Latest News

Denver Sets Up ‘Host Migrants In Your Home’ Hotline

Denver Sets Up ‘Host Migrants In Your Home’ Hotline

Authored by Steve Watson via Modernity.news,

The Democrat run city of Denver is encouraging residents to host migrant families in their homes and has even set up a hotline so people can volunteer to take in illegals who have no where else to go.

{kind=link}

FOX31 Denver reports that a charity calling itself ‘Hope Has No Borders’ “began pairing migrant workers and their families with hosts in Colorado in late 2023. Now, with help from the United Way, getting paired up is a simple phone call away by dialing 211.”

A news segment details how one resident happily took in a family of four migrants after seeing that they are camping out in airports and on the streets because all the shelters are full.

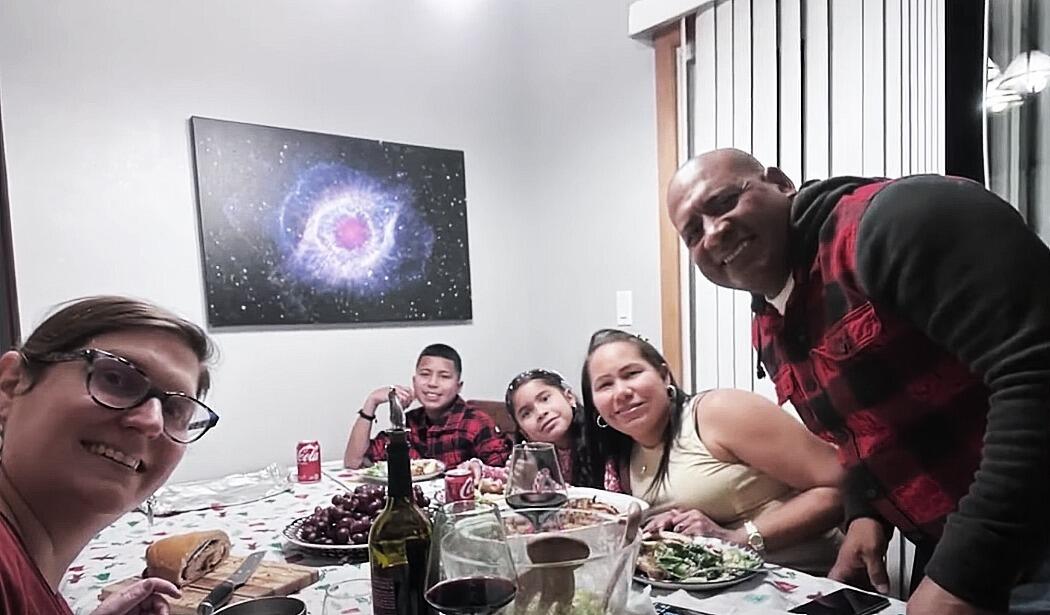

The Democrat run city of Denver is encouraging residents to host migrants in their homes and has even set up a hotline so people can volunteer to take in entire families of illegals, like this single mother with 1 spare bedroom. Full report herehttps://t.co/22rIwnI3OE pic.twitter.com/E7N4885h9A

— m o d e r n i t y (@ModernityNews) May 8, 2024

The woman, Erin Lennon, is “a single mom with a spare bedroom,” according to the report.

Not a rich liberal with an eight bedroom house then.

Imagine our shock.

The report notes that Lennon’s young son “was nervous at first about the idea of taking in strangers,” but she states “Some of the greatest things that, you know, that you do or have done, has been involved with some risk.”

As we previously highlighted, this kind of thing is happening in several cities nationwide.

Some people are treating it like it’s a way of getting a free servant:

The state of Michigan is even offering $500 per month to residents who agree to house illegal immigrants in their homes.

I’m sure the phones are ringing off the hook.

— Awitty Fellow (@JustTrollinLibs) May 7, 2024

Lots of huge houses in Cherry Creek, Boulder, and Cherry Hills. Once those are full get back to me.

— Brad Coen (@brad_coen) May 7, 2024

Whether people do or don’t invite the illegal immigrants in to their homes, they risk literal invasions via progressive squatting laws.

People in Denver dumb enough to host illegals won’t be able to get rid of them once they’re there beyond 30 days because of squatting laws.

And forget about getting the illegals prosecuted for any crimes they commit.

Eventually Denver residents will be forced to host illegals.

— Paul A. Szypula 🇺🇸 (@Bubblebathgirl) May 6, 2024

{kind=link}

{kind=link}

* * *

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Wed, 05/08/2024 – 08:55

Tesla Tumbles On Reports Of DoJ Securities Fraud Probe Over Deceptive Self-Driving Capabilities

Tesla Tumbles On Reports Of DoJ Securities Fraud Probe Over Deceptive Self-Driving Capabilities

In what appears to be just the latest ‘lawfare’ angle of attack against Elon Musk (and his freedom of speech enabling platform), President Biden’s Department of Justice is examining whether Tesla committed securities or wire fraud by misleading investors and consumers about its electric vehicles’ self-driving capabilities.

{kind=link}

Tesla’s Autopilot and Full Self-Driving systems assist with steering, braking and lane changes – but are not fully autonomous – and Reuters reports that, according to three people familiar with the matter, the DoJ is checking statements by the automaker and Chief Executive Elon Musk suggesting cars can drive themselves.

Investigators are exploring whether Tesla committed wire fraud, which involves deception in interstate communications, by misleading consumers about its driver-assistance systems, the sources said.

They are also examining whether Tesla committed securities fraud by deceiving investors, two of the sources said.

The Securities and Exchange Commission is also investigating Tesla’s representations about driver-assistance systems to investors, one of the people said. The SEC declined to comment.

TSLA shares are down around 3-4% in the pre-market on the headlines…

{kind=link}

Presumably, the Biden administration knows best exactly what level of full autonomy ‘counts’; knows best what tolerance for ‘death’ is allowed on the streets; and knows best just what the buyers of Tesla’s FSD system expected.

It appears the Biden administration also knows better than Beijing since Chinese officials told Musk that China “welcomes Tesla to do some robotaxi tests in the country” and hopes it to “set a good example”, and sources indicated that the Chinese government may have offered partial support for this FSD rollout plan.

And why go after Musk? (rhetorical question of course) – …because no other executive at any firm in history has ever exaggerated claims about product features.

Meanwhile, at the leading manufacturer of charging stations in Europe…

The headquarters of @alpitronic, the leading provider of charging stations in Europe, is in flames. pic.twitter.com/KkMgi7XPuC

— Roland Pircher (@piloly) May 8, 2024

Tyler Durden

Wed, 05/08/2024 – 08:36

US Futures Mixed As European Stocks Hit All Time High, Yields And Dollar Rise

US Futures Mixed As European Stocks Hit All Time High, Yields And Dollar Rise

US equity futures flipped between gains and losses on Wednesday while European stocks hit an all time high as May’s rally in equities continued amid a clutch of solid earnings reports. As of 7:45am, S&P 500 futures traded down 0.2%, and was near session lows reversing an earlier modest gain after the underlying gauge advanced the previous four sessions. The benchmark Treasury yield rose two basis points to 4.48%. Oil fell to the lowest level since mid-March, after a mildly bearish US stockpile report. The renewed plunge in the yen took the USDJPY as high as 155.5 amid a renewed bout of impotent jawboning by Japanese officials who however have now lost all credibility. Later today the focus will be on comments from Fed officials, including Lisa Cook, and earnings from Uber, Arm and Airbnb.

{kind=link}

Among notable premarket movers, Lyft shares rose after the ride-hailing firm’s results and outlook beat estimates. Reddit rises 13% after the social-media company reported first-quarter results that beat expectations and gave an outlook that surpassed estimates even though there is no way in hell the company can ever achieve that forecast but at least it will enjoy a higher stock price for a few months. Here are some other notable premarket movers:

Arista Networks gains 6.8% after the cloud-networking company posted a 1Q profit that beat estimates amid strong AI demand trends.

