Latest News

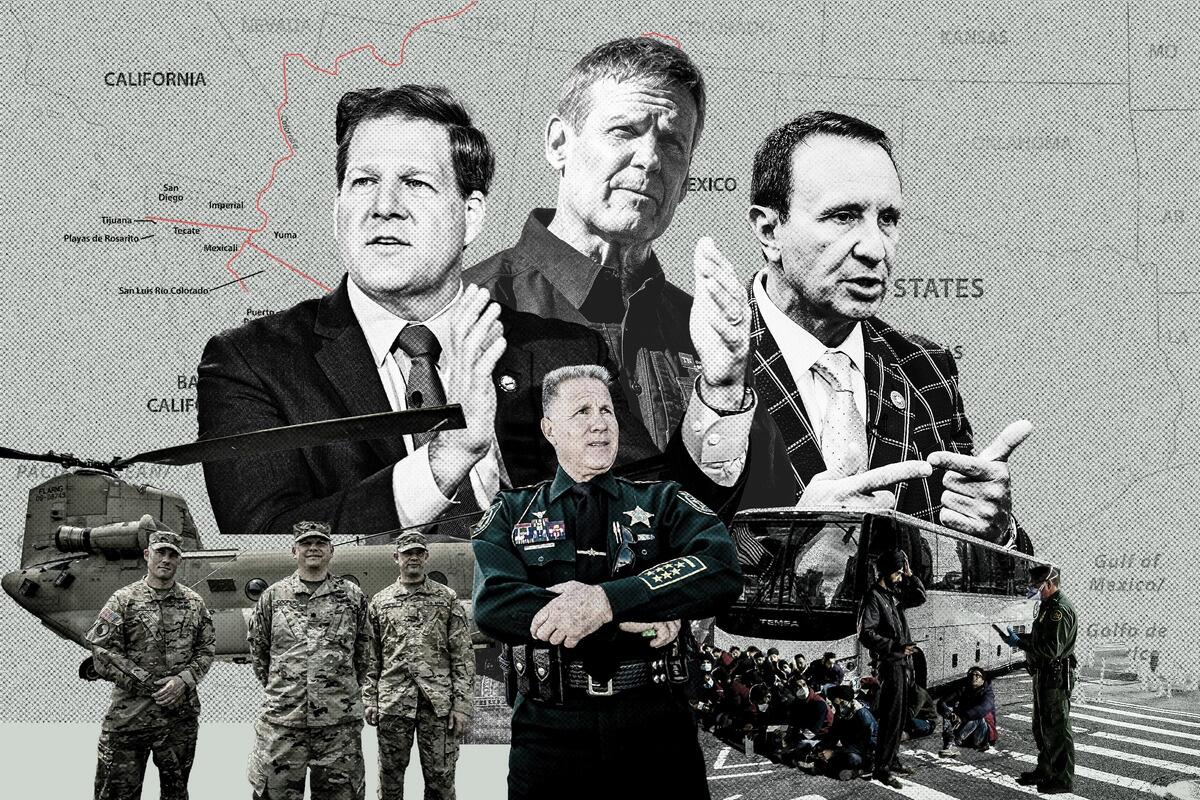

These States Are Making It Illegal For Illegal Immigrants To Enter

These States Are Making It Illegal For Illegal Immigrants To Enter

Authored by Darlene McCormick Sanchez via The Epoch Times (emphasis ours),

Conservative states across the country—Florida, Iowa, Louisiana, Tennessee, Georgia, and Oklahoma—are taking border security matters into their own hands, proposing or passing legislation targeting illegal immigration.

(Illustration by The Epoch Times, Shutterstock, Getty Images)

{kind=link}

The Oklahoma legislature just passed a bill designed to prohibit illegal immigrants from entering or living in the state.

HB 4156 states: “A person commits an impermissible occupation if the person is an alien and willfully and without permission enters and remains in the State of Oklahoma without having first obtained legal authorization to enter the United States.”

The bill passed the state House and Senate by wide margins and Gov. Kevin Stitt, a Republican, is expected to sign it into law.

The legislature declared the issue a crisis in the state and stated in the bill: “Throughout the state, law enforcement comes into daily and increasingly frequent contact with foreign nationals who entered the country illegally or who remain here illegally.

“Often, these persons are involved with organized crime such as drug cartels, they have no regard for Oklahoma’s laws or public safety, and they produce or are involved with fentanyl distribution, sex trafficking, and labor trafficking.”

Under the new law, a conviction related to “impermissible occupation” would be considered a misdemeanor, punishable by up to one year in a county jail, a fine of up to $500, or both.

Subsequent offenses are felonies, punishable by up to two years in prison, a fine of up to $1,000, or both.

Illegal immigrants who are barred from the country or have been issued a removal order by an immigration judge, and then enter Oklahoma will face a felony charge carrying a possible sentence of up to two years in prison, a fine of up to $1,000, or both.

In all instances, those found guilty must leave Oklahoma within 72 hours of being convicted or released from custody.

{kind=link}

The law requires police to collect fingerprints, photographs, and biometric data, which will be cross-checked with Oklahoma State Bureau of Investigation databases.

“The failure of the federal government to address this issue … has turned every state into a border state,” said bill sponsor state Rep. Charles Mr. McCall said in a statement.

“Those who want to work through the process of coming to our country legally are more than welcome to come to Oklahoma; we would love to have them here. We will not reward [illegal immigration] in Oklahoma, and we will protect our state borders.”

U.S. border authorities have apprehended more than 9 million illegal immigrants nationwide under President Joe Biden, according to Customs and Border Protection (CBP) data.

Under the administration’s catch-and-release policy, many have been released into the United States and have taken up residence all over the country.

Texas’ law, Senate Bill 4, makes it a state crime to enter Texas outside legal ports of entry.

The new law was set to go into effect in March, but has been blocked and is currently tied up in the courts.

New Iowa, Tennessee, and Georgia Laws

Earlier this month, Iowa’s Republican Gov. Kim Reynolds signed Senate File 2340 into law.

The new law, which goes into effect July 1, makes it a misdemeanor to be in the state or attempt to enter the state after being deported, denied admission to the United States, or if an individual has an outstanding deportation order.

Being in the state illegally becomes a felony under certain circumstances such as the accused having two or more misdemeanor convictions involving drugs or crimes against a person.

As with the Texas law, it gives judges the discretion to drop the charges if the illegal immigrant agrees to return to the country from which he or she entered the United States.

“Those who come into our country illegally have broken the law, yet Biden refuses to deport them,” Ms. Reynolds stated in a news release.

“This bill gives Iowa law enforcement the power to do what he is unwilling to do: enforce immigration laws already on the books.”

Tennessee Gov. Bill Lee signed a new law this month that requires law enforcement agencies to communicate with federal immigration authorities if they discover people are in the country illegally, requiring in most cases cooperation in the process of identifying, catching, detaining, and deporting them.

{kind=link}

The law takes effect July 1.

“When there is an interaction with law enforcement, it’s important that the appropriate authorities are notified of the status of that individual,” Mr. Lee, a Republican, told reporters after signing the bill into law. “I think that makes sense. So, I’m in support of that legislation.”

Members of the Tennessee House blamed President Biden’s lack of border enforcement for the necessity of the law.

“President Biden’s administration has delivered this pain to our doorsteps,” Tennessee state Rep. Chris Todd said on the House floor.

In Georgia, lawmakers passed House Bill 1105 that would require jailers to check the immigration status of inmates.

The bill is part of an ongoing political response to the February slaying of nursing student Laken Riley on the University of Georgia campus, allegedly by an illegal immigrant from Venezuela.

The man, Jose Antonio Ibarra, was arrested in February on murder and assault charges in the death of the 22-year-old.

Immigration officials say Mr. Ibarra, 26, crossed into the United States illegally in 2022. The Department of Homeland Security confirmed to Sen. Lindsey Graham(R-S.C.) that Mr. Ibarra was paroled into the country illegally due to “capacity problems” at border detention facilities

The Georgia bill was sent to Republican Gov. Brian Kemp’s desk on April 3 and awaits his signature, at which time most measures would take effect immediately.

Louisiana, Arizona, New Hampshire

Texas’ neighbor, Louisiana, is considering the passage of SB 388, a GOP-led bill that would allow state police to arrest suspected illegal immigrants within the state.

The law passed the chamber on April 8 along party lines and headed to the House, also controlled by Republicans.

“Louisiana is one step closer to securing our border and addressing our illegal immigration crisis,” Republican state Sen. Valarie Hodges, the bill’s sponsor, posted on X.

{kind=link}

The battleground state of Arizona passed a law similar to Texas’ HB 4, but its Democratic Gov. Katy Hobbs vetoed it.

