Latest News

Druckenmiller Dropped The Biggest ‘F’ Bomb

Druckenmiller Dropped The Biggest ‘F’ Bomb

By Michael Every of Rabobank

F is for Fed; Biden; Trump; and the 1980s

In a sea of lurid, stupid headlines today, it was billionaire investor Stanley Druckenmiller who arguably dropped the biggest F bombs via a TV interview.

First: “Bidenomics, If I was a professor, I’d give him an ‘F’. Basically, they misdiagnosed Covid and thought [the economy] was going into a depression… Treasury is still acting like we’re in a depression. They’ve spent and spent and spent, and my new fear now is that spending and the resulting interest rates on the debt that’s been created are going to crowd out some of the innovation that otherwise would have taken place…. Everybody seems to get it but Yellen, who just keeps spending and spending. I think it’s dumb politically because it’s causing inflation and it doesn’t take a genius to figure out that the average American is getting hurt by the inflation.”

Investor Stanley Druckenmiller on Bidenomics: “If I were a professor, I’d give them an ‘F’.” pic.twitter.com/WfsU4ecO6y

— Squawk Box (@SquawkCNBC) May 7, 2024

As an aside, one of the reasons the White House is able to get away with this fiscal splurge is not just that ‘the US is the US’, which is true, but rather that 24/7 markets don’t have an easy spoon-fed monthly number for the US fiscal deficit as a percentage of GDP on a Bloomberg screen like CPI or GDP. What is the US fiscal deficit now and compared to cycles where unemployment was below 4%? If you know off the top of your head, I’m impressed: and you’re depressed (ZH: here is the answer).

Fiscal stimulus is off the charts: 6.5% budget deficit implies 8% unemployment (instead of 3.8%). Very soon this fiscal turbo boost will be handed over to monetary stimulus pic.twitter.com/U5TRyijf1K

— zerohedge (@zerohedge) March 24, 2024

Looking ahead to the post-2024 landscape, Druckenmiller stated:

“With Biden, I’m more worried about stagflation, with all the government spending, with all the tricks that Yellen has been using to manipulate yield curve, with the way the Fed seems to have reignited financial conditions. I think the inflationary outcome could be there. But I also fear regulation and everything else preventing productivity.”

However, he didn’t have much nice to say about Trump either and noted that inflation was likely to be even higher under his presidency, particularly if he interferes with the Fed’s independence and raises tariffs, as pledged. (Perhaps Stanley reads the work of our own Philip Marey, who has been arguing the same? It’s a small world, after all.) So that’s a pre-emptive F for Trump as well.

He therefore bewailed, “I’m basically a guy without a candidate. I’m an old-style Reagan, free markets, pro-immigration, and anti-tariff Republican.” Which would explain why he’s so unhappy. Because as I had argued before it started happening, that “The 1980s called, they want their economic policy back” recipe is being repeatedly given an F by both realpolitik and voters. That fact was just underlined by the latest US restrictions on chip sales to Huawei, TikTok’s decision to fight divest-or-close legislation in court, and any dozen other headlines from around the world.

Druckenmiller was equally acerbic about the Fed’s December pivot, where markets were suddenly led to believe that rates were going to fall rapidly again, and we were heading back to the New Normal, as if the world had not changed: as I have put it before, the Pavlov’s dogs on Wall Street started to surf a wave of their own saliva. He argued, “It seemed to me the Fed was in a perfect position. Inflation was coming down, financial conditions were tightening. To some extent, I feel like they fumbled on the five-yard line.” And this is coming from someone who is a self-proclaimed “major beneficiary” of this alleged policy error.

So, what we have now is stagflationary.

What we may have next is inflationary.

And the time-machine policy some want to see is delusionary.

Tyler Durden

Wed, 05/08/2024 – 10:45

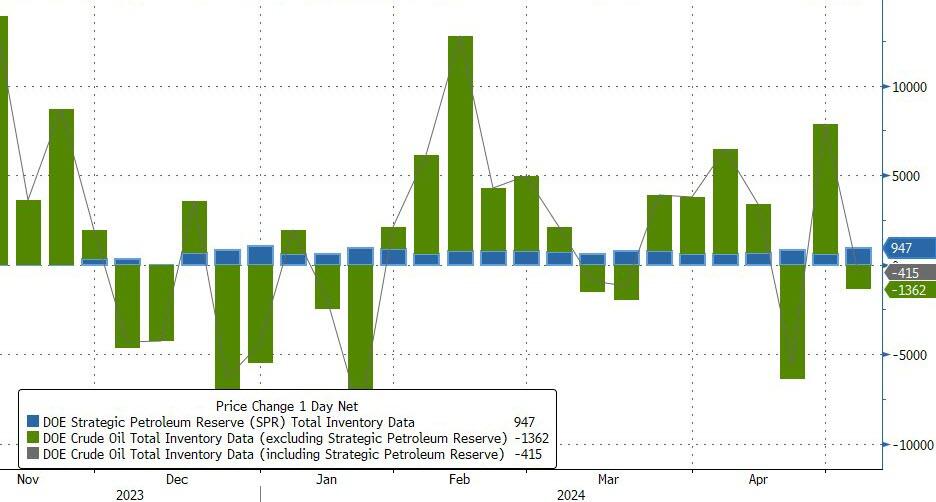

WTI Rises After Crude Draw, Biden Admin Adds Most To SPR Since Dec

WTI Rises After Crude Draw, Biden Admin Adds Most To SPR Since Dec

Oil prices are rebounding off overnight lows – once again testing the technical support of the 100-day moving average – after sliding following API’s report of across the board inventory builds last night.

Oil has been on a downtrend since early April, posting losses in three of the past four weeks, with weakness not just in timespreads but in processing margins too.

That decline has come as much of the geopolitical premium from tensions in the Middle East has unwound, bringing traders’ focus back to a cooling market.

OPEC is due to meet next month to assess supply policy after implementing production cuts over the first half of the year to support prices. Most traders expect that the curbs will be extended, possibly to the year-end

For now, the next leg will be decided by the official supply/demand data…

API

Crude +509k (-1.40mm exp)

Cushing +1.339mm

Gasoline +1.46mm

Distillates +1.713mm

DOE

Crude -1.36mm (-1.40mm exp)

Cushing +1.88mm

Gasoline +915k

Distillates +560k

After last week’s large crude build (and the API report overnight), expectations remained for a small draw… and the official data confirmed exactly that (opposing what API reported). Stocks at the Cushing Hub rose considerably and products also saw builds…

{kind=link}

Source: Bloomberg

The Biden admin added 947k barrels to the SPR – the most since Dec 2023

{kind=link}

Source: Bloomberg

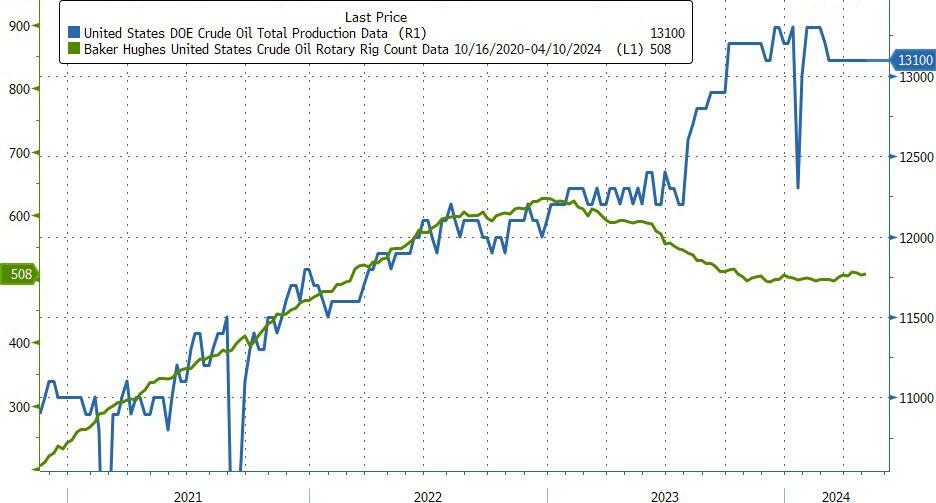

US Crude production was flat near record highs at 13.1mm b/d…

{kind=link}

Source: Bloomberg

WTI was trading around $78 ahead of the official data, just below its 100DMA…

{kind=link}

…and WTI extended gains after the ‘surprise’ draw…

{kind=link}

Overall, “oil is lower because a renewed battle between Israel and Hamas, in isolation, does not really affect oil-producing nations,” Stewart Glickman, energy equity analyst at CFRA Research, told MarketWatch.