Confluent climbs 7.6% after the application software company reported first-quarter results that beat expectations.

Coupang falls 7.8% after earnings per share missed estimates, driven mostly by losses attributable to its Farfetch acquisition.

DoubleVerify plummets 42% after the digital media measurement software company cut its full-year forecast.

Dutch Bros jumps 7.8% after the drive-thru coffee chain lifted full-year projections for revenue.

Electronic Arts slips 3.8% after the video-game maker’s first-quarter bookings forecast fell shy of estimates.

Luminar rises 6% after the LiDAR sensor maker’s results broadly met expectations

Lyft gains 5% after the ride-hailing firm’s results and outlook beat estimates.

Rivian drops 6.8% after the EV-maker reported a wider-than-expected adjusted loss for the first quarter.

Shoals Technologies (SHLS) falls 16% after the solar energy equipment supplier cut its revenue guidance for the year.

Shopify shares tumble 18% after the Canadian e-commerce company reported a surprise net loss in the first quarter.

Treace Medical tumbles 59% after the medical device company cut its full-year revenue guidance.

TripAdvisor drops 16% after management determined that there is no transaction with a third party that is in the best interests of the company and its stockholders.

Twilio falls 8% after the software company’s second-quarter guidance fell short of the average analyst estimate.

Uber Technologies falls 6% as gross bookings in the first quarter missed analysts’ estimates.

Upstart declines 12% after the consumer finance company forecast revenue for the second quarter that missed analysts’ expectations.

ZoomInfo Technologies slumps 23% after the infrastructure software company’s forecasts for revenue and profit trailed Wall Street’s expectations.

Investors saying goodbye to Q1 earnings season and enjoying a 3% S&P 500 rally in May are now uncertain what comes next, as US policymakers signal bets on a pivot to easier policy may be premature. Minneapolis Fed president Neel Kashkari said it’s likely the central bank will keep rates where they are “for an extended period of time” although Neel is best known for always being wrong about everything so taking the other side my seem prudent.

“We are now crawling through the tail end of earnings season and the market is lapsing into complacency,” said Hugh Grieves, fund manager of the Premier Miton US Opportunities fund. “The economy is ‘okay,’ rate cuts remain on the table and the oil price is declining. Unfortunately that’s not a stable equilibrium.”

The Fed’s stubborn hawkish stance as a result of even more stubborn inflation has put it out of sync with central banks in Europe that have already embarked on easing. Earlier Wednesday, Sweden’s Riksbank kicked off its rate cutting cycle, easing policy for the first time in eight years. That followed the Swiss National Bank’s decision to leapfrog peers with an interest rate cut in March. Meanwhile, Fed Governor Lisa Cook is due to speak later Wednesday.

Europe’s Stoxx 600 rose 0.4%, sending European stocks rise to a record high after another batch of strong corporate earnings including sold results from Siemens Energy (for once).

{kind=link}

Elsewhere, strong earnings from AB InBev lift food and beverages, which leads gains among sectors, while auto stocks and miners lag, with BP notching a second day of losses. Here are the most notable European movers:

AB InBev shares rise as much as 5%, the most in three months, after reporting stronger organic adjusted Ebitda growth than expected in the first quarter.

Ahold Delhaize shares rise as much as 4.6% after improvement in US sales momentum and the timing of the Easter holiday drove a beat in 1Q Ebit.

Fresenius shares gain as much as 5% after the German health-care company increased its organic revenue growth guidance for the full year.

Siemens Energy shares rise as much as 14% after the company posted forecast-beating orders and boosted its guidance.

Puma shares rise as much as 6.4% after the apparel retailer delivered a 1Q Ebit beat and reaffirmed its guidance for the full year.

Alstom shares gain as much as 11% after the French train maker announced plans for a capital increase of around €1 billion.

Evonik shares climb as much as 2.2% after the chemicals company reported 1Q adjusted Ebitda that beat estimates.

Auto1 shares jump as much as 25% after the German used-car-dealer raised its gross profit forecast for the full year.

Grifols shares advance as much as 5.4% after the Spanish blood plasma firm’s board of directors adopted various resolutions to strengthen corporate governance.

Sabadell shares slip as much as 3.8% after the Spanish bank released a letter sent to its chairman on the weekend from rival BBVA, saying it had no room to improve its takeover offer.

Continental shares fall as much as 1.8% after the German tiremaker’s 1Q Ebit missed the average analyst estimates.

Securitas shares fall as much as 4.5% after the firm reported its latest earnings which analysts say were hit by weak cash performance.

Carl Zeiss Meditec shares drop as much as 6.9%, the most in about a year, after the German medical optics company reported weaker-than-expected results for the second quarter.

“Right now we’re seeing the broadening of performance, especially from the earnings perspective,” Nataliia Lipikhina, head of EMEA equity strategy at JPMorgan Private Bank, said in an interview on Bloomberg TV. “The market wanted to see that earnings in different sectors, not just tech, are delivering.”

Earlier in the session, stocks in Asia were set to halt a four-day winning streak as focus shifted to earnings to validate a recent rally. The MSCI Asia Pacific Index slipped as much as 0.9% after closing at a two-year high in the previous session. Japanese tech firms Sony and Nintendo were among the biggest drags to the gauge, with the latter dropping more than 5% on weak outlook. The country’s benchmarks fell more than 1% in the region’s worst performance. Chinese onshore benchmarks posted their first decline this week amid a warning from Morgan Stanley strategists that the recent rally is likely to abate. Hong Kong stocks also fell. Index heavyweights Tencent and Alibaba are among key tech firms to release earnings next week, and the results will be crucial for the rally to resume.

In FX, the Swedish krona is among the worst performing G-10 currencies, falling 0.4% versus the greenback after the Riksbank cut its benchmark interest rate for the first time in eight years and said it could be reduced twice more in the second half of 2024. The yen weakens 0.5% against the dollar, with USD/JPY around 155.50.

In rates, treasuries were slightly cheaper across the curve with losses led by intermediate- to long-end sectors, steepening curve spreads. US long-end yields are cheaper by 2bps, steepening 2s10s spread by 1.5bp, 5s30s by 0.5bp; the 10-year is around 4.48% with bunds lagging by 1.5bp in the sector amid new record high for Europe’s Stoxx 600 Index after another batch of strong corporate earnings. Supply concession is also a factor for Treasuries with 10-year note sale later Wednesday and 30-year bond auction Thursday. Indeed, the week’s refunding auction cycle continues at 1pm New York time with $42b 10-year new issue one day after Tuesday’s 3-year note sale drew good demand, stopping through by 0.3bp. WI 10-year yield at around 4.48% is 8bp richer than April’s, which tailed by 3.1bp in a poor result.

In commodities, oil prices decline, with WTI falling 1.6% to trade near $77.20. Spot gold drops 0.1%.

Looking at today’s calendar, the US economic data slate includes March wholesale inventories (10am). Fed members’ scheduled speeches include Jefferson (11am), Collins (11:45am) and Cook (1:30pm) From central banks, the Riksbank was the latest western bank to commence an easing cycle cutting rates to 3.75%. Finally in the US, a 10yr Treasury auction is taking place.