That inspired the Legislature to draft a ballot measure to be put to voters in November that would require businesses to use E-verify. E-verify is a voluntary federal online service for employers to check an employee’s eligibility to work in the United States against Department of Homeland Security and Social Security records.

New Hampshire, which is Republican-led, passed SB 504 allowing police to bring criminal trespassing charges against people suspected of illegally entering the United States from Canada. The measure must be approved by the House to advance.

Cities and Counties

Cities and counties in red and blue states are also pushing back in creative ways to stop illegal immigrants from coming into their jurisdictions.

“They’re basically dumped on their doorstep,” said Jessica Vaughan, director of policy studies at the Center for Immigration Studies, a “pro-immigrant, low-immigration” think tank.

In June 2023, New York City under Democratic Mayor Eric Adams sued more than 30 New York local governments alleging they issued unlawful executive orders prohibiting temporary housing for illegal immigrants in their jurisdictions.

Counties such as Orange and Rockland in upstate New York were successful in using local zoning laws to stop the mayor from busing illegal immigrants to live in their hotels.

The state Supreme Court granted Rockland a temporary restraining order against the mayor’s plan after the county argued that local zoning laws bar hotels from operating as shelters.

Orange County was granted a similar ruling.

Likewise, zoning was used by the city of Taunton, Massachusetts, to stop illegal immigrants from living in hotels, Ms. Vaughan said.

In May 2023, the state was paying millions of dollars to house some 120 homeless and migrant families at a local hotel long-term.

{kind=link}

Taunton city leaders filed a lawsuit against the hotel, claiming it violated its occupancy limit for nearly four months. The city aims to collect $114,600 in fines.

Residents in these small communities often struggle with housing and obtaining services that illegal immigrants get for free, Ms. Vaughan noted.

“Now paying taxes, essentially, to support these illegal migrants in their town. The schools have to accommodate them. And that’s a huge cost on the local taxpayers,” she said.

In Colorado’s Mesa County, commissioners passed a resolution in February declaring the county a “non-sanctuary county,” and denying shelter and services to illegal aliens sent there by the state or federal government, she said.

Commissioners also passed a resolution to send a letter to Denver Mayor Mike Johnston informing him the county doesn’t plan to help the city deal with its illegal immigrant surge.

Ms. Vaughan said that she believes other states are waiting to see what happens with some of Texas’ laws, such as SB 4, which are aimed at deterring illegal immigration.

“I think the feeling among most state and local officials that I’ve talked to about it is that they are watching and waiting and hoping that the court will draw some boundaries for them on what they can and cannot do,” she said.

Florida’s Laws

When it comes to making life more difficult for illegal immigrants through legislation, Florida has proven as aggressive as Texas.

Besides beefing up law enforcement to help the U.S. Coast Guard spot migrants and sending the Florida National Guard to Texas, Florida Gov. Ron DeSantis has approved laws to deter illegal aliens from staying in the Sunshine State.

The Republican governor signed SB 1718 in 2023, which was criticized by the left as one of the most anti-illegal immigrant pieces of legislation in the country.

Read more here…

Tyler Durden

Fri, 04/26/2024 – 12:45

20% Of Retail Milk Samples Positive For Bird Flu: FDA

20% Of Retail Milk Samples Positive For Bird Flu: FDA

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

One in five samples of milk from grocery store shelves tested positive for the highly pathogenic avian influenza, the U.S. Food and Drug Administration (FDA) announced late April 25.

A dairy cow at a dairy farm in Ohio, on December 12, 2014. (Aaron Josefczuk/Reuters)

{kind=link}

In a brief 237-word update, the FDA said that initial results from a national commercial milk sampling study “show about 1 in 5 of the retail samples tested are quantitative polymerase chain reaction (qPCR)-positive for HPAI viral fragments, with a greater proportion of positive results coming from milk in areas with infected herds.”

The FDA has refused to disclose how many samples it tested and from which stores the samples came, and a Freedom of Information Act request for the information has not yet yielded results.

Thirty-three cattle herds across eight states—Idaho, Kansas, Michigan, New Mexico, North Carolina, Ohio, South Dakota, and Texas—have tested positive for avian influenza, commonly known as the bird flu, according to the U.S. Department of Agriculture. Poultry in Minnesota and a person in Texas have also become infected with the same genotype of the H5N1 avian influenza strain found in cattle.

Authorities have stressed that positive results from qPCR testing do not mean the pasteurized milk contains intact virus, because the testing can return positive based on fragments of residual virus.

“Additional testing is required to determine whether intact pathogen is still present and if it remains infectious, which would help inform a determination of whether there is any risk of illness associated with consuming the product,” the FDA said.

Testing includes injecting eggs with samples that tested positive and seeing whether any active virus replicates.

In another round of testing, conducted by a team from Ohio State University, 58 of 150 milk samples gathered from grocery stores across six states tested positive for bird flu.

“We’ve screened them for the presence of influenza genetic material, so the viral RNA. Those that have tested positive, we have been forwarded to St. Jude Children’s Research Hospital, where they are conducting studies to see if there’s a viable virus in there. To date, none of them have been viable, but certainly they give the indication that there is viral genetic material in the region,” Dr. Andrew Bowman, an associate professor at Ohio State University, told the Bovine Veterinarian magazine.

“The fact that you can go into a supermarket and 30 percent to 40 percent of those samples test positive, that suggests there’s more of the virus around than is currently being recognized,” Richard Webby, a virologist at St. Jude’s, told STAT News.

The FDA has said it will release more details about the testing in the future. Raw milk from farms with affected cows has also tested positive for bird flu.

Authorities initially said that pasteurized milk was definitely safe but have since acknowledged that they’re not sure whether milk in grocery stores contains live bird flu virus. The FDA announced Tuesday that some samples tested positive for the influenza.

Officials say it’s still safe to drink milk but some outside experts, including former U.S. government official Rick Bright, have said they’re going to hold off until more information is made public about the outbreak.

The U.S. Department of Agriculture only required testing dairy cows showing symptoms of the flu but, starting Monday will require lactating cows to test negative before being moved across state lines.

The flu originated in birds but has since moved to other animals, including cattle and goats.

The person in Texas, and an individual in Colorado who became sick in 2022, are the only humans with confirmed cases of the H5N1 version in the United States.

Monitoring of people who have come into contact with animals has only covered 44 people so far, Sonja Olsen, an epidemiologist with the U.S. Centers for Disease Control and Prevention, told an Association of State and Territorial Health Officials webinar this week. Twenty-three people who showed symptoms were tested. The person in Texas, a farm worker, has been the only person to test positive so far.