If Iran is “subsequently encouraged to do more direct attacks on Israel, it may be different,” he said, but the market is “discounting this possibility.”

Finally, President Biden will use crude oil from the strategic petroleum reserve should the need arise, energy adviser Amos Hochstein has said, noting there was enough oil in the reserve.

“We have been replenishing into the SPR for the last several months. I think we have sufficient supply in the SPR to address any kind of concern in the economy if we need it,” Hochstein said, speaking at the Milken Institute Global Conference, as quoted by Reuters.

Tyler Durden

Wed, 05/08/2024 – 10:37

Another Trump Trial Derailed: Fani-Donating Judge’s Decision To Keep Her On RICO Trial Under Scrutiny By Appeals Court

Another Trump Trial Derailed: Fani-Donating Judge’s Decision To Keep Her On RICO Trial Under Scrutiny By Appeals Court

One day after former President Donald Trump’s classified documents trial was postponed indefinitely after we learned that the DOJ mishandled evidence in the case (with Judge Aileen M. Cannon citing a mountain of ‘outstanding’ pre-trial matters that would make a May 20 trial ‘imprudent’), another Trump case appears to have no chance of going to trial before the 2024 election.

{kind=link}

On Wednesday, a Georgia appeals court agreed to review a lower court ruling which allowed Fulton County District Attorney Fani Willis to remain on the Trump RICO prosecution despite being highly conflicted.

To review, Atlanta Judge Scott McAfee of Fulton Superior Court, who donated to Fani Willis when she was running for office, ruled in March that the Fani simply had to kick her lover, Nathan Wade, off the case after she paid him more than $600,000. The two notoriously took several lavish vacations together on Wade’s dime (which Fani swears she repaid in cash).

According to McAfee, while he found the “appearance of impropriety,” no “disqualification of a constitutional officer necessary when a less drastic and sufficiently remedial option is available,” adding “that the prosecution of this case cannot proceed until the State selects one of two options.”

And now, the Atlanta Court of Appeals has agreed to hear an appeal from the defendants over whether McAfee erred in his decision.

The Georgia Court of Appeals has agreed to hear an appeal from defendants over whether the judge erred when he ruled that Fani Willis could remain on the Trump RICO prosecution in Fulton County. This pushes that trial further off, likely beyond the election. pic.twitter.com/F1gXIfwI5E

— Joyce Alene (@JoyceWhiteVance) May 8, 2024

Willis indicted Trump and 18 other defendants last August, accusing them of a wide-ranging scheme to attempt to overturn the results of the 2020 presidential election in the state. All of the defendants were charged under Georgia’s Racketeer Influenced and Corrupt Organizations, or RICO, law. Trump and most of the other defendants have pleaded not guilty.

In their appeal application, Trump and other defendants argued that McAfee was wrong not to remove both WIllis and Wade, writing that “providing DA Willis with the option to simply remove Wade confounds logic and is contrary to Georgia law.“

Most recently, Willis has defiantly refused to appear before a Georgia Senate Investigative Committee, telling reporters earlier this week (via RedState):

REPORTER: Would you appear before a Georgia Senate committee without a subpoena?

WILLIS: Well first of all I don’t even think they have the authority to subpoena me, but they didn’t learn the law.

REPORTER: Will you appear, yes or no?

WILLIS: I will not appear to anything that is unlawful. I have not broken the law in any way. I’ve said it, you know, I’ll say it amongst these leaders—I’m sorry folks get p***ed off that everybody gets treated even.

FAITH LEADER STANDING NEXT TO HER: I think she answered that very well.

The Georgia Court of Appeals has agreed to hear an appeal from defendants over whether the judge erred when he ruled that Fani Willis could remain on the Trump RICO prosecution in Fulton County. This pushes that trial further off, likely beyond the election. pic.twitter.com/F1gXIfwI5E

— Joyce Alene (@JoyceWhiteVance) May 8, 2024

Another one bites the dust?

Every Trump trial is melting down in front of the weaponized DOJ’s eyes. https://t.co/FjikKJDrPF

— zerohedge (@zerohedge) May 7, 2024

Tyler Durden

Wed, 05/08/2024 – 10:14

Forward Guidance: The Fed Sounds Like A Wizard Reading Chicken Bones

Forward Guidance: The Fed Sounds Like A Wizard Reading Chicken Bones

Authored by Mike Shedlock via MishTalk.com,

Stanley Druckenmiller says the Fed should get rid of forward guidance and just do their job.

{kind=link}

I totally endorse a view by Stan Druckenmiller, the Fed Should Stop Forward Guidance.

Partial Video Transcript

Squawk Box:

I’ve been perplexed about the unwavering focus the Fed has had on cuts for a six month period. … Did cuts make sense the whole time?

Druckenmiller:

I was perplexed with the December pivot. …

To some extent it seems they fumbled on the 5-yard line with the game on the line. I remember saying to some of my partners, that’s the speech I thought we might hear in March.

… Instead they set financial conditions on fire. …

And once financial conditions took off, it became very clear this thing could go either way. More curiously, why they and others continued to talk about, well, it’s not going to be six cuts it’s only going to be three cuts or four cuts.

I’m going, why are we even talking about cuts?

Because inflation, if you remember, we did trillions of dollars of QE because it was 1.7 percent instead of 2! But somehow now that we are at 3 vs 2 we’ve got to start cutting rates to bring in a smooth landing. Huge mistake. It goes back to Kevin Warsh, when he was in the running for the Fed job, used to talk about reforming the Fed.

And I go Kevin, what is the major reform that we do? He says we’ve got to get rid of forward guidance.

When you put forward guidance out, unlike me when I am wrong, I tend to change my mind very rapidly, they get trapped in the forward guidance, stuck in it. … Bizarrely, at the last press conference, the Fed seems to still be hanging on to this asymmetric directive of we are not going to hike and we expect to cut but we are going to wait for the data.

… I don’t know where inflation is going to be in a year, Powell doesn’t know. I don’t think anybody knows.

Squawk Box:

You think a hike is off the table? Definitely?

Druckenmiller:

No, because there’s not a zero percent chance inflation has bottomed. I don’t know. What I would do is just say nothing, and do what a Fed chair used to do: When you need to raise rates, raise them; when you need to cut rates, cut them.

Don’t go on 60 Minutes.

You are not a rock star. You’re the Fed chair.

You are supposed to be running monetary policy.

Bernanke did a lot of things I don’t feel good about. One of the worst was forward guidance.

You have a bunch of academics talking about sending a message to the markets.

I would rather they get rid of forward guidance and just do their job.