Market Snapshot

S&P 500 futures little changed at 5,214.75

STOXX Europe 600 up 0.3% to 515.72

MXAP down 1.0% to 176.52

MXAPJ down 0.4% to 550.52

Nikkei down 1.6% to 38,202.37

Topix down 1.4% to 2,706.43

Hang Seng Index down 0.9% to 18,313.86

Shanghai Composite down 0.6% to 3,128.48

Sensex little changed at 73,495.37

Australia S&P/ASX 200 up 0.1% to 7,804.49

Kospi up 0.4% to 2,745.05

German 10Y yield little changed at 2.44%

Euro down 0.1% to $1.0741

Brent Futures down 1.2% to $82.15/bbl

Gold spot down 0.4% to $2,305.33

US Dollar Index up 0.18% to 105.60

Top Overnight News

Chinese iPhone shipments jumped about 12% in March after Apple Inc. and its retailers slashed prices, official data showed, suggesting efforts to arrest an accelerating decline in sales are yielding early results. BBG

The BOJ may take monetary policy action if yen falls affect prices significantly, governor Kazuo Ueda said on Wednesday, offering the strongest hint to date the currency’s relentless declines could trigger another interest rate hike. Ueda also said the BOJ could raise interest rates sooner than expected if inflation overshoots its forecasts, or risks to the price outlook increases. RTRS

Germany’s industrial production for Mar was a bit better than anticipated, coming in -0.4% M/M (vs. the Street’s -0.7% forecast), although Feb was revised lower (from +2.1% to +1.7%). BBG

Sweden’s central bank lowered rates 25bp (from 4% to 3.75%) and said two additional reductions could happen in H2 (the Riksbank is only the second monetary body from an advanced economy to commence easing since the post-COVID inflation surge after Switzerland’s central bank cut in March). RTRS

Indiana primary results showed Haley performing very well, signaling a large anti-Trump faction of the GOP exists. Politico

Trump’s classified documents trial in Florida has been postponed indefinitely, raising the odds that the current Stormy Daniels/hush money one underway in NYC is the only verdict voters will receive before the election. WaPo

Corporate profits are performing very well (firms beat in Q1 and analysts have been raising estimates for Q2), suggesting an economic downturn won’t occur anytime soon. WSJ

Saudi-backed chip and AI investment firm Alat said it would divest from China if it were asked to do so by the US. The comments came after people familiar said the US revoked licenses allowing Huawei to buy chips from Intel and Qualcomm. BBG

FTX will amass as much as $16.3 billion in cash once it sells all of its assets, far more than it needs to cover what customers lost. The extra will be used to pay them interest but nothing will be left for equity holders. BBG

Earnings

BMW (BMW GY) Q1 (EUR): Revenue 36.61bln (exp. 36.82bln). EBIT 4.05bln (exp. 3.96bln). Automotive revenue 30.94bln (exp. 31.01bln). Automotive EBIT Margin 8.8% (exp. 9.05%). EBT Margin 11.4% (exp. 10.6%). BEV sales +28% Y/Y. 2024 outlook confirmed. Shares -4.5% in European trade

Siemens Energy (ENR GY) Q2 (EUR): FCF 483mln (prev. -294mln Y/Y), Profit before special items 170mln (prev. 41mln Y/Y), Net Profit 108mln (exp. -11mln). Outlook: Expects sales growth 10-12% (exp. +6%), Profit margin of -1% to +1% (prev. guided -2% to +1%). Now expects FCF pretax of up to 1bln (prev. guided negative at up to 1bln). Shares +12.5% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower after the choppy US performance and in the absence of fresh catalysts. ASX 200 lacked firm direction with gains in industrials and energy offset by weakness in miners and financials. Nikkei 225 underperformed as participants digested earnings including disappointing guidance by Nintendo. Hang Seng & Shanghai Comp were ultimately lower amid trade and tech-related frictions after the US revoked export licences that allowed Intel (INTC) and Qualcomm (QCOM) to supply Huawei with semiconductors.

Top Asian News

BoJ Governor Ueda said the BoJ will scrutinise the impact of yen moves on the economy in guiding monetary policy and FX moves could have a big impact on the economy and prices, so could warrant a monetary policy response, while he added the BoJ may need to respond via monetary policy if such impact from yen moves affect trend inflation. Ueda said they expect trend inflation to gradually head towards 2% and will adjust monetary policy as appropriate if trend inflation heads toward 2% as projected or if they see a risk of inflation overshooting their forecast. Furthermore, Ueda said they don’t see yen moves as having a big impact on trend inflation so far but there is a risk the impact could become more significant in the future and they won’t necessarily wait until inflation achieves their forecasts in 1.5 to 2 years to raise rates with the central bank to adjust the degree of monetary support accordingly if trend inflation moves as projected.

Japanese Finance Minister Suzuki said he is watching FX movements with a sense of urgency and won’t comment on forex levels, while he added it is important for currencies to move in a stable manner reflecting fundamentals. Furthermore, he said they will take a thorough response for forex and don’t believe that resources for intervention are limited.

Chinese April Prelim Retail Car Sales -2% Y/Y (vs +6% in March).

BoJ Governor Ueda says Japan’s economy is recovering moderately albeit with some weakness; will guide policy appropriately from perspective of stably and sustainably achieving the price target. Rapid/abrupt and one-sided Yen falls are negative for Japan’s economy are undesirable.

European bourses, Stoxx600 (+0.3%) are almost entirely in the green, with indices initially opening tentatively around the unchanged mark before picking up gradually to session highs throughout the morning. European sectors are mixed, with Food Beverage and Tobacco at the top of the pile, lifted by post-earning strength in AB InBev (+4.4%). Basic Resources is the clear underperformer, given the weakness in underlying metals prices; Autos are also hampered by poor BMW (-4.5%) results. US Equity Futures (ES U/C, NQ U/C, RTY -0.3%) are mixed and trading with little direction, continuing the tentative price action seen in the prior session. Apple (+0.6% pre-market) gains amid reports that its China iPhone shipments rose 12% in March.

Top European News

The BoE should leave rates unchanged at its meeting on Thursday but consider lowering them in June, according to the Times’ shadow MPC.

UK Home Office announced on Tuesday night that it was aware of a technical issue affecting E-gates across the country, while it was working closely with the Border Force and affected airports to resolve the issue. However, Heathrow Airport later stated that all Border Force systems were now running as usual and it did not expect any issues this morning when the operation starts up.

ECB’s Scicluna is to face charges of “fraud and misappropriation,” relating to his time as the Finance Minister of Malta, via Politico citing documents.

Riksbank cuts its Rate by 25bps to 3.75% (as expected by a majority of respondents); Policy rate is expected to be cut two more times during H2 if inflation outlook cuts (bringing total 2024 cuts to 3 vs prev. guided just over 2).

Barclays European Equity Strategy; raises Utilities to Market Weight from Underweight; cuts Energy to Market Weight from Overweight

FX

USD is firmer vs. all peers but to varying degrees. Support for the DXY has in large part been provided by further upside in USD/JPY. Fresh US fundamentals are lacking in what could well be a quiet week ahead of next week’s inflation metrics, though a handful of speakers and supply populate today’s docket. As such, DXY has continued to consolidate around the mid-point of the 105 handle.

EUR is softer vs. the USD but less so than peers with some support via the EUR/GBP and EUR/SEK crosses. Fresh fundamental drivers for the Eurozone are lacking and expectations of a June ECB cut remain firmly anchored. Currently trading around 1.074.

GBP is softer vs. the broadly firmer USD with UK specifics light ahead of tomorrow’s BoE which some are framing as a potential dovish hold. Cable has slipped to the 1.24 handle, going as low as 1.2468.

JPY is losing further ground to the USD with jawboning efforts from Japanese officials futile. 155.41 is the high watermark thus far with the next target a test of 156. CPI next week likely to be the next inflection point for the pair. Commentary from BoJ Governor Ueda sparked some volatility, though was ultimately unreactive to the commentary.

Antipodeans are both softer vs. the USD with AUD lagging alongside downside in metals prices. AUD/USD has extended on yesterday’s downside which has seen the pair dragged from Friday’s post-NFP peak at 0.6647 to a current low of 0.6565.

SEK is losing ground vs. peers as the Riksbank pulls the trigger on a rate reduction and leaves the door open to another two cuts in the second half of the year. Accordingly, EUR/SEK has jumped from 11.691 to a high of 11.7564 but has failed to test the YTD peak at 11.7708.

PBoC set USD/CNY mid-point at 7.1016 vs exp. 7.2202 (prev. 7.1002).