Tyler Durden

Fri, 04/26/2024 – 12:05

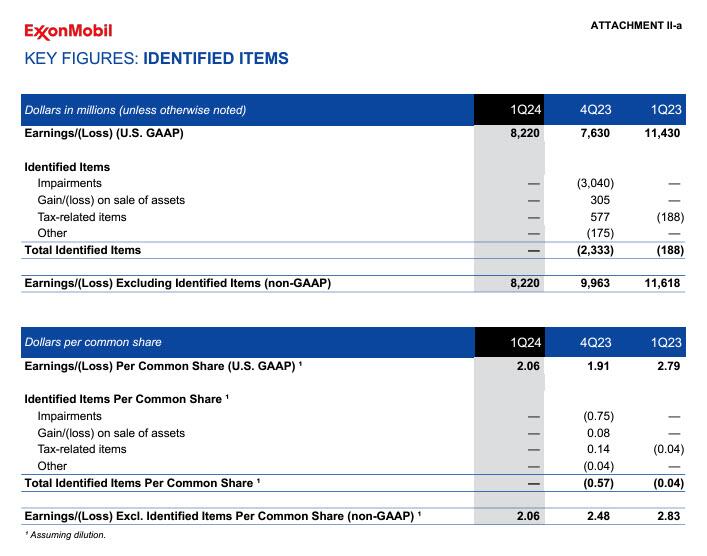

Exxon Tumbles On One-Time EPS Charges Despite Surge In Cash Flow, Buyback Boost

Exxon Tumbles On One-Time EPS Charges Despite Surge In Cash Flow, Buyback Boost

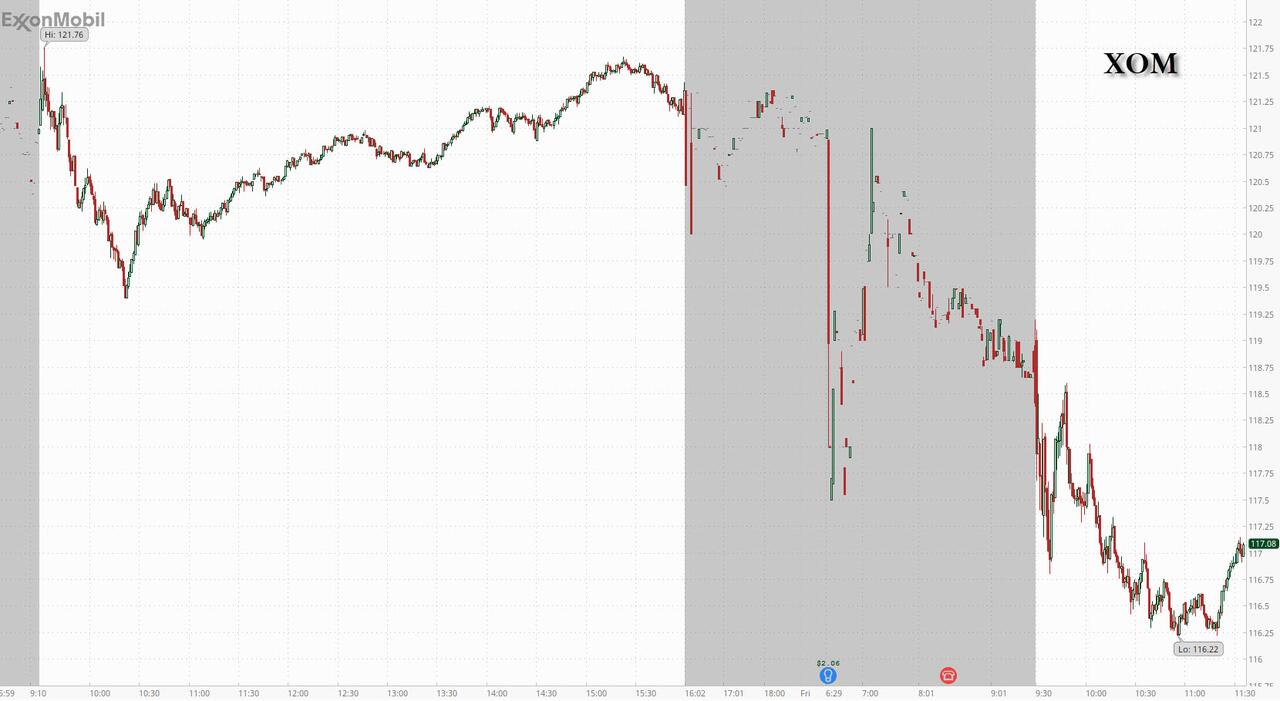

With oil prices enjoying a powerful renaissance in recent months amid mounting supply concerns, declining inventory and the growing possibility that China’s economy may finally kickstart, energy giants such as Exxon and Chevron had enjoyed a similar rebound in their stock price, and in fact XOM hit a record high as recently as 2 weeks ago. Which is why many were looking to today’s earnings reports by the largest US energy company to see if the numbers would validate the rebound in sentiment and, of course, price.

So here is what Exxon reported today for the first quarter:

EPS of $2.06, down from 2.83 a year ago, and missing consensus estimates of $2.19, as a result of delayed bump in commodity prices (which however will lift results in Q2) and a spike in non-cash charges

{kind=link}

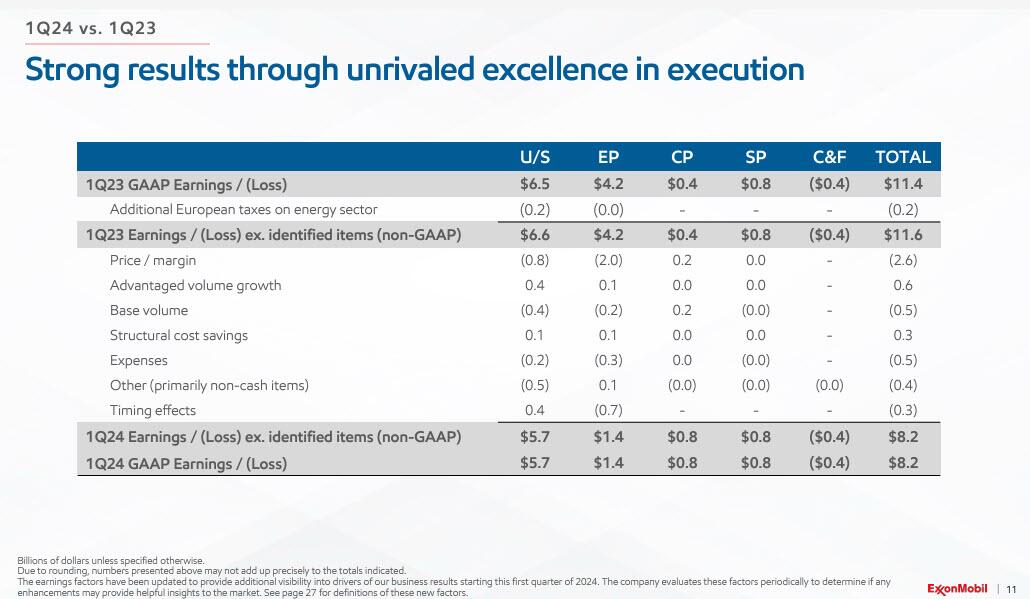

The Net Income number was $8.22 billion, down from $11.618 billion a year ago, with weakness in Upstream and Energy products hitting the bottom line number, coupled with an increases in expenses. The biggest factor behind the drop in earnings was a $2.6 billion hit to price/margin due to lower energy prices in Q1. However, with Brent now well above year ago levels and rising, what XOM lost in Q1 it will more than make up in Q2 absent a collapse in the energy market.

{kind=link}

A breakdown by the various operating segments, reveals that price and margin were indeed the biggest culprits for declining earnings.