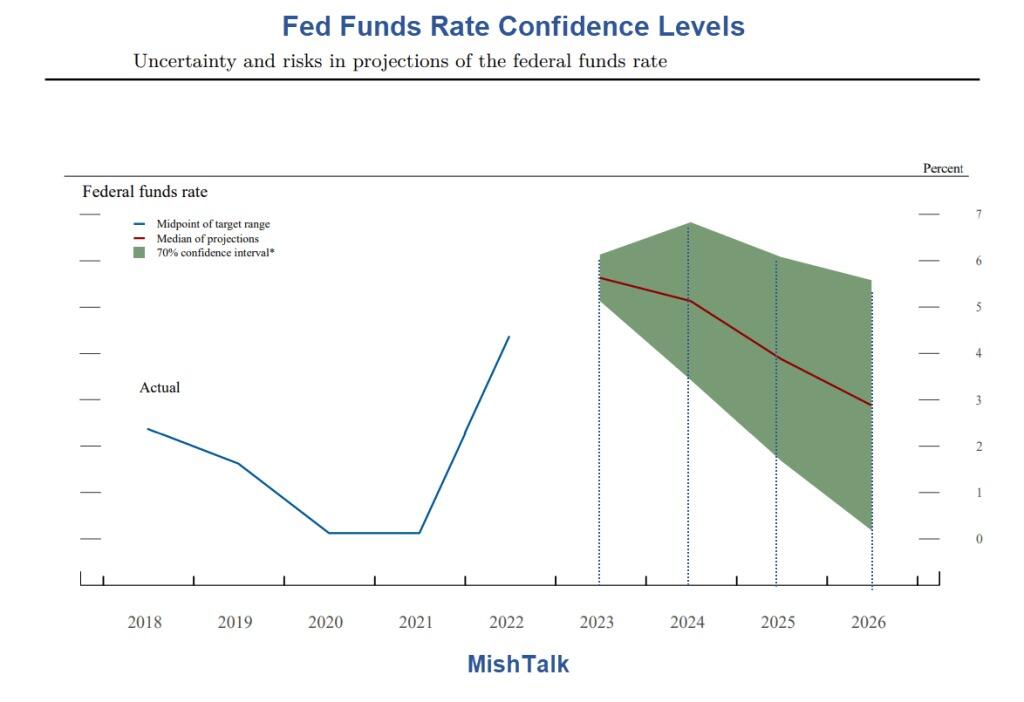

The Fed is Uncertain About Uncertainty, So Why the Forward Guidance?

On September 22, 2023, shortly before the Fed’s pivot, I asked The Fed is Uncertain About Uncertainty, So Why the Forward Guidance?

The key words at the FOMC press conference is “uncertain” for good reason. The Fed doesn’t know what it’s doing.

Here is the image I posted then.

{kind=link}

Image from the Fed FOMC projection materials.

Hoot of the Day

Actually, it’s good that the Fed is uncertain because their expectations have not been close to the mark for a decade.

The above chart is particularly amusing. The Fed has only a 70 percent confidence level that interest rates three years from now will be in the range of of 0 to 5.5 percent.

That means the Fed expects that 30 percent of the time, rates will be outside that range.

From 2012 to 2019 the Fed kept producing interest rate charts showing hikes that never happened.

Then the Fed decided it was necessary to make up for lack of inflation.

Need to Make Up For Lack of Inflation

Seeing a lot of inflation-related tweets…

Don’t forget to thank the folks at the @federalreserve who’ve been trying for years to spike your cost of living. pic.twitter.com/W67bBgr8Wq

— Rudy Havenstein, Senior Markets Commentator. (@RudyHavenstein) July 24, 2021

I’ve been discussing this for going on two decades.

Fed Uncertainty Principle

Flashback April 3, 2008 before the collapse of Lehman and Bear Stearns, to one of my all time favorite posts: Fed Uncertainty Principle

Most think the Fed follows market expectations.

However, this creates what would appear at first glance to be a major paradox: If the Fed is simply following market expectations, can the Fed be to blame for the consequences? More pointedly, why isn’t the market to blame if the Fed is simply following market expectations?

This is a very interesting theoretical question. While it’s true the Fed typically only does what is expected, those expectations become distorted over time by observations of Fed actions.

For example: If market participants are expecting the Fed to cut on weakness and the Fed does, market participants get into a psychology of expecting more cuts on more weakness. Here is another example: If market participants expect the Fed to cut rates when economic stress occurs, they will take positions based on those expectations. These expectation cycles can be self-reinforcing.

The Observer Affects The Observed

The Fed, in conjunction with all the players watching the Fed, distorts the economic picture. I liken this to Heisenberg’s Uncertainty Principle where observation of a subatomic particle changes the ability to measure it accurately.

The Fed, by its very existence, alters the economic horizon. Compounding the problem are all the eyes on the Fed attempting to game the system.

Fed Uncertainty Principle Recap

Fed Uncertainty Basis Principle:

The fed, by its very existence, has completely distorted the market via self-reinforcing observer/participant feedback loops. Thus, it is fatally flawed logic to suggest the Fed is simply following the market, therefore the market is to blame for the Fed’s actions. There would not be a Fed in a free market, and by implication, there would not be observer/participant feedback loops either.

Corollary Number One:

The Fed has no idea where interest rates should be. Only a free market does. The Fed will be disingenuous about what it knows (nothing of use) and doesn’t know (much more than it wants to admit), particularly in times of economic stress.

Corollary Number Two: The government/quasi-government body most responsible for creating this mess (the Fed), will attempt a big power grab, purportedly to fix whatever problems it creates. The bigger the mess it creates, the more power it will attempt to grab. Over time this leads to dangerously concentrated power into the hands of those who have already proven they do not know what they are doing.

Corollary Number Three:

Don’t expect the Fed to learn from past mistakes. Instead, expect the Fed to repeat them with bigger and bigger doses of exactly what created the initial problem.

Corollary Number Four:

The Fed simply does not care whether its actions are illegal or not. The Fed is operating under the principle that it’s easier to get forgiveness than permission. And forgiveness is just another means to the desired power grab it is seeking.

And so here we are. Still discussing the same things, with the Fed making the same mistakes.

The Fed’s Big Problem

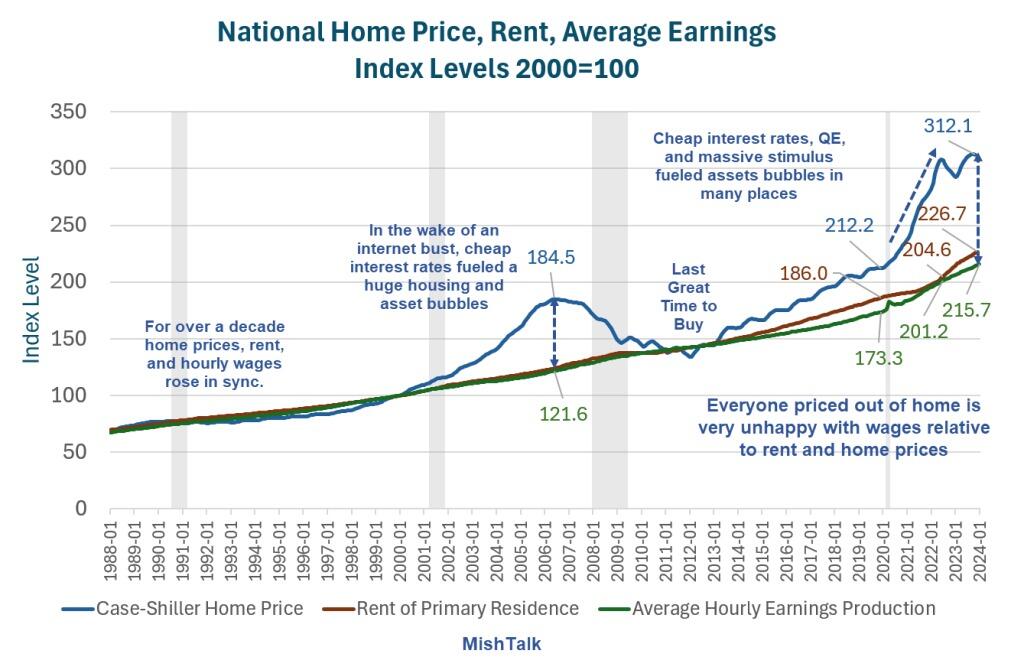

On average, the economy looks OK. But averages are misleading. Several large groups of people are struggling. They all have one thing in common.