Fixed Income

USTs are a touch softer, in-fitting with the narrative outlined for Bunds above but with USTs yet to meaningfully or lastingly deviate from the unchanged mark in narrow 108-28+ to 109-03 bounds. 10yr supply and Fed speak from Cook, Collins and Jefferson scheduled.

Bunds are under modest pressure as the fixed income complex takes a very slight breather from the bullish action that has been in place since the Payrolls report on Friday. After printing an earlier 131.45 base Bunds have since stabilised around 20 ticks above this.

Gilts are essentially unchanged, and under some very modest pressure at the open which was softer by 15 ticks given bearish leads elsewhere. UK-specific developments light. Overnight, the Times Shadow MPC said the BoE on Thursday should leave rates unchanged. Currently holding around 97.95 towards Tuesday’s close and by extension at the top-end of that session’s 97.48-98.08 bounds.

UK sells GBP 2.5bln 1.50% 2053 Green Gilt: b/c 3.26x (prev. 3.05x), average yield 4.545% (prev. 4.565%), tail 0.6bps (prev. 0.3bps).

Commodities

A downbeat morning for the crude complex with newsflow rather light and Israel’s Rafah operation seemingly not likely to spark a wider conflict as things stand, though the situation remains very fluid. Brent July slipped from USD 83.05/bbl to 81.96/bbl, with some flagging the 200 DMA around USD 81.95/bbl.

Another soft session for precious metals, likely as Israel’s “limited” Rafah operation has failed to spark a regional war, with international efforts also underway to cushion the impact of the incursion. XAU trades towards the bottom of a 2,303.75-2,321.53/oz range.

Lower across the board for base metals amid a firmer Dollar and following the downbeat mood in Chinese markets overnight.

US Private Energy Inventory Data (bbls): Crude +0.5mln (exp. -1.1mln), Cushing +1.3mln, Gasoline +1.5mln (exp. -1.3mln), Distillate +1.7mln (exp. -1.1mln).

Russian Deputy PM Novak said there are no discussions about an oil output increase at OPEC+.

EU Ambassadors will today be discussing a new package of sanctions against Russia, where the focus will be on restricting LNG profits, via Politico.

Indonesia’s President said copper concentrate export permits for Freeport and Amman will be extended with the details of the extension still being calculated, according to Reuters.

Morgan Stanley has removed its USD 4/bbl risk premium from Brent forecasts, reverts forecast back to forecast of USD 90/bbl by Q3; expects OPEC to extend current production agreement at June 1st meeting, eventually to year-end, including voluntary cuts.

China Industry Ministry says the draft rules would guide Lithium battery firms to reduce manufacturing projects that “purely” expand production capacity

Geopolitics: Middle East

“IDF: We are conducting a precision operation in limited areas east of Rafah in the southern Gaza Strip”, according to Asharq News. Additionally, “IDF says it continues operations east of Rafah”, via Al Arabiya, “IDF: Hamas military infrastructure destroyed in the Rafah crossing area”.

Israeli artillery shelling was reported east of Rafah in the southern Gaza strip, according to Al Jazeera.

Hamas said Cairo talks are the ‘last chance’ for Israel to recover hostage talks, according to Al Arabiya. Furthermore, a Hamas official said the group set red lines in the ceasefire negotiations that cannot be conceded, according to Sky News Arabia.

White House thinks the Israeli operation to capture the Rafah crossing doesn’t cross President Biden’s “red line” that could lead to a shift in US policy towards the Gaza war although the US warned that if it broadens or gets out of control and Israeli forces go into the city of Rafah itself, it will be a breaking point, according to US officials cited by Axios.

CIA Director Burns plans to travel to Israel on Wednesday for talks with Israeli PM Netanyahu and Israeli officials, according to a source cited by Reuters.

Geopolitics: Other

Ukrainians hit a fuel depot in the Russian-controlled city of Luhansk, according to sources via X.

Russia launched an air attack on Kyiv, according to Ukraine’s military. It was later reported that Russia targeted energy facilities in Kyiv, Poltava, Lviv and other regions, according to Ukraine’s Energy Minister. Furthermore, Ukraine’s largest private electricity company said the Russian attack caused serious damage at three thermal power plants.

Taiwan’s leader is open to dialogue with Beijing on an equal footing, according to Taipei’s de facto envoy to the US under President-elect Lai cited by SCMP.

US Event Calendar

07:00: May MBA Mortgage Applications, prior -2.3%

10:00: March Wholesale Trade Sales MoM, est. 0.8%, prior 2.3%

10:00: March Wholesale Inventories MoM, est. -0.4%, prior -0.4%

Fed speakers

11:00: Fed’s Jefferson Speaks About Careers in Economics

11:45: Fed’s Collins Speaks to MIT Students

13:30: Fed’s Cook Speaks on Financial Stability

DB’s Jim Reid concludes the overnight wrap

As summer finally threatens to arrive here in London, even if I’m looking out on fog this morning as I type, markets continued their advance yesterday, with the risk rally continuing post what was deemed to be a very dovish payroll print last Friday. As recently as April 25th, 10yr yields peaked at 4.735% intra-day but a -28bps rally to 4.46% has come alongside a more optimistic view on rate cuts this year again. Obviously Fed Chair Powell helped this by playing down the prospect of further rate hikes at last week’s FOMC. 10yr yields have rallied around 24bps since their peak on FOMC day and yields have now fallen for a 5th consecutive session. That’s the longest run of declines since August.

Those moves on the rates side supported risk assets too, with the STOXX 600 (+1.14%) and the FTSE 100 (+1.22%) both hitting a new record yesterday as UK equities resumed trading after the holiday. The advance was more moderate in the US, but the S&P 500 (+0.13%) still posted a 4th consecutive advance despite underperformance from tech stocks. It now means the S&P has posted its strongest 4-day rally since November, having risen by +3.37% since the close last Wednesday after Powell’s press conference. Moreover, it’s worth noting that the equal-weighted S&P 500 managed to post a stronger +0.28% gain, since the Magnificent 7 (-0.50%) dragged down the rest of the index amidst larger declines from Tesla (-3.76%) and Nvidia (-1.72%). Otherwise, Disney (-9.51%) was a standout after their earnings release, and was the second-worst performer in the S&P 500 yesterday.

Asian markets are running out of a bit of steam this morning though with the Nikkei (-1.43%) the biggest underperformer across the region, slipping from multi-week highs while the CSI (-0.66%), the Shanghai Composite (-0.41%), the Hang Seng (-0.16%) and the KOSPI (-0.12%) are all lower. US stock futures are pretty much flat though with Treasury yields back up 0.5bps-1.5bps across the curve.

In FX, the J apanese yen continues to struggle trading -0.29% lower at 155.16 versus the dollar despite the B OJ Governor Kazuo Ueda stating that the central bank may take appropriate monetary action if yen moves significantly impact Japan’s inflation. Nothing particularly new in those comments but the government’s popularity is also under pressure over the weak currency and cost of travelling to, and importing from, abroad. Trade figures for April are out tomorrow.

Back to markets and one asset that continues to struggle is oil. Brent Crude was down another -0.35% to $83.04/bbl yesterday and is trading down at $82.74 this morning. We peaked above $92 in the second week of April after Middle East tensions ramped up. This reversal has been supportive for the broader market, since its helped to ease fears about more persistent inflation. For instance, US 5yr inflation swaps were down another -0.8bps yesterday to 2.49%. This is the first time since March that they’ve closed beneath 2.5%, having fallen for 7 of the past 8 sessions.

We’ll have to wait another week for the next US CPI release and the latest on inflation, but in the meantime, and as discussed at the top, sovereign bonds posted a fresh rally on both sides of the Atlantic yesterday. In the US, that saw yields on 10yr Treasuries (-3.0bps) decline to 4.46%, whilst 2yr yields were -0.2bps to 4.83%. 2yr yields had been as low as 4.80% intra-day, with a modest rise later on in part following some hawkish comments from Minneapolis Fed President Kashkari (a non-voter this year). He said in a blog post that “ with inflation in the most recent quarter moving sideways, it raises questions about how restrictive policy really is.” But Kashkari was already one of the most hawkish-sounding members on the FOMC, so the comments have to be taken in context. Year-end Fed pricing was unchanged on the day, with 44bps of cuts priced in.

