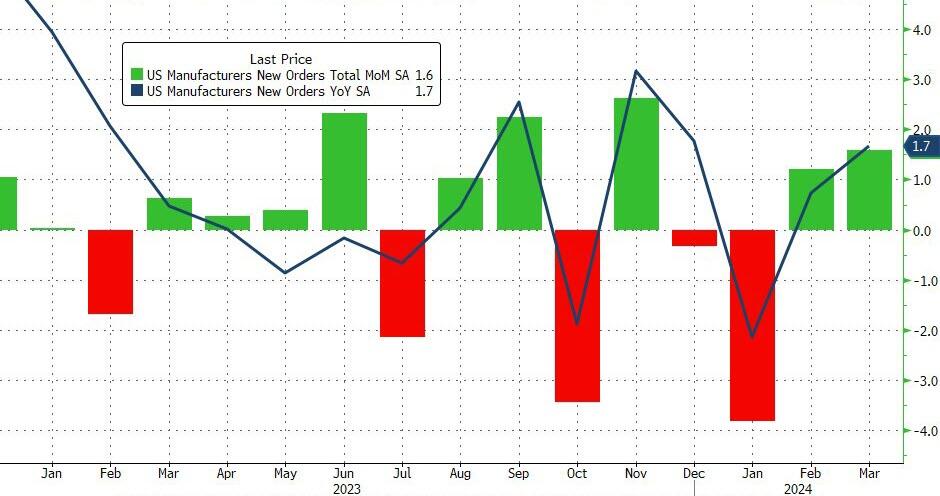

The roller-coaster ride of US durable goods and factory orders continued in March (final data just released) as the flip-flopping data series

Having plunged by the most since COVID lockdowns in January, US factory orders continued to accelerate in March, +1.6% MoM (as expected) – but February was revised lower… again. This pushed the YoY factory orders up 1.7% (nominal)…

{kind=link}

Source: Bloomberg

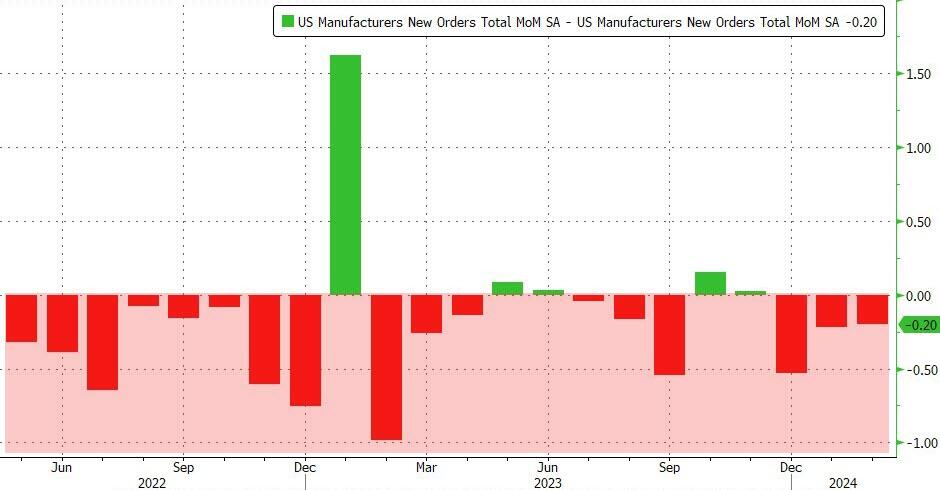

This is the 17th monthly downward revision in the last 22 months… come on!!!