Case-Shiller home price index, CPI rent index, and the index of hourly earnings for production and nonsupervisory workers.

{kind=link}

The Fed is now trapped in a box of its own making. Everyone who is priced out of a home is very unhappy with soaring rent, soaring home prices.

If the Fed cuts rates prematurely, what does that do to housing prices?

For discussion, please see The Fed’s Big Problem, There Are Two Economies But Only One Interest Rate

Meanwhile, Powell sounds like a wizard reading chicken bones because that’s really all he is.

Tyler Durden

Wed, 05/08/2024 – 10:10

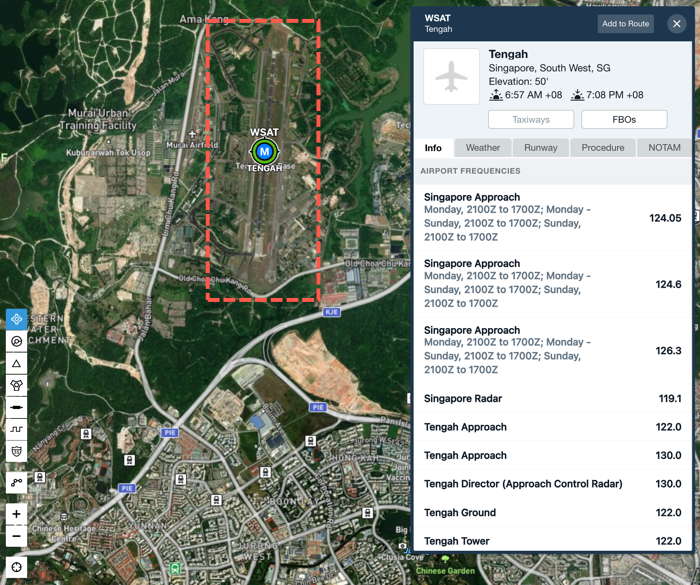

Singapore Air Force Says F-16 Fighter Jet Crashed At Air Base

Singapore Air Force Says F-16 Fighter Jet Crashed At Air Base

A Republic of Singapore Air Force (RSAF) General Dynamics F-16 Fighting Falcon jet crashed on Wednesday after experiencing an “issue” during take-off.

The Ministry of Defence said, “The pilot successfully ejected and the plane crashed thereafter within Tengah Air Base. The pilot is conscious and able to walk. He is receiving medical attention and no other personnel are hurt.”

{kind=link}

Here’s ForeFlight data on Tengah Air Base.

{kind=link}

“Full investigations are underway to make sure all factors are identified and rectified decisively,” Minister for Defense Ng Eng Hen said in a Facebook post.

The RSAF did not elaborate on what caused the downing of the US-made fighter jet, which was the RSAF’s first incident with the fighter in two decades.

Stateside, on Monday, a Lockheed Martin F-22 stealth fighter experienced a “mishap” during landing at Savannah/Hilton Head International Airport.

Simultaneously, in a significant development for the ongoing war in Eastern Europe, Belgium, Denmark, Norway, and the Netherlands have committed to providing F-16s to Ukraine. In response, Russia issued a warning on Monday, stating that the deployment of F-16s in Ukraine would be viewed as an escalation.

Tyler Durden

Wed, 05/08/2024 – 09:50

Brazen Election Interference: Illinois Democrats Retroactively Change Law To Knock Out Republican Challengers

Brazen Election Interference: Illinois Democrats Retroactively Change Law To Knock Out Republican Challengers

By Mark Glennon of Wirepoints

As an alternative to a primary election, Illinois law allowed for a party to get its candidates on the ballot for General Assembly spots by party slating procedure, along with collection of a requisite number of public signatures on nominating positions. A number of Republican challengers have been proceeding accordingly.

But over the course of just 30 hours on the first days of this month, the Democratic supermajority changed the law to retroactively disallow that procedure, thereby barring challengers from the November ballot as Republican party candidates.

The new law almost certainly gives Democrats a win in races in which Republicans did not run a candidate in the primary and could result in dozens of unopposed races.

Gov. JB signed the new law the day after it was passed, hours after telling reporters he didn’t know all the details. He also claimed it was an “ethics” bill.

“It really does make sure that we don’t have backroom deals to put people on the ballot and run as a result of some small group of people in a smoke-filled room making the choice,” Pritzker said at an unrelated news conference in Bloomington.

“So I think to me, more transparency is better.” It’s not like Illinois Democrats ever line up their chosen candidates to run for the party, right?

“This is nothing more than a brazen attempt by Illinois Democrats to disenfranchise voters and eliminate political competition. To hide behind the guise of ‘ethics,’ is laughable,” said Sean M. Morrison, Chairman of the Cook County GOP.

The new law originated as a “shell bill” – one on an entirely different subject with a different label, before being changed in the 30-hour cram-through.

Senate Minority Leader John Curran (R-Downers Grove) said it right:

“This abuse of power that blocks candidates from giving voters a choice in free, fair and open elections is unprecedented in Illinois’ 205-year history,” Curran said. “Their dictator-style tactic of stealing an election before a vote is cast is a new low for elective government in this state and undermines the core principals of American democracy.”

Democrats are widely believed to be particularly motivated by trying to assist Rep. Katie Stuart (D-Edwardsville), who is running for reelection in an increasingly Republican district. However, we are told that at least 20 Republicans may be knocked out of ballot spots.

This is all brought to you by the crowd who tells us that democracy is at risk in November’s election, headed, in Illinois by President Biden’s proxy (as he is routinely called, even by his allies), Pritzker.

At least one Democrat couldn’t ignore the hypocrisy. “At this time in our history, when we are watching Republican legislatures across the country really attack access to the ballot and attack voting rights and fundamentally attack democracy, I just think it’s fundamentally wrong for Democrats to participate in something that makes it harder for people to run, to run for office, makes it harder for folks to engage,” Rep. Kelly Cassidy (D-Chicago) said.

Grounds for lawsuits are now being considered, we are told by knowledgeable sources. I am no expert on election law and I don’t know what they are considering, but I have to believe that federal claims based on well-established application of civil rights laws to election rigging are in order.

It doesn’t get more shameless, tyrannical and hypocritical than this.

Tyler Durden

Wed, 05/08/2024 – 09:30

Intel Shares Fall After Cutting Q2 Revenue Estimates Over Pulled China Licenses

Intel Shares Fall After Cutting Q2 Revenue Estimates Over Pulled China Licenses

Intel provided an update on its second-quarter revenue forecast following the Biden administration’s decision to revoke its export license to supply semiconductors to Huawei. The new estimates reveal revenues will be below the midpoint of the $12.5 billion to $13.5 billion range.

Blame game…

A new trend? Blame earnings weakness on Biden policies: here’s Intel pic.twitter.com/UjIdBcishc

— zerohedge (@zerohedge) May 8, 2024

In an SEC filing on Wednesday, Intel revealed that the US Department of Commerce’s revoking of its license for exports to specific Chinese customers will pressure second-quarter earnings. The company now expects revenue for the quarter to “remain in the original range of $12.5 billion to $13.5 billion but below the midpoint.”

Intel added, “For full year 2024, the Company continues to expect revenue and earnings per share to grow year-over-year compared to 2023.”

This comes after an overnight report from the Financial Times that said the Biden administration “revoked export licences that allow Intel and Qualcomm to supply Huawei with semiconductors as Washington increases the pressure on the Chinese telecoms equipment company.”

People familiar with the situation said the Department of Commerce’s latest move was to pressure the supply of chips for Huawei’s smartphones.

“We continuously assess how our controls can best protect our national security and foreign policy interests, taking into consideration a constantly changing threat environment and technological landscape,” said a spokesperson for the department. The agency confirmed to FT that it had “revoked certain licenses for exports to Huawei” but did not reveal which US companies were involved.

The spokesperson added, “As part of this process, as we have done in the past, we sometimes revoke export licences.”