Over in Europe, the focus continued to be on the ECB, with anticipation mounting that they’ll cut rates at their next meeting in 4 weeks’ time. That contributed to a fresh rally for sovereign bonds, with the 10yr bund yield (-4.9bps) falling for a 4th consecutive day to 2.42%. That was echoed across the continent, with yields on 10yr OATs (-5.2bps) and BTPs (-2.9bps) also moving lower, whilst those on 10yr gilts (-9.9bps) saw a larger decline as they caught up with the previous day’s moves.

There wasn’t much other data yesterday, although we did get the UK construction PMI for April, which hit a 14-month high of 53.0 (vs. 50.4 expected). By contrast, in Germany the construction PMI fell to 37.5, whilst the factory orders data for March contracted by -0.4% (vs. +0.4% expected). So some negative news after what have been more encouraging recent growth data for Europe’s largest economy of late. Finally, Euro Area retail sales were up +0.8% in March (vs. +0.7% expected).

To the day ahead, and data releases include German industrial production and Italian retail sales for March. From central banks, the Riksbank will be making its latest decision, and we’ll hear from Fed Vice Chair Jefferson, the Fed’s Collins and Cook, and the ECB’s Wunsch and De Cos. Finally in the US, a 10yr Treasury auction is taking place.

Tyler Durden

Wed, 05/08/2024 – 08:26

Syrian Hamsters Dead After Chinese Scientists Engineer Horrific Ebola-Enhanced Virus

Syrian Hamsters Dead After Chinese Scientists Engineer Horrific Ebola-Enhanced Virus

A group of Chinese scientists have engineered a new virus in which they took a common animal disease (vesicular stomatitis virus, or VSV) and added parts of Ebola in order to mimic Ebola symptoms in a lab setting using animals.

{kind=link}

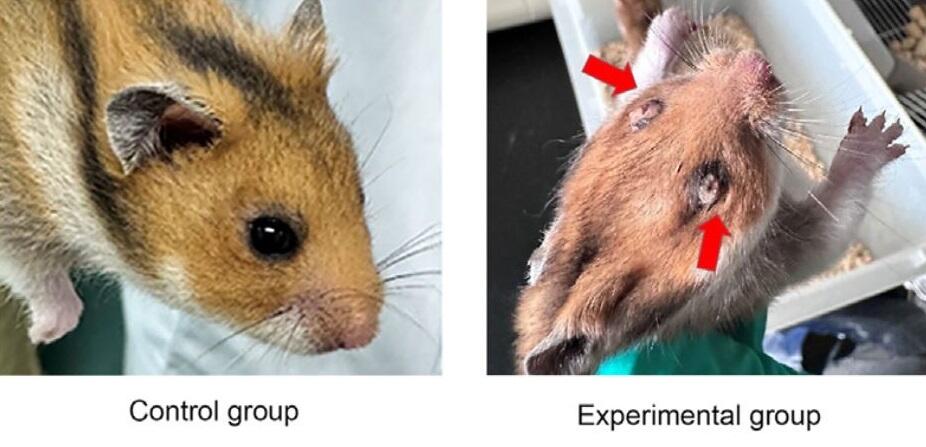

The result? A group of Syrian hamsters that received the lethal injection “developed severe systemic diseases similar to those observed in human Ebola patients, including multi-organ failure, the Daily Mail reports, citing the team’s study.

The team studied five female and five male hamsters that were three weeks old – all but two of which died between two and three days. The females – all of which died, showed decreased rectal temperature and up to 18% weight loss, the males lost 15% of their weight and died – except two, which survived and gained 20% more weight than they started with.

Some of the infected hamsters developed disgusting secretions in their eyes, which impaired vision and resulted in scabs on the surface of their eyeballs.

{kind=link}

Upon harvesting the organs from the deceased animals, they found the virus in various organs – including the heart, liver, spleen, lung, kidney, stomach, intestines and brain tissues – with the highest concentrations found in the liver, and the lowest found in the brain.

The group of female hamsters also had multi-organ failure

{kind=link}

According to the scientists, “It is a sign that 3-week-old Syrian hamsters infected with VSV-EBOV/GP have the possibility of playing a role in the study of optic nerve disorders caused by EVD.”

The team concluded that the infected hamsters showed a rapid onset of symptoms, shock liver, systemic infection, and developed severe systemic diseases similar to those observed in human EBOV patients.

They also noted that the experiments provided a rapid preclinical evaluation of medical countermeasures against Ebola under BLS-2 conditions, concluding the study was a success. -Daily Mail

Are we in danger?

{kind=link}

According to Dr. Richerd Ebright, a Rutgers University chemical biologist, it’s unlikely that a lab leak involving VSV would lead to widespread infection in the public.

“[It] will be imperative to verify that the novel chimeric virus does not infect and replicate in human cells, and does not pose risk of infectivity, transmissibility, and pathogenicity in humans, before proceeding with studies at biosafety level 2,” he said.

So, not yet.

Tyler Durden

Wed, 05/08/2024 – 07:45

A Warning For Washington From The ‘Breakdown Nations’

A Warning For Washington From The ‘Breakdown Nations’

Authored by Ruchir Sharma via FT,

{kind=link}

At a time when two big economies, the US and India, are attracting a lot of hype for their enduring strength, it is worth looking at nations that not too long ago were billed as star performers but are now breaking down. All are among the world’s 50 largest economies and, so far this decade, have suffered both a sharp decline in real per capita income growth, and a fall in their share of global gross domestic product.

Led by Canada, Chile, Germany, South Africa and Thailand, these “breakdown nations” carry a lesson. Growth is hard, sustaining it even harder, so the stars of today are not necessarily the stars of tomorrow.

Take Canada first. Widely admired for how it weathered the global financial crisis of 2008, it missed the boat when the world moved on, driven by big tech instead of commodities. Canada’s per capita GDP has been shrinking 0.4 per cent a year since 2020 — the worst rate for any developed economy in the top 50. New investment and job growth is being driven mainly by the government.

Private-sector action is confined largely to the property market, which does little for productivity and prosperity. Many young people can’t afford to buy in one of the world’s most expensive housing markets. Pressed to name a digital success, Canadians cite Shopify — but the online store is the only tech name among the country’s 10 largest companies, and its shares are trading at half their 2021 peak.

Then there’s Chile. Hailed in the 1990s as a model of deft, East-Asian style government in Latin America, its halo has since vanished. The country now makes headlines for political strife over its constitution. Anaemic tax collection has gutted public services, triggering violent street protests. Red tape has spread — the time required to get new investments approved doubled to nearly 20 months — chasing off investors.

As a result, manufacturing industries remain small compared with emerging world peers, including neighbouring Argentina. Mining products such as copper still account for most of its exports and billionaire wealth, making Chile look more like an old-fashioned commodity economy than an East Asian star.

No developed economy has seen a more dramatic turn for the worse than Germany. Its per capita income growth fell from 1.6 per cent in the past decade to less than zero in the past few years. During the pandemic Germany looked flush and flexible, poised to excel in the post-Covid world. Now it looks undone by its heavy dependence on exports to China and energy imports from Russia. Investment has contributed nothing to growth in recent years, industrial productivity is declining at a shocking annual pace of 5 per cent. Suddenly, the future of the Mittelstand — the network of manufacturers that has long been the engine of German growth — looks murky.

South Africa, meanwhile, was added to an acronym for big, fast-growing emerging markets led by Brazil, Russia, India and China back in 2010, when Bric became Brics. The largest economy in Africa, resource-rich South Africa was powered by a commodity boom that then went bust, exposing the country’s many faultlines.