{kind=link}

Source: Bloomberg

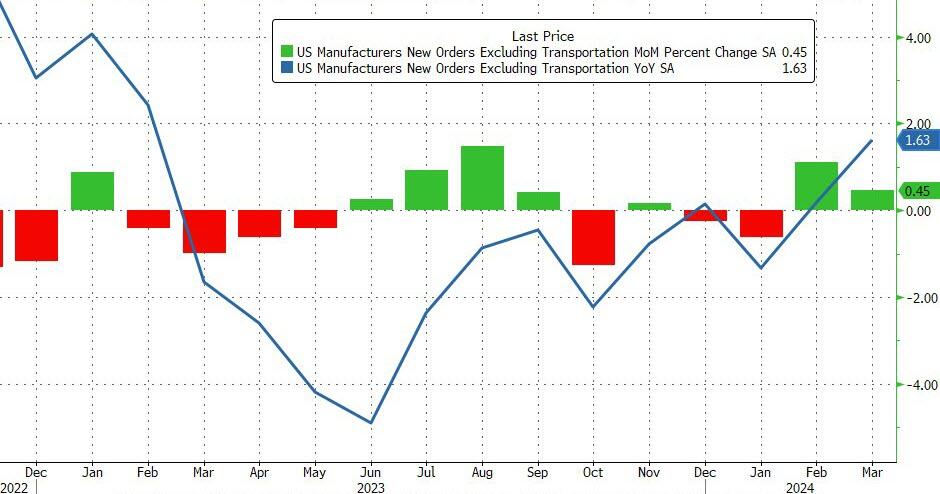

Core Factory Orders also rose MoM (+0.5% vs +0.2% exp)…

{kind=link}

Source: Bloomberg

The final durable goods orders data prints for March were in line with the preliminary data but more problematically – Capital Goods Shipments Non-Defense Ex-Air was flat MoM, downwardly revised from the initial print…

{kind=link}

Source: Bloomberg

…strongly suggesting the capex cycle is stalling.

Tyler Durden

Thu, 05/02/2024 – 10:11

‘Unity’: Pro-Israel And Pro-Palestine Supporters Chant “F**k Joe Biden” In Solidarity As Democrats In ‘Panic Mode’

‘Unity’: Pro-Israel And Pro-Palestine Supporters Chant “F**k Joe Biden” In Solidarity As Democrats In ‘Panic Mode’

How it started:

{kind=link}

How it’s going:

Biden finally managed to unify the country https://t.co/Oppf7ssAXn

— zerohedge (@zerohedge) May 2, 2024

In early March, President Biden and the Democrats called for the “Unity of all Americans.”

Fast forward to the Marxist revolution spreading like stage four cancer at the nation’s colleges and universities, anti-Israel and counter-protesters found common ground, or perhaps a glimpse of solidarity, when both sides were heard chanting “F**K Joe Biden” this week at the University of Alabama.

“It finally happened. Joe managed to get both sides of the protest to hate him for different reasons,” X user Alex The Ghost wrote.

It finally happened. Joe managed to get both sides of the protest to hate him for different reasons @ShamashAran @ClairNova4k @Carlkeck1 @DefiantlyFree @Piper010100 @Katie_likes_it @ImissPresTrump @CreativeVerveM

— Alex The Ghost (@GhostOfAlex1) May 2, 2024

Others on X agreed…

See, he really did unify the country.

— Jason Lambeth (@JLambo79) May 1, 2024

Finally!

America agrees on one thing!

— flyby (@Barbara88625178) May 1, 2024

He’s finally found a way to unite the country after 3.5 years. Bravo. pic.twitter.com/t3L9weU4c7

— Shooting News Weekly (@SN_Weekly_) May 1, 2024

Finally something we can all agree on. Thanks Joe.

— Bernard (@BBD100) May 2, 2024

The president and the radical left are walking a very fine line between supporting the Marxist kids at schools and their right to protest while simultaneously denouncing antisemitism. The surge in criticism from both the left and the right of the elderly president’s Israel policy risks the unity of both sides in their hatred of the president.

Meanwhile, Axios reports Democrats are in full-blown’ panic mode’ behind the scenes as campus takeovers by extremists of their own party produce terrible optics ahead of the presidential election in November.

“The longer they continue, and the worse that they get, the worse it’s going to be for the election overall,” one House Democrat said.

The House Democrat warned that school chaos will only “bring out [the public’s] most conservative side.”

What’s clear is that campus protesters are becoming a political liability for Biden and Democrats.

{kind=link}

Republicans are now seizing on the opportunity from New York to California to inform voters that under this administration, the destruction and chaos of America continues. Add this chaos to the long list of failures by the Biden administration, including the migrant invasion, worsening drug overdose crisis, violent crime proliferating across metro areas, disastrous foreign policy moves in Eastern Europe and the Middle East, risking World War III, and, of course, the failure of Bidenomics that has ignited stagflation, crushing America’s middle class.

“[Democrats] were trying to make a big deal out of these Trump trials, but they’ve taken a back seat” to the protests, John Feehery, a Republican strategist and former congressional aide, told Financial Times.

This week, the White House has been awfully silent on the campus takeover crisis.

“When will the president himself, not his mouthpieces, condemn these hate-filled little Gazas?” Tom Cotton, the Republican senator from Arkansas, told reporters on Wednesday.