Intel shares fell 2% in premarket trading in New York. Shares are nearing Covid lows.

{kind=link}

Intel shares are down 40% this year, while the Philadelphia Semiconductor Index is up around 15%.

{kind=link}

Didn’t Biden give Intel $8.5 billion via the CHIPs Act?

{kind=link}

Maybe Chips Act 2.0 is needed to save Intel.

Tyler Durden

Wed, 05/08/2024 – 09:10

Denver Sets Up ‘Host Migrants In Your Home’ Hotline

Denver Sets Up ‘Host Migrants In Your Home’ Hotline

Authored by Steve Watson via Modernity.news,

The Democrat run city of Denver is encouraging residents to host migrant families in their homes and has even set up a hotline so people can volunteer to take in illegals who have no where else to go.

{kind=link}

FOX31 Denver reports that a charity calling itself ‘Hope Has No Borders’ “began pairing migrant workers and their families with hosts in Colorado in late 2023. Now, with help from the United Way, getting paired up is a simple phone call away by dialing 211.”

A news segment details how one resident happily took in a family of four migrants after seeing that they are camping out in airports and on the streets because all the shelters are full.

The Democrat run city of Denver is encouraging residents to host migrants in their homes and has even set up a hotline so people can volunteer to take in entire families of illegals, like this single mother with 1 spare bedroom. Full report herehttps://t.co/22rIwnI3OE pic.twitter.com/E7N4885h9A

— m o d e r n i t y (@ModernityNews) May 8, 2024

The woman, Erin Lennon, is “a single mom with a spare bedroom,” according to the report.

Not a rich liberal with an eight bedroom house then.

Imagine our shock.

The report notes that Lennon’s young son “was nervous at first about the idea of taking in strangers,” but she states “Some of the greatest things that, you know, that you do or have done, has been involved with some risk.”

As we previously highlighted, this kind of thing is happening in several cities nationwide.

Some people are treating it like it’s a way of getting a free servant:

The state of Michigan is even offering $500 per month to residents who agree to house illegal immigrants in their homes.

I’m sure the phones are ringing off the hook.

— Awitty Fellow (@JustTrollinLibs) May 7, 2024

Lots of huge houses in Cherry Creek, Boulder, and Cherry Hills. Once those are full get back to me.

— Brad Coen (@brad_coen) May 7, 2024

Whether people do or don’t invite the illegal immigrants in to their homes, they risk literal invasions via progressive squatting laws.

People in Denver dumb enough to host illegals won’t be able to get rid of them once they’re there beyond 30 days because of squatting laws.

And forget about getting the illegals prosecuted for any crimes they commit.

Eventually Denver residents will be forced to host illegals.

— Paul A. Szypula 🇺🇸 (@Bubblebathgirl) May 6, 2024

{kind=link}

{kind=link}

* * *

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden

Wed, 05/08/2024 – 08:55

Tesla Tumbles On Reports Of DoJ Securities Fraud Probe Over Deceptive Self-Driving Capabilities

Tesla Tumbles On Reports Of DoJ Securities Fraud Probe Over Deceptive Self-Driving Capabilities

In what appears to be just the latest ‘lawfare’ angle of attack against Elon Musk (and his freedom of speech enabling platform), President Biden’s Department of Justice is examining whether Tesla committed securities or wire fraud by misleading investors and consumers about its electric vehicles’ self-driving capabilities.

{kind=link}

Tesla’s Autopilot and Full Self-Driving systems assist with steering, braking and lane changes – but are not fully autonomous – and Reuters reports that, according to three people familiar with the matter, the DoJ is checking statements by the automaker and Chief Executive Elon Musk suggesting cars can drive themselves.

Investigators are exploring whether Tesla committed wire fraud, which involves deception in interstate communications, by misleading consumers about its driver-assistance systems, the sources said.

They are also examining whether Tesla committed securities fraud by deceiving investors, two of the sources said.

The Securities and Exchange Commission is also investigating Tesla’s representations about driver-assistance systems to investors, one of the people said. The SEC declined to comment.

TSLA shares are down around 3-4% in the pre-market on the headlines…

{kind=link}

Presumably, the Biden administration knows best exactly what level of full autonomy ‘counts’; knows best what tolerance for ‘death’ is allowed on the streets; and knows best just what the buyers of Tesla’s FSD system expected.

It appears the Biden administration also knows better than Beijing since Chinese officials told Musk that China “welcomes Tesla to do some robotaxi tests in the country” and hopes it to “set a good example”, and sources indicated that the Chinese government may have offered partial support for this FSD rollout plan.

And why go after Musk? (rhetorical question of course) – …because no other executive at any firm in history has ever exaggerated claims about product features.

Meanwhile, at the leading manufacturer of charging stations in Europe…

The headquarters of @alpitronic, the leading provider of charging stations in Europe, is in flames. pic.twitter.com/KkMgi7XPuC

— Roland Pircher (@piloly) May 8, 2024

Tyler Durden

Wed, 05/08/2024 – 08:36

US Futures Mixed As European Stocks Hit All Time High, Yields And Dollar Rise

US Futures Mixed As European Stocks Hit All Time High, Yields And Dollar Rise

US equity futures flipped between gains and losses on Wednesday while European stocks hit an all time high as May’s rally in equities continued amid a clutch of solid earnings reports. As of 7:45am, S&P 500 futures traded down 0.2%, and was near session lows reversing an earlier modest gain after the underlying gauge advanced the previous four sessions. The benchmark Treasury yield rose two basis points to 4.48%. Oil fell to the lowest level since mid-March, after a mildly bearish US stockpile report. The renewed plunge in the yen took the USDJPY as high as 155.5 amid a renewed bout of impotent jawboning by Japanese officials who however have now lost all credibility. Later today the focus will be on comments from Fed officials, including Lisa Cook, and earnings from Uber, Arm and Airbnb.

{kind=link}

Among notable premarket movers, Lyft shares rose after the ride-hailing firm’s results and outlook beat estimates. Reddit rises 13% after the social-media company reported first-quarter results that beat expectations and gave an outlook that surpassed estimates even though there is no way in hell the company can ever achieve that forecast but at least it will enjoy a higher stock price for a few months. Here are some other notable premarket movers:

Arista Networks gains 6.8% after the cloud-networking company posted a 1Q profit that beat estimates amid strong AI demand trends.

Confluent climbs 7.6% after the application software company reported first-quarter results that beat expectations.

Coupang falls 7.8% after earnings per share missed estimates, driven mostly by losses attributable to its Farfetch acquisition.

DoubleVerify plummets 42% after the digital media measurement software company cut its full-year forecast.

Dutch Bros jumps 7.8% after the drive-thru coffee chain lifted full-year projections for revenue.

Electronic Arts slips 3.8% after the video-game maker’s first-quarter bookings forecast fell shy of estimates.

Luminar rises 6% after the LiDAR sensor maker’s results broadly met expectations

Lyft gains 5% after the ride-hailing firm’s results and outlook beat estimates.

Rivian drops 6.8% after the EV-maker reported a wider-than-expected adjusted loss for the first quarter.

Shoals Technologies (SHLS) falls 16% after the solar energy equipment supplier cut its revenue guidance for the year.

Shopify shares tumble 18% after the Canadian e-commerce company reported a surprise net loss in the first quarter.

Treace Medical tumbles 59% after the medical device company cut its full-year revenue guidance.

TripAdvisor drops 16% after management determined that there is no transaction with a third party that is in the best interests of the company and its stockholders.

Twilio falls 8% after the software company’s second-quarter guidance fell short of the average analyst estimate.

Uber Technologies falls 6% as gross bookings in the first quarter missed analysts’ estimates.

Upstart declines 12% after the consumer finance company forecast revenue for the second quarter that missed analysts’ expectations.

ZoomInfo Technologies slumps 23% after the infrastructure software company’s forecasts for revenue and profit trailed Wall Street’s expectations.