The African National Congress has held power for 30 years yet presides over the same dogged set of failures: youth unemployment above 50 per cent, a shocking share of the population on welfare, weak investment, rolling power outages. While voters could oust the ANC next month, the malaise looks too deep to end soon. The IMF predicts negative per capita GDP growth over the next five years in only one top 50 economy: South Africa.

Finally, Thailand. A leader of the “Asian Tigers” before debts tripped them up in the crisis of 1998, it is now the runt of the lot, the only former Tiger to see its per capita GDP decline in this decade. It has one of the world’s highest inequality rates with 79 per cent of the poor living in rural areas. A running political battle between the rural poor and the Bangkok elite focuses public debate on how to distribute — not expand — the economic pie. Despite efforts to turn its location on global trade routes into a factory hub, productivity growth is stagnating and Thailand is losing out to manufacturing rivals like Vietnam.

The takeaway here is not that smart countries somehow turned stupid. It is that hidden traps line the path of development and can spring on nations at every income level from the middle to the rich. One basic mistake or miss, and any country can find itself stuck — until it finds the leadership and vision to chart a way out. For current stars, the message is a warning: don’t take growth for granted.

Tyler Durden

Wed, 05/08/2024 – 07:20

Apple iPhone Shipments In China Jump 12% After Discounts

Apple iPhone Shipments In China Jump 12% After Discounts

New data shows iPhone shipments in China surged in March, reversing a previous multi-month decline. This increase comes after Apple discounted handset prices throughout the first quarter, mostly in response to waning demand due to unofficial bans on the device by government agencies and competition from local brands.

Bloomberg cites official data from a new monthly report by the China Academy of Information and Communications Technology showing iPhone shipments in China bounced 12% in March.

Shipments of foreign-branded smartphones—most of which are Apple iPhones—increased to 3.75 million units in March from a year earlier. This follows a 37% decline in the first two months of the year.

{kind=link}

A report from the beginning of the year showed Apple offered an ‘ultra-rare’ iPhone discount of up to 500 yuan ($70)

At the time, Apple’s website stated, “Discounts this year encompass everything from the iPhone 13 to the iPhone 15 Pro Max.”

{kind=link}

The rare discount was made shortly after analysts from Piper Sandler and Barclays downgraded Apple due to slumping iPhone demand.

Currently, analysts tracked by Bloomberg show Apple has 35 “buys,” 18 “holds,” and 4 “sells.”

{kind=link}

The discounts early this year were the highest on record, according to analysts from Jefferies.

{kind=link}

At the time, we noted the two main drivers driving iPhone sales lower in the world’s largest handset market:

We suspect the made-in-China Mate 60 Pro, which defied Western tech sanctions and has a top-of-the-line processor, has spurred patriotic fervor among Mainland consumers for domestic handsets.

Also, companies and government agencies have told staffers to abandon Apple devices.

Last week, Apple CEO Tim Cook addressed an analyst’s question about the March quarter. He said iPhone revenue in mainland China increased “on a reported basis” before adjustments for Covid-related supply chain disruptions in 2022.

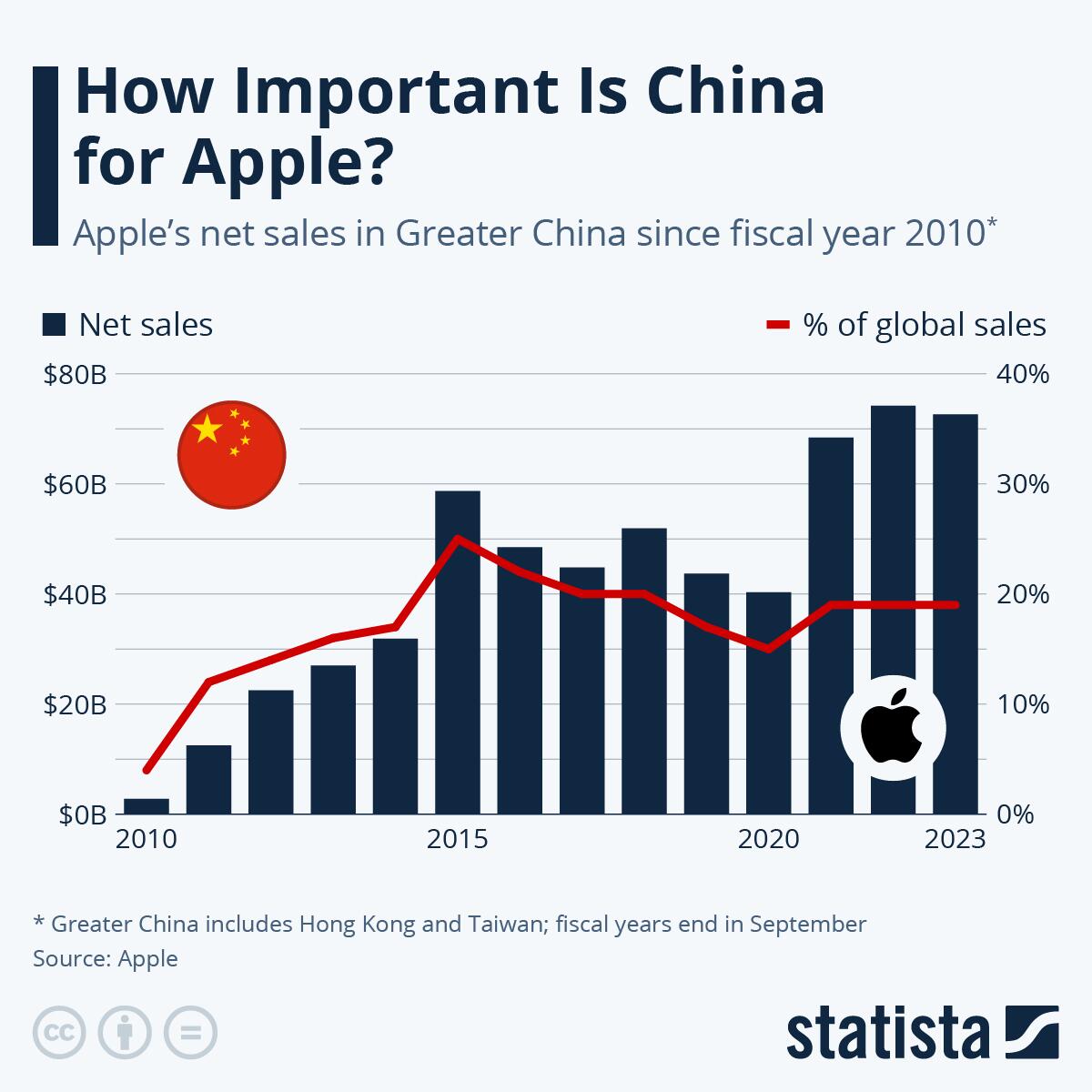

Cook did not provide further details on this metric but reiterated Apple’s commitment to the Chinese market, which, despite its contraction, still represents 18% of the company’s net sales.

According to Statista data, China is very important to Apple, accounting for nearly 20% of the company’s total sales.

{kind=link}

This is why analysts and investors closely watch iPhone demand trends in the world’s second-largest economy.

Tyler Durden

Wed, 05/08/2024 – 06:55

The Stablecoin Debate That Isn’t

The Stablecoin Debate That Isn’t

Stablecoins have been in the news lately, thanks to another round of failed legislation, a well-intentioned but poorly-designed analytics dashboard compliments of Visa, and false equivocation by a columnist at the FT.

{kind=link}

Meet the wire transfer

Nic Carter just published an epic review of the evolution of academic viewpoints on this topic, demonstrating how things are trending in the right direction. I consider Nic’s essay as a sort of realpolitik of acceptance: places where the industry is making progress because those who thought these coins could never work now concede that they can, and those who’ve been arguing they are dangerous are starting to see the benefits.