“President Biden needs to denounce Hamas’ campus sympathizers without equivocating about Israelis fighting a righteous war of survival,” Cotton added.

A recent poll showed that 81 percent of voters aged 18 to 35 disapprove of Biden’s handling of the conflict in the Middle East.

Michael Moore, who correctly predicted Trump’s victory in 2016, even issued a plea to Biden urging him to accomplish a ceasefire or face defeat.

“We’re going to lose the election. We’re going to lose Michigan if we don’t turn this around. If President Biden doesn’t turn this around, that is going to do more to put Trump back in the White House. And I refuse to have Donald Trump back in the White House,” said Moore.

To sum up, the Democrats are in serious trouble if anti-Israel protesters and counter-protesters begin to march in solidarity around their hatred of Biden.

Tyler Durden

Thu, 05/02/2024 – 09:35

US Traders Took Powell’s Pivot More Seriously Than Foreigners

US Traders Took Powell’s Pivot More Seriously Than Foreigners

Authored by Simon White, Bloomberg macro strategist,

Most of the hawkish tilt in yields and rise in Federal Reserve interest rate expectations this year has come in non-US trading hours. A dovish repricing would therefore require (other things equal) a change of trading direction only in overnight hours when volumes are typically lighter.

US yields have risen steadily since their end-of-December lows. Expectations the Fed was going to make over six rate cuts has dwindled down to barely one. The risk-reward now favors a dovish repricing as liquidity conditions are set to worsen as the year goes on. And that is more likely to come from domestic trading rather than from abroad, if recent history is anything to go by.

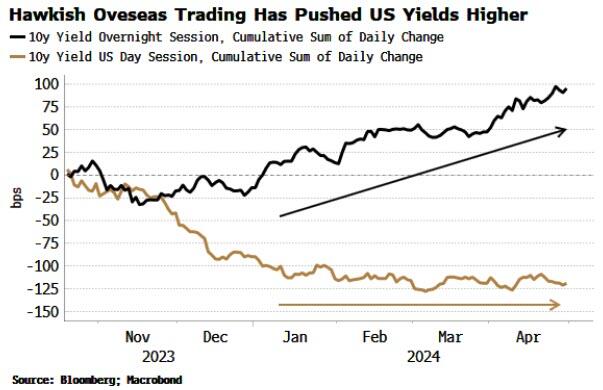

We can get hourly data going back to October for US Treasuries and fed funds futures, and separate it out into a US day session and an overnight session (both contracts trade 22-23 hours a day). The chart below shows the cumulative sum of the daily change in the day session and the overnight session for the 10-year yield. This year, almost all of the rise in 10-year yields has taken place in non-US trading hours.

{kind=link}

Making the assumption that it’s predominately US-based volumes driving trading in US hours, US-based traders pushed yields lower from their October peak. But there has been little further movement all of this year. In contrast, predominately overseas trading (and no doubt some US-based algos and insomniac traders) has pushed the 10-year yield higher all this year – driving the 80 bps rise in the 10y in 2024.

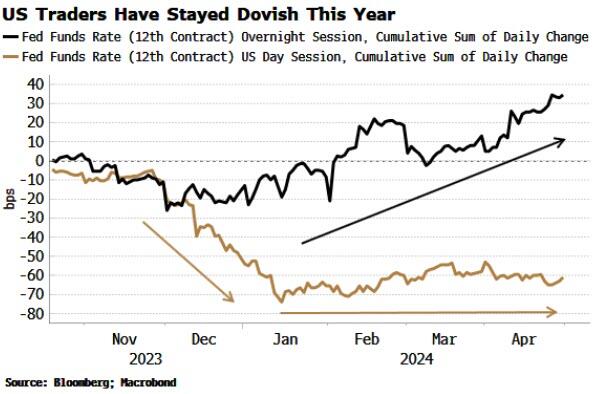

The delineation between US and non-US trading is even more pronounced when looking at Fed rate expectations. The chart below is the same as the one above, but with the twelfth generic fed funds future, which gives an approximation for what’s priced for the Fed in ~12 months’ time.

Here we can see US-based trading drove the proliferation of rate cuts expected at the end of 2023. Since then, US-based traders have not changed their dovish view.

Almost all of the hawkish tilt this year – eradicating most of the cuts expected – came in trading during non-US hours.

{kind=link}

It looks like mainly US-based traders took Powell’s pivot in December more seriously than those predominately based abroad. Either way, risk-reward now favors siding with the domestic team for a more dovish rate outcome than is currently priced.