Investors saying goodbye to Q1 earnings season and enjoying a 3% S&P 500 rally in May are now uncertain what comes next, as US policymakers signal bets on a pivot to easier policy may be premature. Minneapolis Fed president Neel Kashkari said it’s likely the central bank will keep rates where they are “for an extended period of time” although Neel is best known for always being wrong about everything so taking the other side my seem prudent.

“We are now crawling through the tail end of earnings season and the market is lapsing into complacency,” said Hugh Grieves, fund manager of the Premier Miton US Opportunities fund. “The economy is ‘okay,’ rate cuts remain on the table and the oil price is declining. Unfortunately that’s not a stable equilibrium.”

The Fed’s stubborn hawkish stance as a result of even more stubborn inflation has put it out of sync with central banks in Europe that have already embarked on easing. Earlier Wednesday, Sweden’s Riksbank kicked off its rate cutting cycle, easing policy for the first time in eight years. That followed the Swiss National Bank’s decision to leapfrog peers with an interest rate cut in March. Meanwhile, Fed Governor Lisa Cook is due to speak later Wednesday.

Europe’s Stoxx 600 rose 0.4%, sending European stocks rise to a record high after another batch of strong corporate earnings including sold results from Siemens Energy (for once).

{kind=link}

Elsewhere, strong earnings from AB InBev lift food and beverages, which leads gains among sectors, while auto stocks and miners lag, with BP notching a second day of losses. Here are the most notable European movers:

AB InBev shares rise as much as 5%, the most in three months, after reporting stronger organic adjusted Ebitda growth than expected in the first quarter.

Ahold Delhaize shares rise as much as 4.6% after improvement in US sales momentum and the timing of the Easter holiday drove a beat in 1Q Ebit.

Fresenius shares gain as much as 5% after the German health-care company increased its organic revenue growth guidance for the full year.

Siemens Energy shares rise as much as 14% after the company posted forecast-beating orders and boosted its guidance.

Puma shares rise as much as 6.4% after the apparel retailer delivered a 1Q Ebit beat and reaffirmed its guidance for the full year.

Alstom shares gain as much as 11% after the French train maker announced plans for a capital increase of around €1 billion.

Evonik shares climb as much as 2.2% after the chemicals company reported 1Q adjusted Ebitda that beat estimates.

Auto1 shares jump as much as 25% after the German used-car-dealer raised its gross profit forecast for the full year.

Grifols shares advance as much as 5.4% after the Spanish blood plasma firm’s board of directors adopted various resolutions to strengthen corporate governance.

Sabadell shares slip as much as 3.8% after the Spanish bank released a letter sent to its chairman on the weekend from rival BBVA, saying it had no room to improve its takeover offer.

Continental shares fall as much as 1.8% after the German tiremaker’s 1Q Ebit missed the average analyst estimates.

Securitas shares fall as much as 4.5% after the firm reported its latest earnings which analysts say were hit by weak cash performance.

Carl Zeiss Meditec shares drop as much as 6.9%, the most in about a year, after the German medical optics company reported weaker-than-expected results for the second quarter.

“Right now we’re seeing the broadening of performance, especially from the earnings perspective,” Nataliia Lipikhina, head of EMEA equity strategy at JPMorgan Private Bank, said in an interview on Bloomberg TV. “The market wanted to see that earnings in different sectors, not just tech, are delivering.”

Earlier in the session, stocks in Asia were set to halt a four-day winning streak as focus shifted to earnings to validate a recent rally. The MSCI Asia Pacific Index slipped as much as 0.9% after closing at a two-year high in the previous session. Japanese tech firms Sony and Nintendo were among the biggest drags to the gauge, with the latter dropping more than 5% on weak outlook. The country’s benchmarks fell more than 1% in the region’s worst performance. Chinese onshore benchmarks posted their first decline this week amid a warning from Morgan Stanley strategists that the recent rally is likely to abate. Hong Kong stocks also fell. Index heavyweights Tencent and Alibaba are among key tech firms to release earnings next week, and the results will be crucial for the rally to resume.

In FX, the Swedish krona is among the worst performing G-10 currencies, falling 0.4% versus the greenback after the Riksbank cut its benchmark interest rate for the first time in eight years and said it could be reduced twice more in the second half of 2024. The yen weakens 0.5% against the dollar, with USD/JPY around 155.50.

In rates, treasuries were slightly cheaper across the curve with losses led by intermediate- to long-end sectors, steepening curve spreads. US long-end yields are cheaper by 2bps, steepening 2s10s spread by 1.5bp, 5s30s by 0.5bp; the 10-year is around 4.48% with bunds lagging by 1.5bp in the sector amid new record high for Europe’s Stoxx 600 Index after another batch of strong corporate earnings. Supply concession is also a factor for Treasuries with 10-year note sale later Wednesday and 30-year bond auction Thursday. Indeed, the week’s refunding auction cycle continues at 1pm New York time with $42b 10-year new issue one day after Tuesday’s 3-year note sale drew good demand, stopping through by 0.3bp. WI 10-year yield at around 4.48% is 8bp richer than April’s, which tailed by 3.1bp in a poor result.

In commodities, oil prices decline, with WTI falling 1.6% to trade near $77.20. Spot gold drops 0.1%.

Looking at today’s calendar, the US economic data slate includes March wholesale inventories (10am). Fed members’ scheduled speeches include Jefferson (11am), Collins (11:45am) and Cook (1:30pm) From central banks, the Riksbank was the latest western bank to commence an easing cycle cutting rates to 3.75%. Finally in the US, a 10yr Treasury auction is taking place.

Market Snapshot

S&P 500 futures little changed at 5,214.75

STOXX Europe 600 up 0.3% to 515.72

MXAP down 1.0% to 176.52

MXAPJ down 0.4% to 550.52

Nikkei down 1.6% to 38,202.37

Topix down 1.4% to 2,706.43

Hang Seng Index down 0.9% to 18,313.86

Shanghai Composite down 0.6% to 3,128.48

Sensex little changed at 73,495.37

Australia S&P/ASX 200 up 0.1% to 7,804.49

Kospi up 0.4% to 2,745.05

German 10Y yield little changed at 2.44%

Euro down 0.1% to $1.0741

Brent Futures down 1.2% to $82.15/bbl

Gold spot down 0.4% to $2,305.33

US Dollar Index up 0.18% to 105.60

Top Overnight News

Chinese iPhone shipments jumped about 12% in March after Apple Inc. and its retailers slashed prices, official data showed, suggesting efforts to arrest an accelerating decline in sales are yielding early results. BBG

The BOJ may take monetary policy action if yen falls affect prices significantly, governor Kazuo Ueda said on Wednesday, offering the strongest hint to date the currency’s relentless declines could trigger another interest rate hike. Ueda also said the BOJ could raise interest rates sooner than expected if inflation overshoots its forecasts, or risks to the price outlook increases. RTRS

Germany’s industrial production for Mar was a bit better than anticipated, coming in -0.4% M/M (vs. the Street’s -0.7% forecast), although Feb was revised lower (from +2.1% to +1.7%). BBG

Sweden’s central bank lowered rates 25bp (from 4% to 3.75%) and said two additional reductions could happen in H2 (the Riksbank is only the second monetary body from an advanced economy to commence easing since the post-COVID inflation surge after Switzerland’s central bank cut in March). RTRS

Indiana primary results showed Haley performing very well, signaling a large anti-Trump faction of the GOP exists. Politico

Trump’s classified documents trial in Florida has been postponed indefinitely, raising the odds that the current Stormy Daniels/hush money one underway in NYC is the only verdict voters will receive before the election. WaPo

Corporate profits are performing very well (firms beat in Q1 and analysts have been raising estimates for Q2), suggesting an economic downturn won’t occur anytime soon. WSJ

Saudi-backed chip and AI investment firm Alat said it would divest from China if it were asked to do so by the US. The comments came after people familiar said the US revoked licenses allowing Huawei to buy chips from Intel and Qualcomm. BBG