{kind=link}

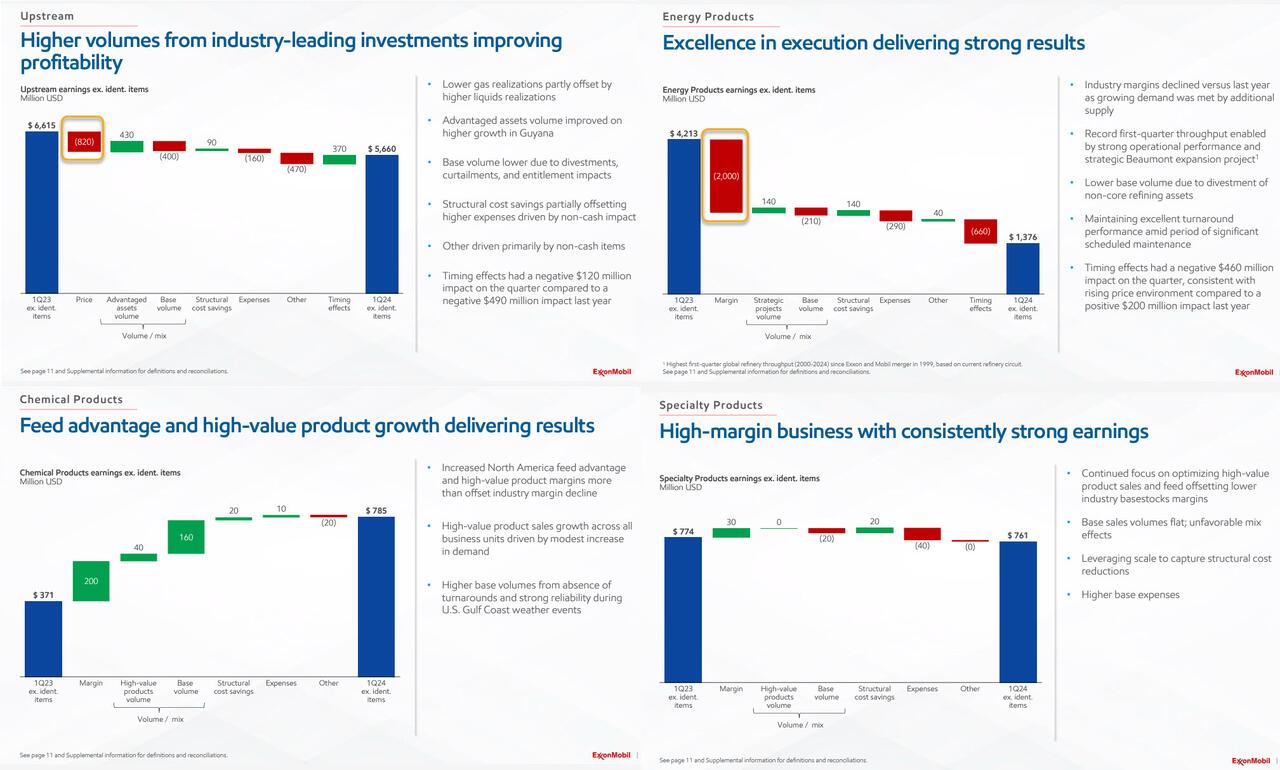

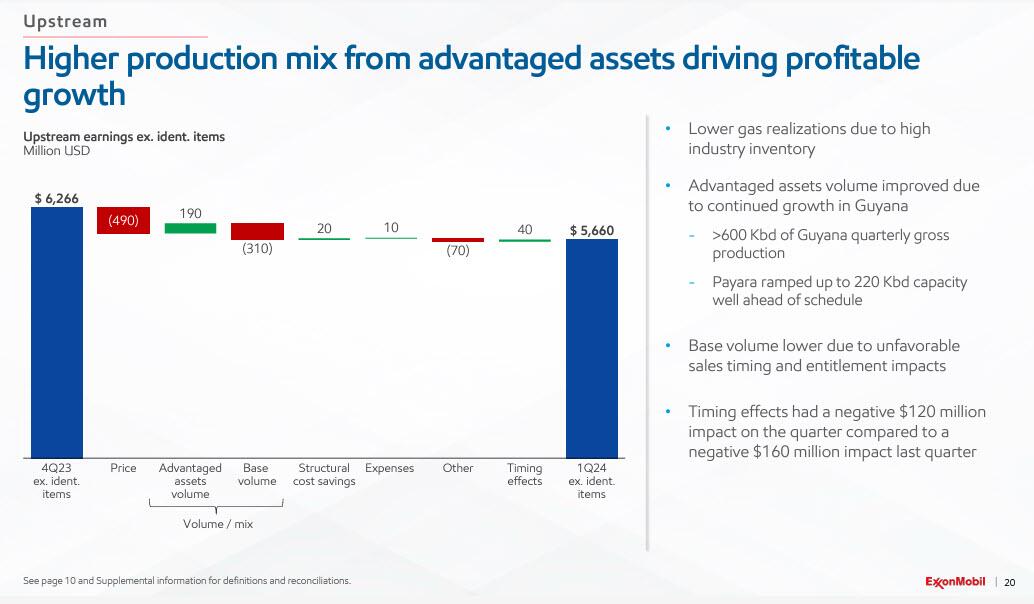

Taking a closer look at the company’s two main divisions, Upstream and Energy products, the company provided the following detail for the somewhat disappointing earnings here:

Starting with Upstream:

Lower gas realizations due to high industry inventory

Advantaged assets volume improved due to continued growth in Guyana

>600 Kbd of Guyana quarterly gross production

Payara ramped up to 220 Kbd capacity well ahead of schedule

Base volume lower due to unfavorable sales timing and entitlement impacts

Timing effects had a negative $120 million impact on the quarter compared to a negative $160 million impact last quarter

{kind=link}

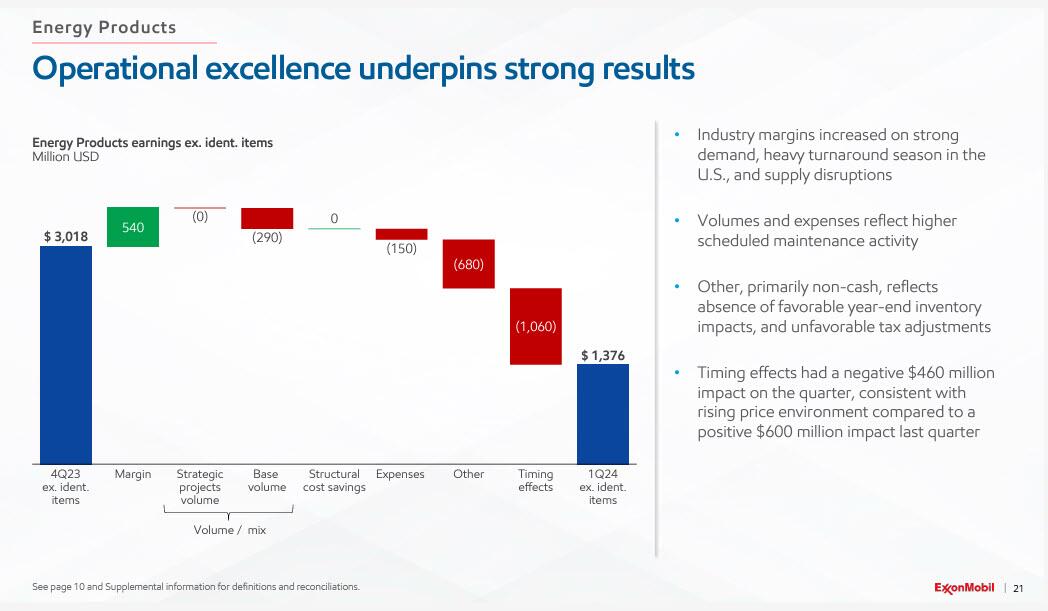

Energy products, where we saw the bulk of the earnings delta (some $1.7BN in earnings reductions between Q4 and Q1), was more interesting as Exxon attributed the slide to three primary drivers:

Volumes and expenses reflect higher scheduled maintenance activity

Non-cash charges which reflected the absence of favorable year-end inventory impacts, and unfavorable tax adjustments

Finally, timing effects which had a negative $460 million impact on the quarter, consistent with rising price environment compared to a positive $600 million impact last quarter.

{kind=link}

“Any given quarter we’ll have a number of non-cash, just a bit more unusual expenses that kind of ebb and flow,” CFO Kathy Mikells told BBG in an interview. “This quarter we had a number of small ones that added up together to be more significant and that’s difficult for analysts to model.”

“We continue to bring projects in more quickly and under budget so we’ve just had great execution in Guyana,” Mikells said, noting that gross daily production is now more than 600,000 barrels, up from 440,000 in the final three months of 2023.

Exxon’s accounting charges were non-cash items associated with tax and inventory balance sheet adjustments, Mikells said. The company also had higher expenses from scheduled maintenance at its facilities.

Some more highlights from the report:

Exxon started output at Payara, its third Guyanese development, ahead of schedule late last year, adding 220,000 barrels of daily supplies that earn profits even if crude plunges to the $35 mark.

Achieved quarterly gross production of more than 600,000 oil-equivalent barrels per day in Guyana and reached a final investment decision on the sixth major development.

Net production was 47,000 oil-equivalent barrels per day lower than the same quarter last year with the growth in advantaged Guyana volumes more than offsetting the earnings impact from lower base volumes due to divestments, government-mandated curtailments and unfavorable entitlement effects.

Excluding the impacts from divestments, entitlements, and government-mandated curtailments, net production grew 77,000 oil-equivalent barrels per day driven by the start-up of the Payara development in Guyana.