Tyler Durden

Thu, 05/02/2024 – 09:15

Unit Labor Costs Soar In Q1 As ‘AI Productivity Boom’ Fails To Show Up

Unit Labor Costs Soar In Q1 As ‘AI Productivity Boom’ Fails To Show Up

Remember how AI was going to save the world, give us all more leisure time because of its massive boost to productivity?

Well, in Q1 in the US… it failed to show up as non-farm productivity – or nonfarm employee output per hour – rose at a measly 0.3% annualized rate after an upwardly revised 3.5% gain in the prior period (well below expectations)…

{kind=link}

Source: Bloomberg

On the flip-side of that – and echoing the market-worrying ECI data earlier this week – Unit Labor Costs soared 4.7% in Q1 (well above the 4.0% expected and the 0.4% rise in Q4)…

{kind=link}

Source: Bloomberg

So wage inflation is confirmed – rising at the fastest pace in a year – as all the gains we have been told to expect from AI just aren’t there in the data.

While quarterly productivity figures are quite volatile, a sustained slowdown represents another hurdle for the Federal Reserve’s inflation fight. With interest rates expected to stay at a two-decade high for awhile longer, business investment in equipment will likely continue to be a weak factor in overall economic growth.

Today’s data corroborates other data that showed gross domestic product cooled in the first quarter while employment costs rose by the most in a year. As a result, inflation is proving stubborn, supporting the Fed’s pivot to a more hawkish stance that will keep interest rates higher for longer than anticipated.

Of course, Fed Chair Powell told us yesterday that he “doesn’t see the stag or the flation” in US data…

{kind=link}

Maybe he needs to subscribe to ZeroHedge to see the real picture.

Tyler Durden

Thu, 05/02/2024 – 09:05

Joe Biden Says There Are Very Fine People On Both Sides Of The Oct. 7 Debate

Joe Biden Says There Are Very Fine People On Both Sides Of The Oct. 7 Debate

Authored by David Harsanyi via The Epoch Times (emphasis ours),

“I condemn the anti-Semitic protests …” President Joe Biden told reporters after days of anti-Jewish demonstrations at Columbia University and other Ivy League schools. “I also condemn those who don’t understand what’s going on with the Palestinians …”

{kind=link}

Any morally clearheaded American already has a very good idea of what’s going on. Biden is bothsidesing the actions of keffiyeh-wearing terror cheerleaders on Columbia’s Gaza Quad—who target American Jews who have absolutely no bearing on Israel’s actions—with those who refuse to accept the blood libel of “genocide” in Gaza. It is the kind of odious moral relativism one expects to hear from a “Squad” member or clout-chasing far-right “influencer,” not the president.

Hamas, the governing authority in an autonomous Gaza—still supported widely by the Palestinian people—flooded over the border on Oct. 7, 2023, raping, murdering, and kidnapping more than a thousand men, women, and children in Israel, including American citizens. Afterward, Hamas retreated and hid among civilians to generate as many Palestinian martyrs as possible. The Israelis retaliated against this nihilistic death cult, keeping the civilian-to-combatant casualty ratio lower than perhaps any other instance of modern urban warfare.

That’s what’s going on. But because a not-insignificant contingent on the contemporary left is now both anti-Semitic and anti-“colonialist,” the president demanded Israel stop before the job was done. And he is willing to sell out a longtime ally and forsake the lives of American hostages to try to entice the votes in Jew-hating enclaves like Dearborn, Michigan, Yale University, and The Washington Post newsroom.

A number of people have pointed out the similarities between Biden’s condemnations and former President Donald Trump’s post-Charlottesville, Virginia, march “very fine people” comment. It’s a good gotcha. After all, Biden has risibly claimed that Trump’s comments impelled him to run for president (for the third time).

There is, however, a key difference. Trump’s garbled line was almost surely not aimed at tiki-torch neo-Nazis. Believe what you like about Trump’s motivations, but he also later unequivocally condemned the white supremacists on more than one occasion. Biden, on the other hand, can’t even get himself to call out brownshirts without throwing them a bone.

Also, incidentally, unlike the nuts in Virginia, these people will be working at our top law firms, in media organizations and in the State Department. Oh, the president also wants you to pay their loans.

Earlier, The Washington Post, like most outlets, claimed that “Biden denounces antisemitism on college campuses amid Yale, Columbia protests.” While technically true, the framing ignores the president’s equivocation. The denouncement was a pro forma White House Passover press release that spent as much space prattling on about a two-state solution as it did the “protests.” For comparison, Biden’s Ramadan press release noted the “terrible suffering on the Palestinian people,” repeated fake Hamas causality numbers and condemned “Islamophobia,” but said nothing about the widespread outbreak of anti-Semitism.