I, on the other hand, am as confident as ever that eventually all currencies will be digital and ride some kind of blockchain infrastructure, by which point we’ll just call them…money. The whole “stablecoin” moniker will be forgotten, in the same way that we no longer distinguish between electronic markets and markets. (People used to debate this distinction too).

A lot has changed since I first started making my “stablecoins will take over” argument 6 years ago. As Nic points out, even the skeptics have evolved their thinking. But most people haven’t gone far enough because most people can’t imagine the world being fundamentally different than it is today. Alas, swans required neither permission nor comprehension to be black.

Here are four reasons why a total transformation of money, payments, and banking is inevitable:

1- Tokens are a superior form factor over accounts for a digital economy. Accounts have served us well for millennia but we don’t write things down in physical ledgers anymore and the telegraph is now 200 years old. Tokens offer greater privacy, are more inclusive, can be programmed, and are more functional for machines.

TLDR: You can’t KYC a web server or an AI agent.

2- On a risk-adjusted basis, narrow banking is better for society as the primary saving and payment mechanism than fractional-reserve banking. Maturity transformation was a useful practice for primitive financial systems that didn’t have mature capital markets or other sources of wholesale funding. But it have outlived its usefulness. There are many ways to create credit in a modern economy and traditional banking is but one, the most fragile and dangerous one.

TLDR: An industry that needs to be bailed out regularly is trying to tell you something.

3- The bundling of payments and credit was always a marriage of necessity, not love. People opened checking accounts because they wanted to pay their bills, not to finance somebody else’s mortgage. But they were forced to play that role because levered banking was the only option.

If savers could pay each other with T-bills or shares in a money market fund, they would. Now they can, so they should. Those who argue the unbundling of payments from lending is somehow bad for the economy don’t understand where credit actually comes from. Banks don’t create loans, they intermediate between savers and borrowers. They will always have access to an infinite amount of deposits, at the right price.

TLDR: A financial system designed to benefit one group is unfairly harming another.

4- Money that doesn’t ride the same infrastructure as the things it is traded against is inferior. Today, our money moves via one set of pipes, and literally everything else, from securities to commodities to real estate moves in another. This is a source of risk throughout the economy. It requires large (often too big to fail) intermediaries to connect the plumbing and strong-armed regulators to watch them. Tokenization lets us put the money on the same infrastructure as every other asset and use code to guarantee outcomes.

TLDR: We no longer use copper wires to talk and radio waves to watch video, all media has converged to a single network. Value will too.

Tyler Durden

Wed, 05/08/2024 – 06:30

The Illusion Of Revolution

The Illusion Of Revolution

Submitted by QTR’s Fringe Finance

One of the topics I discussed with Matt Taibbi during my interview with him this weekend was the palpable loss of soul that has taken place on the Democratic side of the political aisle. And, as Matt Damon reminded us in Good Will Hunting whilst quoting Henry Ward Beecher:

“Liberty is the soul’s right to breathe, and when it cannot take a long breath laws are girded too tight.”

In my interview with Matt Taibbi, I told him that I used to read him when he wrote for Rolling Stone decades ago and admitted that I often wondered if the 20 year old version of me then would loathe the 40 year old version of me I’ve become.

I brought this question up because I find it important to keep myself in check. Is the world really changing and becoming so radical that it’s on the verge of breaking, or have I just grown older and become as allergic to “normal” progressive causes as the people I routinely dismissed as racist, homophobic, conspiratorial right-wing sh*theads when I was in a touring band with leopard print hair in my early 20s?

My discussion with Matt also touched on the topic of the arts. He pointed out that nowadays there really isn’t any great new music, art, poetry, or film that feels like it moves the needle in the way that classics of the last four or five decades used to.

During the course of our discussion, I remarked to Matt that I thought George Carlin was probably the last great left-wing comedian, even though he may have described himself as an independent.

And then, as if the universe heard me wondering aloud and wanted to offer up an answer, I woke up yesterday morning, and my entire Twitter feed was clips from the roast of Tom Brady.

For those unfamiliar with the format, roasts, as made famous by Comedy Central over the last decade or two, are widely accepted “safe spaces”… for comedians. This means it’s widely accepted that people are allowed to say whatever the f*ck they want and that no joke crosses the line. The roasts of the last two decades have been extraordinarily successful because of this. When comedians are unleashed to take digs at one another and there is nothing off-limits, genuine comedy and laughs happen.

The roast of Tom Brady was so popular on the internet yesterday morning because the content—including jokes about Tom Brady’s wife leaving him and the now-dead former Patriots tight end Aaron Hernandez—truly was as ‘on the edge’ as it could get.

Yet, despite the fire breathing comedians that pierced the membrane of the PC bubble repeatedly, there was nary a Karen to be found, nary a censorship report being sent to a censor, and nary a protester to be seen. For an hour or so, the soul of the nation was allowed to breathe, and people were too busy cracking the f*ck up to be offended or care, even when the crudest and meanest things were said.

It’s moments like these, Ricky Gervais hosting an award show or a Dave Chappelle “controversial” Netflix special that now serve as the reminders of what made the nation great to begin with: free speech.

During my conversation with Matt Taibbi, we examined how free speech used to be the hill that Democrats would die on. As Matt told me, it was the one issue that was non-negotiable. Matt and I both believe vehemently in free speech and I still consider myself to be liberal in the classic sense. As a self-described libertarian, the prefix lib- puts me almost all the way there already. They both come from the idea of liberty, meaning “the state of being free within society from oppressive restrictions imposed by authority on one’s way of life, behavior, or political views.”

As Matt and I continued with our Socratic analysis, desperate to figure out whose brains have been broken, us or everybody in the Democratic Party, we arrived at one key point: neither one of us could believe that censorship had become a key issue for Democrats.

And not a key issue to fight against…a key issue to fight for.

Yes, that’s right. The party that once dominated Woodstock and advocated for peace, civil rights, race relations, freedom of expression and freedom of…well, anything you wanted to do…has now become the party segregating college campuses, censoring speech and meticulously micromanaging what they perceive to be misinformation about vaccines being hurriedly forced onto the public by giant pharmaceutical companies. What happened?

As Matt and I discussed, the Democrats have somehow become the party of the know-it-all snobs, societal elites and the wealthy, whereas Republicans now seem to be the party of the working man. This wasn’t always the case, but as we said on the podcast, the entire party appears to have had some type of bizarre ideological aneurysm simply as a result of Donald Trump existing, and the magnetic poles of both parties have apparently flipped.

🔥 40% off FOR LIFE: Use this special coupon link and get 40% off an annual subscription, good for as long as you wish to remain a subscriber.

For example, while Gavin Newsom was dining out maskless at a Michelin star restaurant called French Laundry in the middle of Covid, the rest of us peons were at home, triple masked, surviving off of French dressing and doing laundry.

Decades ago, the Republicans used to be the fat cats. You know — war mongers, oil companies, the whole litany. Now the Democrats are the Martha’s Vineyard-living, limousine-riding, gated community-living insider traders.

Democrats have become the party George Carlin is railing against instead of for. They’re the big club that you’re not in.

“They own all the big media companies,” he exclaims. “They don’t want a population of citizens capable of critical thinking.”

Another glaring example of how the left has inadvertently become what they once hated are the ongoing protests on collage campuses. Unlike days of yonder, students now cloak themselves in masks to avoid being “doxxed” — oddly hilarious for a group so obsessed with embracing their own particular identities.

And while many of the students choosing to partake in these protests are doing nothing but fairly exercising their right to free speech, which I support, there have been innumerable examples of how these “activists” are devoid of understanding what they are fighting for to begin with.

Instead, it’s an exercise in entitlement and groupthink. What kind of a “revolutionary” protester demands that gluten-free bread be delivered to them?

Real revolutionaries fight the power and don’t give a f*ck about what they eat!