FTX will amass as much as $16.3 billion in cash once it sells all of its assets, far more than it needs to cover what customers lost. The extra will be used to pay them interest but nothing will be left for equity holders. BBG

Earnings

BMW (BMW GY) Q1 (EUR): Revenue 36.61bln (exp. 36.82bln). EBIT 4.05bln (exp. 3.96bln). Automotive revenue 30.94bln (exp. 31.01bln). Automotive EBIT Margin 8.8% (exp. 9.05%). EBT Margin 11.4% (exp. 10.6%). BEV sales +28% Y/Y. 2024 outlook confirmed. Shares -4.5% in European trade

Siemens Energy (ENR GY) Q2 (EUR): FCF 483mln (prev. -294mln Y/Y), Profit before special items 170mln (prev. 41mln Y/Y), Net Profit 108mln (exp. -11mln). Outlook: Expects sales growth 10-12% (exp. +6%), Profit margin of -1% to +1% (prev. guided -2% to +1%). Now expects FCF pretax of up to 1bln (prev. guided negative at up to 1bln). Shares +12.5% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower after the choppy US performance and in the absence of fresh catalysts. ASX 200 lacked firm direction with gains in industrials and energy offset by weakness in miners and financials. Nikkei 225 underperformed as participants digested earnings including disappointing guidance by Nintendo. Hang Seng & Shanghai Comp were ultimately lower amid trade and tech-related frictions after the US revoked export licences that allowed Intel (INTC) and Qualcomm (QCOM) to supply Huawei with semiconductors.

Top Asian News

BoJ Governor Ueda said the BoJ will scrutinise the impact of yen moves on the economy in guiding monetary policy and FX moves could have a big impact on the economy and prices, so could warrant a monetary policy response, while he added the BoJ may need to respond via monetary policy if such impact from yen moves affect trend inflation. Ueda said they expect trend inflation to gradually head towards 2% and will adjust monetary policy as appropriate if trend inflation heads toward 2% as projected or if they see a risk of inflation overshooting their forecast. Furthermore, Ueda said they don’t see yen moves as having a big impact on trend inflation so far but there is a risk the impact could become more significant in the future and they won’t necessarily wait until inflation achieves their forecasts in 1.5 to 2 years to raise rates with the central bank to adjust the degree of monetary support accordingly if trend inflation moves as projected.

Japanese Finance Minister Suzuki said he is watching FX movements with a sense of urgency and won’t comment on forex levels, while he added it is important for currencies to move in a stable manner reflecting fundamentals. Furthermore, he said they will take a thorough response for forex and don’t believe that resources for intervention are limited.

Chinese April Prelim Retail Car Sales -2% Y/Y (vs +6% in March).

BoJ Governor Ueda says Japan’s economy is recovering moderately albeit with some weakness; will guide policy appropriately from perspective of stably and sustainably achieving the price target. Rapid/abrupt and one-sided Yen falls are negative for Japan’s economy are undesirable.

European bourses, Stoxx600 (+0.3%) are almost entirely in the green, with indices initially opening tentatively around the unchanged mark before picking up gradually to session highs throughout the morning. European sectors are mixed, with Food Beverage and Tobacco at the top of the pile, lifted by post-earning strength in AB InBev (+4.4%). Basic Resources is the clear underperformer, given the weakness in underlying metals prices; Autos are also hampered by poor BMW (-4.5%) results. US Equity Futures (ES U/C, NQ U/C, RTY -0.3%) are mixed and trading with little direction, continuing the tentative price action seen in the prior session. Apple (+0.6% pre-market) gains amid reports that its China iPhone shipments rose 12% in March.

Top European News

The BoE should leave rates unchanged at its meeting on Thursday but consider lowering them in June, according to the Times’ shadow MPC.

UK Home Office announced on Tuesday night that it was aware of a technical issue affecting E-gates across the country, while it was working closely with the Border Force and affected airports to resolve the issue. However, Heathrow Airport later stated that all Border Force systems were now running as usual and it did not expect any issues this morning when the operation starts up.

ECB’s Scicluna is to face charges of “fraud and misappropriation,” relating to his time as the Finance Minister of Malta, via Politico citing documents.

Riksbank cuts its Rate by 25bps to 3.75% (as expected by a majority of respondents); Policy rate is expected to be cut two more times during H2 if inflation outlook cuts (bringing total 2024 cuts to 3 vs prev. guided just over 2).

Barclays European Equity Strategy; raises Utilities to Market Weight from Underweight; cuts Energy to Market Weight from Overweight

FX

USD is firmer vs. all peers but to varying degrees. Support for the DXY has in large part been provided by further upside in USD/JPY. Fresh US fundamentals are lacking in what could well be a quiet week ahead of next week’s inflation metrics, though a handful of speakers and supply populate today’s docket. As such, DXY has continued to consolidate around the mid-point of the 105 handle.

EUR is softer vs. the USD but less so than peers with some support via the EUR/GBP and EUR/SEK crosses. Fresh fundamental drivers for the Eurozone are lacking and expectations of a June ECB cut remain firmly anchored. Currently trading around 1.074.

GBP is softer vs. the broadly firmer USD with UK specifics light ahead of tomorrow’s BoE which some are framing as a potential dovish hold. Cable has slipped to the 1.24 handle, going as low as 1.2468.

JPY is losing further ground to the USD with jawboning efforts from Japanese officials futile. 155.41 is the high watermark thus far with the next target a test of 156. CPI next week likely to be the next inflection point for the pair. Commentary from BoJ Governor Ueda sparked some volatility, though was ultimately unreactive to the commentary.

Antipodeans are both softer vs. the USD with AUD lagging alongside downside in metals prices. AUD/USD has extended on yesterday’s downside which has seen the pair dragged from Friday’s post-NFP peak at 0.6647 to a current low of 0.6565.

SEK is losing ground vs. peers as the Riksbank pulls the trigger on a rate reduction and leaves the door open to another two cuts in the second half of the year. Accordingly, EUR/SEK has jumped from 11.691 to a high of 11.7564 but has failed to test the YTD peak at 11.7708.

PBoC set USD/CNY mid-point at 7.1016 vs exp. 7.2202 (prev. 7.1002).

Fixed Income

USTs are a touch softer, in-fitting with the narrative outlined for Bunds above but with USTs yet to meaningfully or lastingly deviate from the unchanged mark in narrow 108-28+ to 109-03 bounds. 10yr supply and Fed speak from Cook, Collins and Jefferson scheduled.

Bunds are under modest pressure as the fixed income complex takes a very slight breather from the bullish action that has been in place since the Payrolls report on Friday. After printing an earlier 131.45 base Bunds have since stabilised around 20 ticks above this.

Gilts are essentially unchanged, and under some very modest pressure at the open which was softer by 15 ticks given bearish leads elsewhere. UK-specific developments light. Overnight, the Times Shadow MPC said the BoE on Thursday should leave rates unchanged. Currently holding around 97.95 towards Tuesday’s close and by extension at the top-end of that session’s 97.48-98.08 bounds.

UK sells GBP 2.5bln 1.50% 2053 Green Gilt: b/c 3.26x (prev. 3.05x), average yield 4.545% (prev. 4.565%), tail 0.6bps (prev. 0.3bps).

Commodities

A downbeat morning for the crude complex with newsflow rather light and Israel’s Rafah operation seemingly not likely to spark a wider conflict as things stand, though the situation remains very fluid. Brent July slipped from USD 83.05/bbl to 81.96/bbl, with some flagging the 200 DMA around USD 81.95/bbl.

Another soft session for precious metals, likely as Israel’s “limited” Rafah operation has failed to spark a regional war, with international efforts also underway to cushion the impact of the incursion. XAU trades towards the bottom of a 2,303.75-2,321.53/oz range.

Lower across the board for base metals amid a firmer Dollar and following the downbeat mood in Chinese markets overnight.