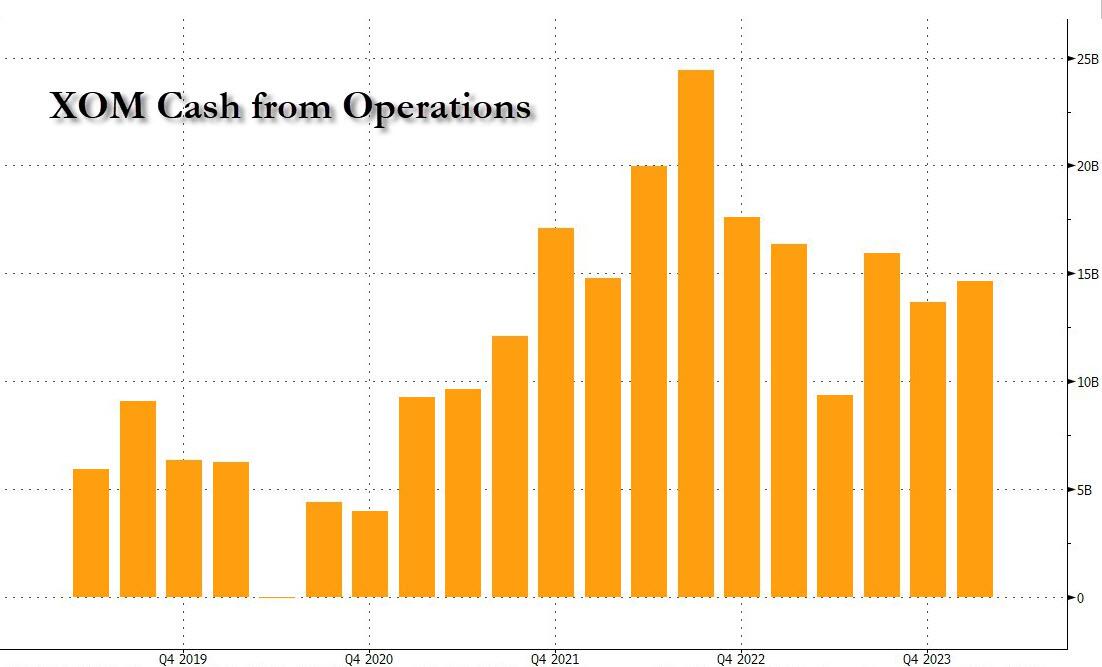

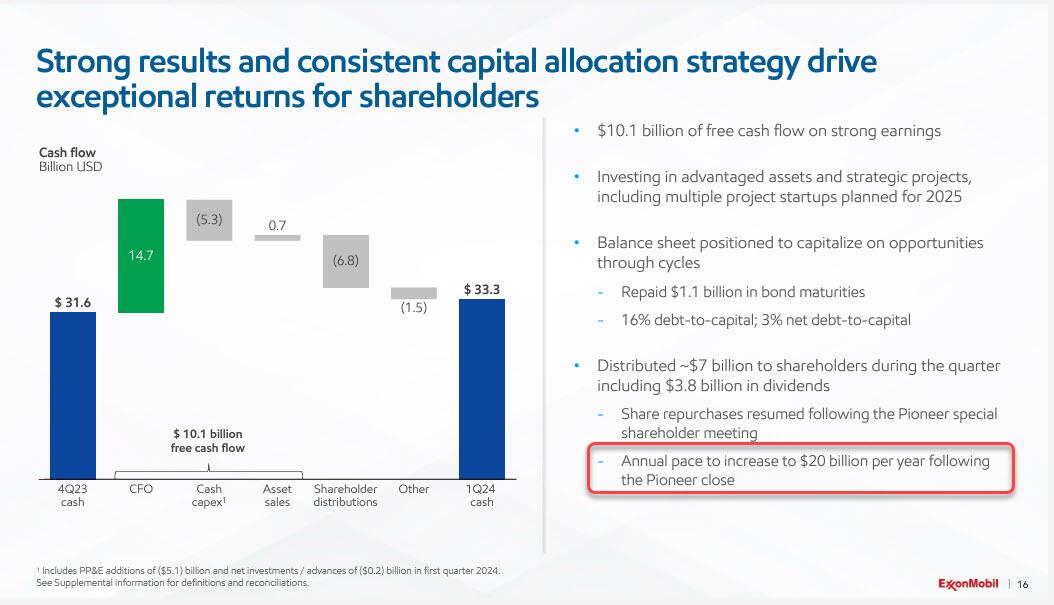

What is remarkable is that even though earnings missed mostly on the timing effect of commodity price increases and one-time charges, which has sent the stock tumbling this morning, the company still managed to blow away expectations for cash generation: in Q1, cash from operations jumped to $14.7 billion, $1 billion higher than Q4 2023 and also $1 billion higher than forecasts, boosted by the more than 35% uplift in Guyanese crude production.

{kind=link}

This in turn led to a $1.8 billion increase in the company’s cash balance despite $6.8 billion in shareholders distributions including $3.8 billion in dividends.

Exxon’s capital spending was $5.8 billion in the first quarter, a third lower than the previous three month period when the company incurred some added Guyana costs. If that level of spending is repeated for the rest of the year, annual capital expenditure would come in at the low end of the company’s $23 billion to $25 billion guidance, and in a market where capital efficiency is extremely rewarded, it likely means that new all time highs are just weeks if not days away.

More importantly, XOM says that it is on pace to increase buybacks to $20 billion following the close of the Pioneer acquisition, some time in Q2.

{kind=link}

Exxon’s stellar performance in Guyana explains why arch-rival Chevron wants to get into the project via a $53 billion takeover of Hess, which has a 30% stake. Exxon claims it has a right-of-first refusal over Hess’s stake while Chevron says that doesn’t apply because its deal is a corporate merger.

Arbitration is still in its “very early days,” Mikells said. Each side has chosen one arbitrator who will sit on a panel of three, she said. Hess this week extended the closing date of its deal with Chevron by six months to October.

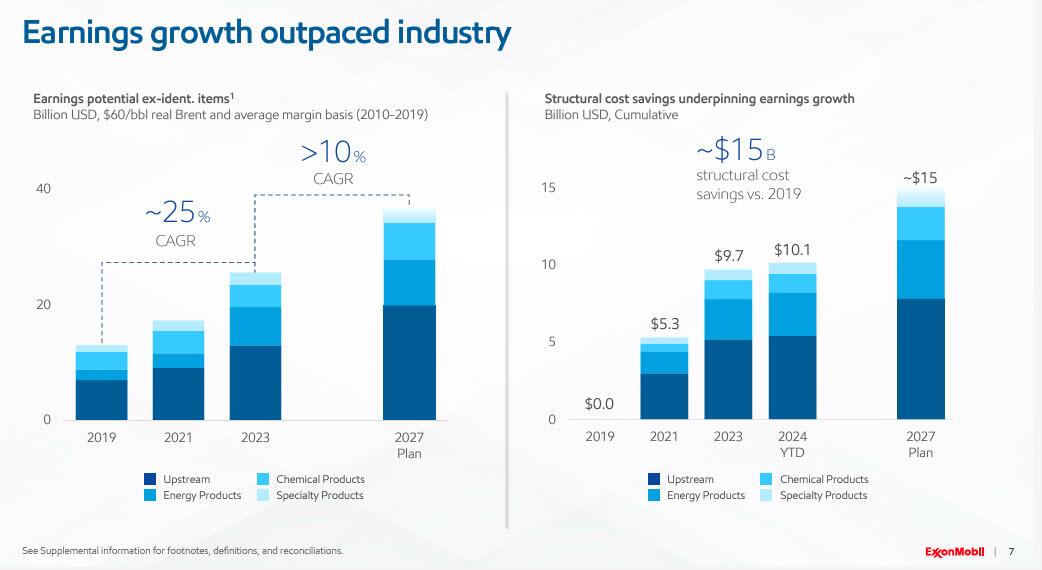

Finally looking ahead, the company forecast that it is on track to more than double upstream profits by 2027…

{kind=link}

… and with cost-savings expected to save another $5BN in spending by 2027 (a total of $15BN vs 2019), this translates into a stellar 10% CAGR in bottom line earnings, and about $10BN in incremental earnings potential by 2027.

{kind=link}

So in its infinite wisdom, when faced with a company that is generating more cash than 99% of companies – and is not reliant on hype and chatbots to keep growing but good, old-fashioned energy which may be boring but is what keeps the world turning – this morning the algos decided to dump their Exxon shares sending the stock some 4% lower, and allowing anyone who pays attention to load up on the dip.

{kind=link}

The XOM Q1 investor presentation is below (pdf link)

Tyler Durden

Fri, 04/26/2024 – 11:45

‘For Your Own Safety’: USC Cancels Commencement To Avoid Pro-Palestinian Protesters

‘For Your Own Safety’: USC Cancels Commencement To Avoid Pro-Palestinian Protesters

Citing safety concerns amid nationwide campus protests against Israel’s conduct of the war in Gaza, the University of Southern California on Thursday announced that its 2024 graduating class will not have the traditional main commencement ceremony that brings all graduates together:

“With the new safety measures in place this year, the time needed to process the large number of guests coming to campus will increase substantially. As a result, we will not be able to host the main stage ceremony that traditionally brings 65,000 students, families, and friends to our campus all at the same time and during a short window from 8:30 a.m. to 10 a.m.”

This news comes on the heels of the university’s controversial declaration that it wouldn’t allow its Muslim valedictorian to deliver a speech to her classmates — a decision that inflamed tensions and prompted an outcry against what was seen by many as an act of censorship and excessive deference to pro-Israel groups.

More immediately, the cancellation also comes on the heels of mass arrests on USC’s campus on Wednesday. More than 90 people were carted off as police cleared protesters from their “occupation” of Alumni Park. As at Columbia University and elsewhere, the protesters are demanding that USC divest from Israel, much as an earlier generation of activists sought similar divestments from apartheid South Africa.

Cops arrest protestors at USC pic.twitter.com/KH7kbKmlEv

— Daily Caller (@DailyCaller) April 24, 2024

On a statement to the campus on Wednesday, USC Provost Andrew Guzman noted that protesters — many of the whom “do not appear to be affiliated with USC”– failed to comply with direction to remove tents from the property. He also said protesters “actions have escalated to include acts of vandalism, defacing campus buildings and structures, as well as physical confrontation.”

Earlier this month, USC announced that its 2024 valedictorian is Asna Tabassum, a self-described first-generation South Asian-American Muslim who is a biomedical engineering major and resistance-to-genocide minor (details on that discipline here). Her selection sparked an immediate uproar from Zionist groups, including Trojans for Israel, which “advocates for the vitality of the US-Israel relationship,” and We Are Tov, which also promotes support for Israel.

Tabassum’s detractors pointed to her social media history, with Trojans for Israel accusing her of “openly traffic[king] antisemitic and anti-Zionist rhetoric.”

Her supposedly disqualifying expressions included:

Sharing a link to a slideshow on “what’s happening in Palestine and how to help.” The presentation called for “one Palestinian state” and “the complete abolishment of the state of Israel,” according to the Times of Israel.