And if there’s nothing left to eat — f*ck it! They go on a hunger strike god damn it, and they do it happily because it’ll draw more attention to the cause they are genuinely standing for! Real revolutionaries put the cause far ahead of themselves — something the coddled narcissism of today’s left wing “activist” would never let them do. Here’s what actually having the balls to stand by your convictions looks like:

Forgive me for not being intimately familiar with the details, but I’d bet my life savings that Thích Quảng Đức (Vietnamese: man on fire in photo) never requested a gluten free bagel before self-immolating.

And look — it’s not especially surprising when you think about it. Over long periods of time, tendencies change, and preferences whipsaw back-and-forth. That’s human nature. At some point, the Democrats will once again be the party supporting actual free speech, and Republicans will be the ones that want to curb “misinformation”. It’s only a matter of time before preferences once again change.

During the days of Woodstock and the feminist movement, people on the left were the ones pushing the edge of what outlandish was to put forth big ideas like fighting inequality and discrimination. The collateral damage of them “fighting the cause”, gifted us with music like Lennon and Dylan, the poetry of Ginsburg and the comedy of Richard Pryor. Riding the edge of what is socially acceptable while making coherent, ideological arguments and observations in favor of liberty and freedom has been a surefire recipe for creating some of the most beautiful art that the world has ever seen.

As was demonstrated by the roast of Tom Brady the other night, continuing to push that envelope still breathes moments of beauty and unity into our country.

But going back to my line of questioning with Matt — sadly, I do think it is the world that has changed, and not us. For instance, I made the point to Matt that “activists” on the left nowadays have devolved into engaging in petulant “protests” like throwing soup on priceless works of art, instead of coherent and impactful action.

It’s only after thinking about why Sunday night’s roast of Tom Brady was so successful that it became crystal clear to me: the same “liberals” who used to stand for liberty and free speech and, as a result, make beautiful art — now stand for nothing coherent and resort to temper tantrums where they destroy the very same art their party’s causes once birthed.

And even though it feels like there’s nothing to look forward to, I will say this: there will be no crueler or more deserved irony than the day that today’s self-absorbed, traffic-blocking, soup-throwing activists realize they’re not revolutionaries — but rather the same authoritarian, censorship-wielding, group-thinking, malleable automatons they once thought they were fighting against.

And that sounds like the makings of a roast I’d love to attend.

QTR’s Disclaimer: I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have not been fact checked and are the opinions of their authors. They are either submitted to QTR, reprinted under a Creative Commons license or with the permission of the author. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get sh*t wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Wed, 05/08/2024 – 05:45

The Great Ukraine Robbery Is Not Over Yet: Ron Paul

The Great Ukraine Robbery Is Not Over Yet: Ron Paul

Authored by Ron Paul via the Ron Paul Institute,

{kind=link}

The ink was barely dry on President Biden’s signature transferring another $61 billion to the black hole called Ukraine, when the mainstream media broke the news that this was not the parting shot in a failed US policy. The elites have no intention of shutting down this gravy train, which transports wealth from the middle and working class to the wealthy and connected class.

Reuters wrote right after the aid bill was passed that, “Ukraine’s $61 billion lifeline is not enough.” Senate Minority Leader Mitch McConnell went on the Sunday shows after the bill was passed to say that $61 billion is “not a whole lot of money for us…” Well, that’s easy for him to say – after all it’s always easier to spend someone else’s money!

Ukraine’s foreign minister, Dmytro Kuleba, was far from grateful for the $170 billion we have shipped thus far to his country. In an interview with Foreign Policy magazine as the aid package was passed, Kuleba had the nerve to criticize the US for not producing weapons fast enough. “If you cannot produce enough interceptors to help Ukraine win the war against the country that wants to destroy the world order, then how are you going to win in the war against perhaps an enemy who is stronger than Russia?”

How’s that for a “thank you”?

It may be understandable why the Ukrainians are frustrated. Most of this money is not going to help them fight Russia. US military aid to Ukraine has left our own stockpiles of weapons depleted, so the money is going to create new production lines to replace weapons already sent to Ukraine. It’s all about the US weapons industry. President Biden admitted as much when he said, “we are helping Ukraine while at the same time investing in our own industrial base.”

This is why Washington Is desperate to make sure that if Donald Trump returns to the White House, the “Ukraine” gravy train cannot be shut down by his – or future – administrations. Last week news broke that the Ukrainian government was in negotiations with the Biden Administration to sign a ten-year security agreement that would lock in US funding for Ukraine for the next two and a half US Administrations. That would unconstitutionally tie future presidents’ hands when it comes to foreign policy and would leave Americans on the hook for untold billions more dollars taken from them and sent to the weapons industry and to a corrupt foreign government.

The US weapons industry and its cheerleaders in Washington DC are determined to keep Ukraine money flowing…until they can figure out a way to gin up a war with China after losing the current war with Russia. That, of course, depends on whether there is anything left of us when the smoke clears.

When President Biden signed the $95 billion bill to keep wars going in Ukraine and Gaza and to provoke a future war with China, he called it “a good day for world peace.” Yes, and “War is peace.” Debt is good. Freedom is slavery. We are living in a post-truth society where billions spent on pointless wars are “not a whole lot of money.” But the piper will be paid and the debt will be cleared.

Tyler Durden

Wed, 05/08/2024 – 05:00

China’s Xi In Serbia Says ‘Never Forget’ This Unprecedented US Atrocity

China’s Xi In Serbia Says ‘Never Forget’ This Unprecedented US Atrocity

Chinese leader Xi Jinping has been in France since Sunday where he met with French President Emmanuel Macron to talk about range of topics but especially the Ukraine war and trade between China and the European Union.

But on Tuesday he traveled to Serbia, and importantly the trip falls precisely on the 25th anniversary of the bombing of the Chinese Embassy in Belgrade, which came in the midst of NATO’s bombing of the Serbs of Yugoslavia during the 1999 Kosovo war.

{kind=link}

Just ahead of arriving in the Serbian capital, Xi wrote a letter which has been published by the Serbian outlet Politika. In it he lambasted NATO and by extension United States for its historic war crime..

“Twenty-five years ago today, NATO flagrantly bombed the Chinese Embassy in Yugoslavia, killing three Chinese journalists,” Xi’s words introduced.

It happened on May 7, 1999 during US-NATO 78-day bombing campaign over Yugoslavia. That’s when five US Joint Direct Attack Munition guided bombs hit scored a direct hit on the Chinese embassy in Belgrade, killing the journalists.

The US was adamant that it was inadvertent and unintentional, and eventually then President Clinton issued a formal apology to the Chinese government. It had marked the first time in all of modern history that a sovereign government’s military attacked another country’s embassy. It had not even happened once during World Wars I and II.

“This we should never forget. The Chinese people cherish peace, but we will never allow such tragic history to repeat itself,” Xi wrote.

“The Chinese-Serbian friendship, forged with the blood of our compatriots, will stay in the shared memory of the Chinese and Serbian peoples,” he continued.

His emphasis on the line “never forget” is interesting given it is a common line used by Americans when it comes to remembering the 9/11 terror attacks, as well as in the West when it comes to Holocaust remembrance days.

To review of what we’ve featured in a previous post called “America’s Benevolent Bombing of Serbia,” President Bill Clinton commenced bombing Belgrade in the name of human rights, justice, and ethnic tolerance. Approximately 1,500 Serb civilians were killed by NATO bombing in one of the biggest sham morality plays of the modern era.

As British professor Philip Hammond has noted, the 78-day bombing campaign “was not a purely military operation: NATO also destroyed what it called ‘dual-use’ targets, such as factories, city bridges, and even the main television building in downtown Belgrade, in an attempt to terrorise the country into surrender.”

{kind=link}

Clinton’s unprovoked attack on Serbia, intended to help ethnic Albanians seize control of Kosovo, set a precedent for “humanitarian” warring that was invoked by supporters of George W. Bush’s unprovoked attack on Iraq, Barack Obama’s bombing of Libya, and Donald Trump’s bombing of Syria.

Tyler Durden

Wed, 05/08/2024 – 04:15