Then again, Democrats are increasingly incapable of even talking about anti-Semitism without diluting any condemnation with mention of “Islamophobia.”

You might recall a few years back a certain Democratic congresswoman was going on about “Benjamin”-grubbing rootless cosmopolitans hypnotizing the world for their evil. After a handful of Jewish Democrats complained about her rhetoric, then-House Speaker Nancy Pelosi finally agreed to pass a resolution condemning Rep. Ilhan Omar. By the end of debate, of course, the resolution was teeming with platitudes and condemnations of a rainbow of thought crimes, with references to Alfred Dreyfus, Leo Frank, Henry Ford, and “anti-Muslim bigotry,” but not Omar.

“We all have a responsibility to speak out against anti-Semitism, Islamophobia, homophobia, transphobia, racism, and all forms of hatred and bigotry, especially as we see a spike in hate crimes in America,” is how Sen. Kamala Harris whitewashed the rising anti-Jewish pronouncements of her party. Which is to say, for years now, Democrats have been downplaying anti-Semitism as it creeped into college campuses, Congress, the Women’s March, Black Lives Matter, and now the mainstream.

And now, here we are. We have a president who can’t make a moral distinction between bigots and their targets.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Tyler Durden

Thu, 05/02/2024 – 08:45

Thursday Humor: Jobless Claims

Thursday Humor: Jobless Claims

With WARNs high, JOLTS data tumbling – led construction jobs collapsing, and Challenger-Grey layoffs remarkably elevated, why would anyone question the government’s official data on jobless claims – that continues to languish (in a good way) near record lows.

Last week saw 208,000 Americans file for jobless benefits for the first time (the same as the prior week), basically flat for the last three years…

{kind=link}

Source: Bloomberg

In the real world labor market, 2024 has been a shitshow of layoffs…

1. Everybuddy: 100% of workforce

2. Wisense: 100% of workforce

3. CodeSee: 100% of workforce

4. Twig: 100% of workforce

5. Twitch: 35% of workforce

6. Roomba: 31% of workforce

7. Bumble: 30% of workforce

8. Farfetch: 25% of workforce

9. Away: 25% of workforce

10. Hasbro: 20% of workforce

11. LA Times: 20% of workforce

12. Wint Wealth: 20% of workforce

13. Finder: 17% of workforce

14. Spotify: 17% of workforce

15. Buzzfeed: 16% of workforce

16. Levi’s: 15% of workforce

17. Xerox: 15% of workforce

18. Qualtrics: 14% of workforce

19. Wayfair: 13% of workforce

20. Duolingo: 10% of workforce

21. Rivian: 10% of workforce

22. Washington Post: 10% of workforce

23. Snap: 10% of workforce

24. eBay: 9% of workforce

25. Sony Interactive: 8% of workforce

26. Expedia: 8% of workforce

27. Business Insider: 8% of workforce

28. Instacart: 7% of workforce

29. Paypal: 7% of workforce

30. Okta: 7% of workforce

31. Charles Schwab: 6% of workforce

32. Docusign: 6% of workforce

33. Riskified: 6% of workforce

34. EA: 5% of workforce

35. Motional: 5% of workforce

36. Mozilla: 5% of workforce

37. Vacasa: 5% of workforce

38. CISCO: 5% of workforce

39. UPS: 2% of workforce

40. Nike: 2% of workforce

41. Blackrock: 3% of workforce

42. Paramount: 3% of workforce

43. Citigroup: 20,000 employees

44. ThyssenKrupp: 5,000 employees

45. Best Buy: 3,500 employees

46. Barry Callebaut: 2,500 employees

47. Outback Steakhouse: 1,000

48. Northrop Grumman: 1,000 employees

49. Pixar: 1,300 employees

50. Perrigo: 500 employees

51. Tesla: 10% of workforce

Continuing claims – according to the government – were also flat week on week at 1.774 million Americans, having gone practically nowhere for a year…

{kind=link}

Spot the odd one out… (or spot the government-supplied data)…

{kind=link}

Source: Bloomberg

Ah, Bidenomics!!

If Trump wins in November, will all this data suddenly be ‘allowed’ to reflect reality?

Tyler Durden

Thu, 05/02/2024 – 08:36