Linking to a site that characterizes Zionism as a “racist settler-colonial ideology.”

Students and faculty protesting USC’s cancellation of valedictorian Asna Tabassum’s commencement speech (Alan Mittelstaedt via LAist)

{kind=link}

USC promptly caved to pro-Israel outcry: On April 16, it announced it had canceled Tabassum’s speech because “discussion related to the selection of our valedictorian has taken on an alarming tenor” and that “the intensity of feelings…has grown to include many voices outside of USC and has escalated to the point of creating substantial risks.” At the same time, USC also cancelled appearances by speakers and honorees that included Billie Jean King and “Crazy Rich Asians” director Jon Chu.

After the USC decision, Tabassum issued a statement noting that, via her resistance to genocide minor — which emphasizes the Holocaust — “[I] have learned that ordinary people are capable of unspeakable acts of violence when they are taught hate fueled by fear. And due to widespread fear, I was hoping to use my commencement speech to inspire my classmates with a message of hope. By canceling my speech, USC is only caving to fear and rewarding hatred.”

As for the commencement cancellation, USC’s shut-it-all-down move echoes the excessive caution displayed by the American education system in the face of the COVID-19 pandemic.

Those echoes are all too loud for USC seniors — four years ago, many of them were denied high school graduation ceremonies in the name of “safety.”

{kind=link}

Now, their college commencement ceremony has been similarly vaporized, only by a different set of quivering academics.

“It is both enabling and irresponsible. Rather than protect students and their families at this important and well-earned event in their lives, the university is yielding to the mob. It is a feckless and feeble response to what should have been an easy decision for any administrator,” said Jonathan Turley.

After hearing the news, one of those seniors, who goes by @gracieflynn12, took to TikTok to vent:

“The seniors that are graduating college right now are the seniors that graduated in 2020, where we didn’t have a high school graduation. A lot of us had drive-through fake graduations or no graduation at all. And now we are seniors getting ready for our first real graduation and it just got cancelled…

…I just had my last class ever, and just right after, should be celebrating. But we just got the new that we have no graduation, so now all my roommates are depressed, and we were all literally just sitting in the living room in tears.”

Here, a USC senior who was robbed of a high school graduation by the COVID Panic reacts to USC cancelling her college commencement because of an anti-Israel valedictorian and fear of protests…

This is the world that liberals want and are creating for her and her generation.😡🥲 pic.twitter.com/QhbTAfBBcp

— John Ziegler (@Zigmanfreud) April 26, 2024

…but at least one especially admirable voice against the Covid regime is being consistent:

It was wrong for public health tyrants to cancel high school graduation for the senior class of 2020.

It is wrong for USC to cancel the big graduation ceremony for their undergraduate class of 2024.

Let the kids (ok, young adults) celebrate graduation for once! pic.twitter.com/FA6qR2mGQ0

— Jay Bhattacharya (@DrJBhattacharya) April 26, 2024

Jonathan Turley summed up the situation succinctly: “The problem of violent protests and threats on campus is not solved by removing the potential victims. To yield this ground is to surrender control over not just the campus but the academic operations of the school. Higher education has to aspire to be more than a mere mobocracy where threats not logic prevail. “

Tyler Durden

Fri, 04/26/2024 – 11:25

Retail Sales Data Suggests A Strong Consumer Or Does It

Retail Sales Data Suggests A Strong Consumer Or Does It

Authored by Lance Roberts via RealInvestmentAdvice.com,

The latest retail sales data suggests a robust consumer, leading economists to become even more optimistic about more robust economic growth this year. To wit:

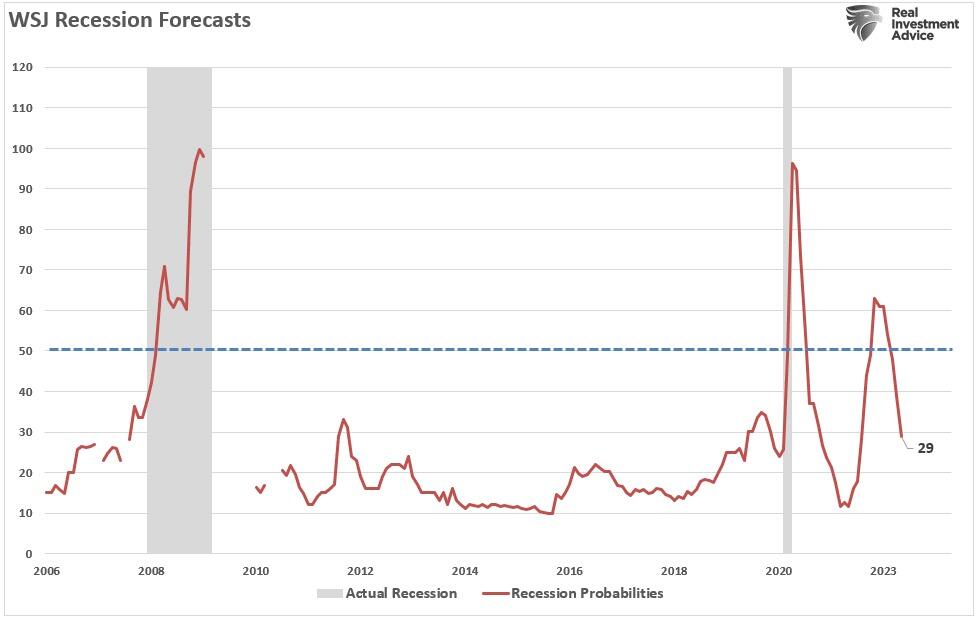

“It has been two years since forecasters felt this good about the economic outlook. In the latest quarterly survey by The Wall Street Journal, business and academic economists lowered the chances of a recession within the next year to 29% from 39% in the January survey. That was the lowest probability since April 2022, when the chances of a recession were set at 28%.

Economists don’t think the economy will get even close to a recession. In January, they, on average, forecast sub-1% growth in each of the first three quarters of this year. Now, they expect growth to bottom out this year at an inflation-adjusted 1.4% in the third quarter.” – WSJ

{kind=link}

According to the March retail sales data, consumer spending added “fuel” to economists’ exuberance about this year.

Rising inflation in March didn’t deter consumers, who continued shopping at a more rapid pace than anticipated, the Commerce Department reported Monday. Retail sales increased 0.7% for the month, considerably faster than the Dow Jones consensus forecast for a 0.3% rise though below the upwardly revised 0.9% in February, according to Census Bureau data that is adjusted for seasonality but not for inflation.” – CNBC

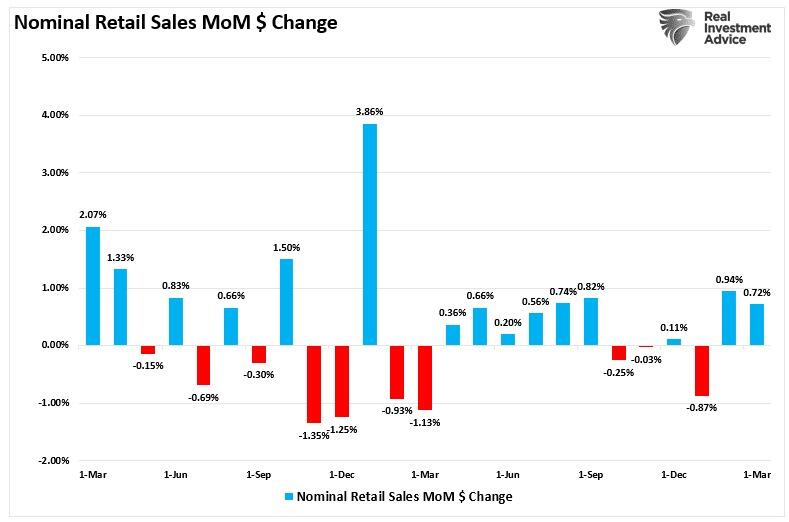

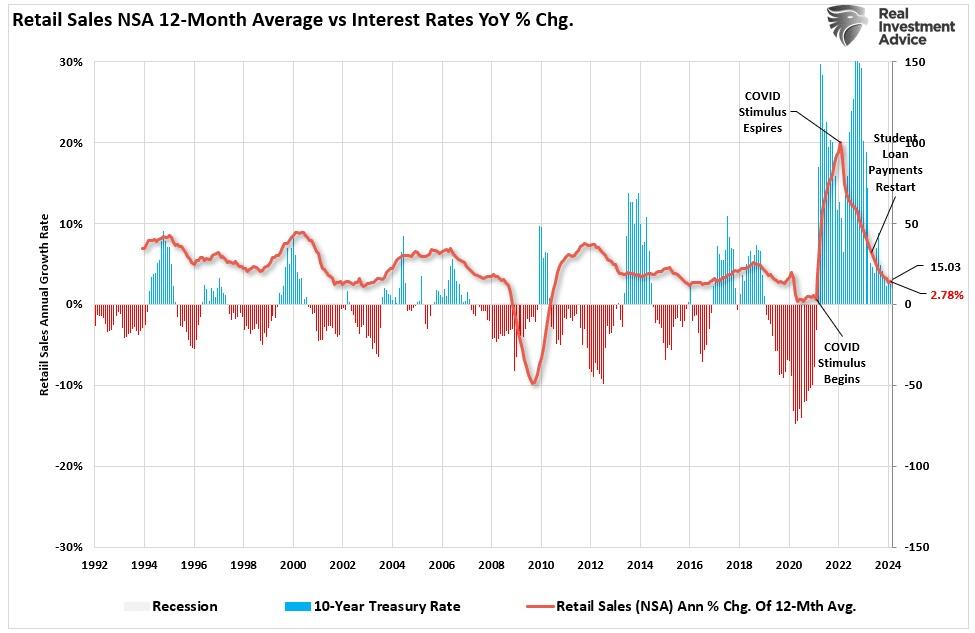

The chart below shows the monthly change in the retail sales data over the last two years.