US Private Energy Inventory Data (bbls): Crude +0.5mln (exp. -1.1mln), Cushing +1.3mln, Gasoline +1.5mln (exp. -1.3mln), Distillate +1.7mln (exp. -1.1mln).

Russian Deputy PM Novak said there are no discussions about an oil output increase at OPEC+.

EU Ambassadors will today be discussing a new package of sanctions against Russia, where the focus will be on restricting LNG profits, via Politico.

Indonesia’s President said copper concentrate export permits for Freeport and Amman will be extended with the details of the extension still being calculated, according to Reuters.

Morgan Stanley has removed its USD 4/bbl risk premium from Brent forecasts, reverts forecast back to forecast of USD 90/bbl by Q3; expects OPEC to extend current production agreement at June 1st meeting, eventually to year-end, including voluntary cuts.

China Industry Ministry says the draft rules would guide Lithium battery firms to reduce manufacturing projects that “purely” expand production capacity

Geopolitics: Middle East

“IDF: We are conducting a precision operation in limited areas east of Rafah in the southern Gaza Strip”, according to Asharq News. Additionally, “IDF says it continues operations east of Rafah”, via Al Arabiya, “IDF: Hamas military infrastructure destroyed in the Rafah crossing area”.

Israeli artillery shelling was reported east of Rafah in the southern Gaza strip, according to Al Jazeera.

Hamas said Cairo talks are the ‘last chance’ for Israel to recover hostage talks, according to Al Arabiya. Furthermore, a Hamas official said the group set red lines in the ceasefire negotiations that cannot be conceded, according to Sky News Arabia.

White House thinks the Israeli operation to capture the Rafah crossing doesn’t cross President Biden’s “red line” that could lead to a shift in US policy towards the Gaza war although the US warned that if it broadens or gets out of control and Israeli forces go into the city of Rafah itself, it will be a breaking point, according to US officials cited by Axios.

CIA Director Burns plans to travel to Israel on Wednesday for talks with Israeli PM Netanyahu and Israeli officials, according to a source cited by Reuters.

Geopolitics: Other

Ukrainians hit a fuel depot in the Russian-controlled city of Luhansk, according to sources via X.

Russia launched an air attack on Kyiv, according to Ukraine’s military. It was later reported that Russia targeted energy facilities in Kyiv, Poltava, Lviv and other regions, according to Ukraine’s Energy Minister. Furthermore, Ukraine’s largest private electricity company said the Russian attack caused serious damage at three thermal power plants.

Taiwan’s leader is open to dialogue with Beijing on an equal footing, according to Taipei’s de facto envoy to the US under President-elect Lai cited by SCMP.

US Event Calendar

07:00: May MBA Mortgage Applications, prior -2.3%

10:00: March Wholesale Trade Sales MoM, est. 0.8%, prior 2.3%

10:00: March Wholesale Inventories MoM, est. -0.4%, prior -0.4%

Fed speakers

11:00: Fed’s Jefferson Speaks About Careers in Economics

11:45: Fed’s Collins Speaks to MIT Students

13:30: Fed’s Cook Speaks on Financial Stability

DB’s Jim Reid concludes the overnight wrap

As summer finally threatens to arrive here in London, even if I’m looking out on fog this morning as I type, markets continued their advance yesterday, with the risk rally continuing post what was deemed to be a very dovish payroll print last Friday. As recently as April 25th, 10yr yields peaked at 4.735% intra-day but a -28bps rally to 4.46% has come alongside a more optimistic view on rate cuts this year again. Obviously Fed Chair Powell helped this by playing down the prospect of further rate hikes at last week’s FOMC. 10yr yields have rallied around 24bps since their peak on FOMC day and yields have now fallen for a 5th consecutive session. That’s the longest run of declines since August.

Those moves on the rates side supported risk assets too, with the STOXX 600 (+1.14%) and the FTSE 100 (+1.22%) both hitting a new record yesterday as UK equities resumed trading after the holiday. The advance was more moderate in the US, but the S&P 500 (+0.13%) still posted a 4th consecutive advance despite underperformance from tech stocks. It now means the S&P has posted its strongest 4-day rally since November, having risen by +3.37% since the close last Wednesday after Powell’s press conference. Moreover, it’s worth noting that the equal-weighted S&P 500 managed to post a stronger +0.28% gain, since the Magnificent 7 (-0.50%) dragged down the rest of the index amidst larger declines from Tesla (-3.76%) and Nvidia (-1.72%). Otherwise, Disney (-9.51%) was a standout after their earnings release, and was the second-worst performer in the S&P 500 yesterday.

Asian markets are running out of a bit of steam this morning though with the Nikkei (-1.43%) the biggest underperformer across the region, slipping from multi-week highs while the CSI (-0.66%), the Shanghai Composite (-0.41%), the Hang Seng (-0.16%) and the KOSPI (-0.12%) are all lower. US stock futures are pretty much flat though with Treasury yields back up 0.5bps-1.5bps across the curve.

In FX, the J apanese yen continues to struggle trading -0.29% lower at 155.16 versus the dollar despite the B OJ Governor Kazuo Ueda stating that the central bank may take appropriate monetary action if yen moves significantly impact Japan’s inflation. Nothing particularly new in those comments but the government’s popularity is also under pressure over the weak currency and cost of travelling to, and importing from, abroad. Trade figures for April are out tomorrow.

Back to markets and one asset that continues to struggle is oil. Brent Crude was down another -0.35% to $83.04/bbl yesterday and is trading down at $82.74 this morning. We peaked above $92 in the second week of April after Middle East tensions ramped up. This reversal has been supportive for the broader market, since its helped to ease fears about more persistent inflation. For instance, US 5yr inflation swaps were down another -0.8bps yesterday to 2.49%. This is the first time since March that they’ve closed beneath 2.5%, having fallen for 7 of the past 8 sessions.

We’ll have to wait another week for the next US CPI release and the latest on inflation, but in the meantime, and as discussed at the top, sovereign bonds posted a fresh rally on both sides of the Atlantic yesterday. In the US, that saw yields on 10yr Treasuries (-3.0bps) decline to 4.46%, whilst 2yr yields were -0.2bps to 4.83%. 2yr yields had been as low as 4.80% intra-day, with a modest rise later on in part following some hawkish comments from Minneapolis Fed President Kashkari (a non-voter this year). He said in a blog post that “ with inflation in the most recent quarter moving sideways, it raises questions about how restrictive policy really is.” But Kashkari was already one of the most hawkish-sounding members on the FOMC, so the comments have to be taken in context. Year-end Fed pricing was unchanged on the day, with 44bps of cuts priced in.

Over in Europe, the focus continued to be on the ECB, with anticipation mounting that they’ll cut rates at their next meeting in 4 weeks’ time. That contributed to a fresh rally for sovereign bonds, with the 10yr bund yield (-4.9bps) falling for a 4th consecutive day to 2.42%. That was echoed across the continent, with yields on 10yr OATs (-5.2bps) and BTPs (-2.9bps) also moving lower, whilst those on 10yr gilts (-9.9bps) saw a larger decline as they caught up with the previous day’s moves.

There wasn’t much other data yesterday, although we did get the UK construction PMI for April, which hit a 14-month high of 53.0 (vs. 50.4 expected). By contrast, in Germany the construction PMI fell to 37.5, whilst the factory orders data for March contracted by -0.4% (vs. +0.4% expected). So some negative news after what have been more encouraging recent growth data for Europe’s largest economy of late. Finally, Euro Area retail sales were up +0.8% in March (vs. +0.7% expected).

To the day ahead, and data releases include German industrial production and Italian retail sales for March. From central banks, the Riksbank will be making its latest decision, and we’ll hear from Fed Vice Chair Jefferson, the Fed’s Collins and Cook, and the ECB’s Wunsch and De Cos. Finally in the US, a 10yr Treasury auction is taking place.

Tyler Durden

Wed, 05/08/2024 – 08:26