{kind=link}

While mainstream economists trumpeted the strength of the consumer, the March retail sales data had some interesting points worth noting.

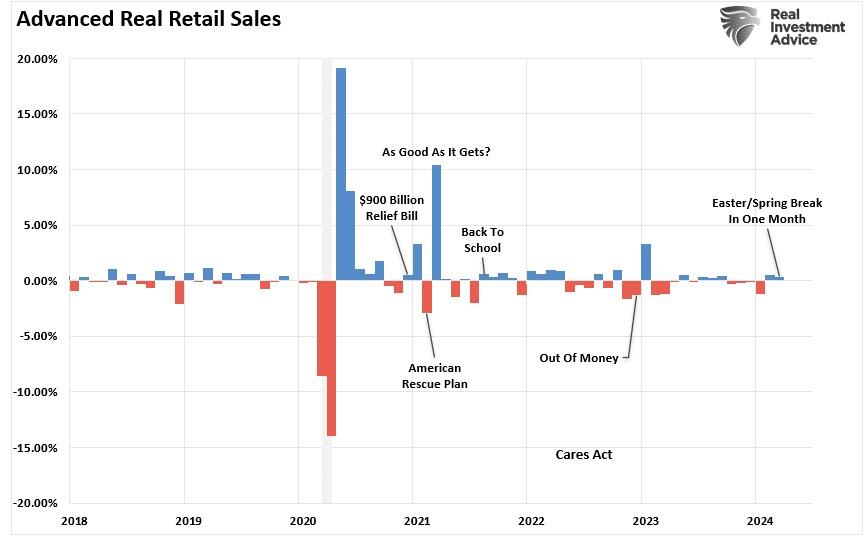

First, retail sales data was extraordinarily weak from October to January, the traditionally strongest shopping months of the year. That period included Halloween, Thanksgiving, Christmas, and NYear’sr’s. So, to some degree, the strength of spending over the last two months is unsurprising as, eventually, consumers need to buy goods or services previously postponed.

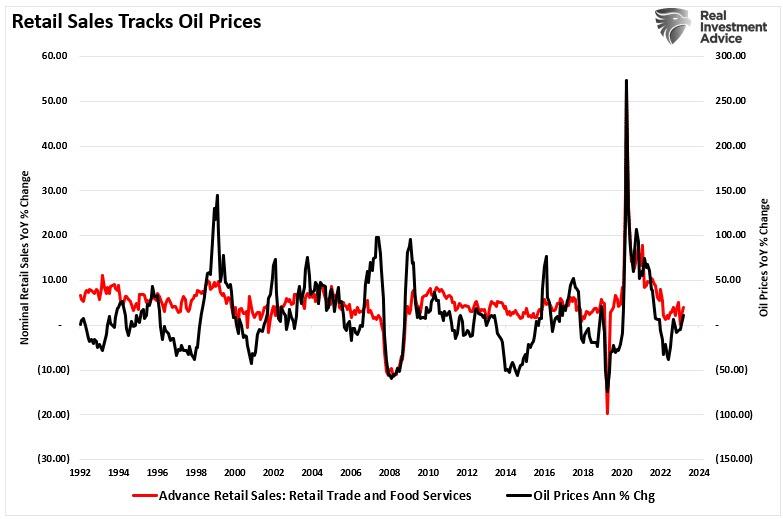

Secondly, while the March retail sales data was strong, it was weaker than February. However, March contained two significant spending periods, Spring Break and Easter, which generally don’t occur. Since Spring Break and Easter are considerable travel and shopping periods, it is unsurprising that the retail sales data increased with oil prices rising. As shown below, there is a very high correlation between nominal retail sales and oil prices.

{kind=link}

Paying More For The Same Amount

Economists often overlook another important point about the retail sales data. As noted above, the March retail sales report was NOT adjusted for inflation. Furthermore, the report is in nominal “dollar volume” and not the amount of goods or services sold. Oil and gasoline prices are an excellent example of the issue with the retail sales data.

Let’s assume you own a car with 18-gallon fuel tank. Your daily activities are mostly going to work, going to the grocery store, eating out, having entertainment, etc. As such, you consume one tank of gas each week. Here is the math:

Week 1: 18-gallons of gas @ $3/gallon = $54.

That week, the store adds $54 to the monthly retail sales total for selling 18 gallons of gasoline. However, the price will increase to $4 per gallon next week.

Week 2: 18-gallons of gas @ $4/gallon = $72.

Here is the question.

While the retail sales data increased by $18 in week two, did the consumer purchase more gasoline? In other words, if the economy’s strength is ultimately measured by how much we produce (gross domestic product), then does spending more for the same amount of goods or services equate to a stronger economy?

The picture is quite different if we adjust the nominal retail sales data for inflation. Again, it is unsurprising that even on an inflation-adjusted basis, retail sales rose in February after declining for four months previously. However, with March containing Spring Break and Easter, the data suggests a weaker consumer that headlines tout.

{kind=link}

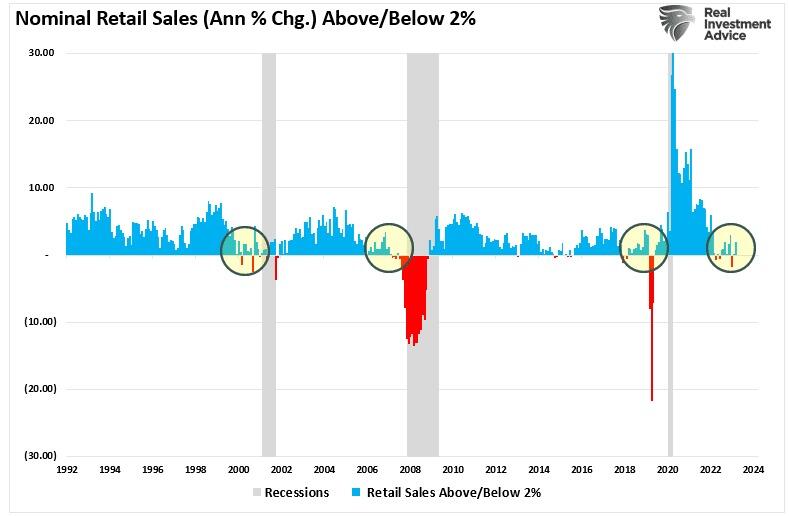

It is worth noting that retail sales data is not very useful in determining whether the economy is nearing a recession. As shown below, an annual growth rate of 2% has been a good marker for economic growth. As such, retail sales should grow at roughly 2% annually as well, given that personal consumption expenditures comprise approximately 70% of the economic equation. However, other than 2007, retail sales did not clarify economic strength.

{kind=link}

In other words, spending more for the same amount of goods and services is not a sign of economic strength.

Economic Forecasts Tend To Be Erroneous

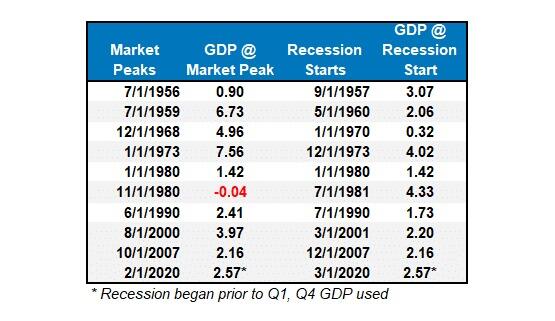

Furthermore, while the recent nominal sales data was robust, it is crucial to remember the economic data has a significant lag. Each of the dates below shows the economy’s growth rate immediately before the onset of a recession. You will note in the table that in 7 of the last 10 recessions, real GDP growth was running at 2% or above. In other words, according to the media, there was NO indication of a recession. But the next month, one began.

{kind=link}

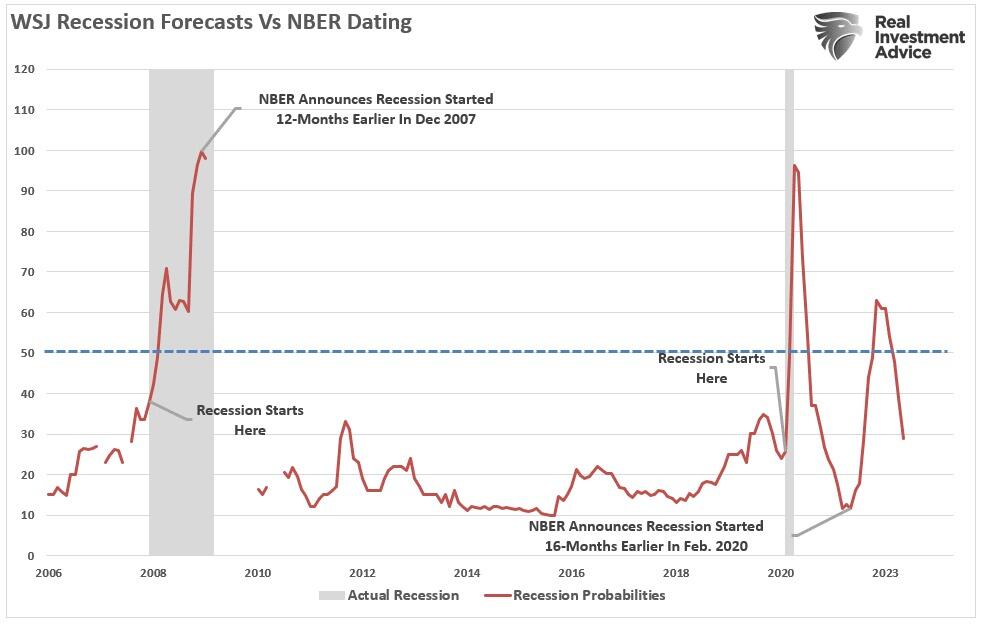

Crucially, I am not saying a recession is starting next month. However, I suggest that relying heavily on one month’s retail sales data to claim the economy avoided a recession is not likely ideal. Let’s revisit that chart of the WSJ economic forecast. I have added two notations: the start and end of recessions and when the NBER officially dated that period. As shown in both previous recessions, WSJ economists had a very low probability of the economy entering a recession just before it occurred.

{kind=link}

The reality is that on an inflation-adjusted basis, the retail sales data suggests the consumer remains weak. While spending more to buy the same amount of goods or services may look good on paper, the average household has less money to spend elsewhere. As shown, the annual rate of change in real retail sales is near some of the lowest levels outside of a recession.

{kind=link}

Lastly, consumer credit supporting retail sales will become more problematic with rising interest rates. Higher interest rates tend to reduce the average growth rate of retail sales data.

{kind=link}

Our advice is to remain cautious about economic exuberance. Those forecasts are often disappointing.

Tyler Durden

Fri, 04/26/2024 – 11:05

JPY Plunges To Fresh 34-Year-Lows After BoJ Does Nothing… Again

JPY Plunges To Fresh 34-Year-Lows After BoJ Does Nothing… Again

Having already lost more than 10% of its value versus the US dollar this year, the yen plunged further overnight after Bank of Japan Governor Kazuo Ueda indicated monetary policy will stay easy as he kept rates unchanged and showed little to no support for the embattled currency during the press conference.

While investors had not expected the BoJ to change its policy this week, there was an expectations that Ueda would strike a hawkish tone regarding future rate rises to slow the yen’s decline.

Instead, Ueda said at a news conference on Friday that the central bank’s board members judged there was “no major impact” from the weaker yen on underlying inflation for now.

“Currency rates is not a target of monetary policy to directly control,” he said.

“But currency volatility could be an important factor in impacting the economy and prices. If the impact on underlying inflation becomes too big to ignore, it may be a reason to adjust monetary policy.”

And that sent the currency reeling (amid chaotic swings) back above 157/USD…

{kind=link}

Source: Bloomberg

“There is no intention by the BoJ to stop the yen’s decline, at least looking at its statement and its outlook report,” said UBS economist Masamichi Adachi.

“The finance ministry will have to act [to stem the yen weakness]… It would have been more effective if both the government and the BoJ faced the same direction,” he added.

Blowing further below the ‘interventionist’ levels seen previously to a fresh 34-year low…

{kind=link}

Source: Bloomberg

“Markets remain on high alert for any indication of whether the yen’s current weakness will be interpreted as a lasting inflationary signal,” said Naomi Fink, global strategist at Nikko Asset Management.

“The BoJ however is likelier to find any knock-on impact from yen weakness upon inflation as more concerning than short-term currency moves.”

Driving the depreciation is the yawning gap between the interest rates in the US – which are at highest in decades after the Fed’s aggressive tightening cycle last year – and those in Japan, where borrowing costs remain stubbornly low near zero.

“Intervention is possible at anytime, but it could have been just someone selling a large lot, which stoked intervention speculation and spurred follow-through moves,” said Koji Fukaya, a fellow at Market Risk Advisory Co. in Tokyo.

“It does not look like intervention, but the only way to confirm is to check data that will be released later by the Ministry of Finance.”

Policymakers have repeatedly warned that depreciation won’t be tolerated if it goes too far too fast.

Finance Minister Shunichi Suzuki reiterated after the BoJ meeting that the government will respond appropriately to foreign exchange moves.

Potential triggers for interventions are public holidays in Japan on Monday and Friday next week, which bring the risk of volatility amid thin trading.

“Should the yen fall further from here, like after the BOJ decision in September 2022, the possibility of intervention will increase,” said Hirofumi Suzuki, chief currency strategist at Sumitomo Mitsui Banking Corp.

“It is not the level but it’s the speed that will trigger the action.”

But so far, nothing! And so the market continues to call Ueda and Suzuki’s bluff, knowing full well that a sudden intervention will perhaps briefly support the currency but will pancake the current gains in Japanese stocks.

However, not everyone is convinced intervention is imminent.

In a note this morning, Deutsche Bank says the currency’s decline is warranted and finally marks the day where the market realizes that Japan is following a policy of benign neglect for the yen.

We have long argued that FX intervention is not credible and the toning down of verbal jawboning from the finance minister overnight is on balance a positive from a credibility perspective. The possibility of intervention can’t be ruled out if the market turns disorderly, but it is also notable that Governor Ueda played down the importance of the yen in his press conference today as well as signalling no urgency to hike rates. We would frame the ongoing yen collapse around the following points.

Yen weakness is simply not that bad for Japan. The tourism sector is booming, profit margins on the Nikkei are soaring and exporter competitiveness is increasing. True, the cost of imported items is going up. But growth is fine, the government is helping offset some of the cost via subsidies and core inflation is not accelerating. Most importantly, the Japanese are huge foreign asset owners via Japan’s positive net international investment position. Yen weakness therefore leads to huge capital gains on foreign bonds and equities, most easily summarized in the observation that the government pension fund (GPIF) has roughly made more profits over the last two years than the last twenty years combined.

There simply isn’t an inflation problem. Japan’s core CPI is around 2% and has been decelerating in recent months. The Tokyo CPI overnight was 1.7% excluding one-off effects. To be sure, inflation may well accelerate again helped by FX weakness and high wage growth. But the starting point of inflation is entirely different to the post-COVID hiking cycles of the Fed and ECB. By extension, the inflation pain is far less and the urgency to hike far less too. No where is this more obvious than the fact that Japanese consumer confidence are close to their cycle highs.

Negative real rates are great. There is a huge attraction to running negative real rates for the consolidated government balance sheet. As we demonstrated last year, it creates fiscal space via a $20 trillion carry trade while also generating asset gains for Japan’s wealthy voting base. This encourages the persistent domestic capital outflows we have been highlighting as a key driver of yen weakness over the last year and that have pushed Japan’s broad basic balance to being one of the weakest in the world. It is not speculators that are weakening the yen but the Japanese themselves.

The bottom line, Deutscxhe concludes, is that for the JPY to turn stronger the Japanese need to unwind their carry trade. But for this to make sense the Bank of Japan needs to engineer an expedited hiking cycle similar to the post-COVID experiences of other central banks. Time will tell if the BoJ is moving too slow and generating a policy mistake. A shift in BoJ inflation forecasts to well above 2% over their forecast horizon would be the clearest signal of a shift in reaction function. But this isn’t happening now.

The Japanese are enjoying the ride.

But there is potential for yen upside as Bloomberg’s Simon White notes that profit taking on foreign asset positions might soon prompt some yen repatriation and pressure USD/JPY lower.

If it is perceived that the yen won’t get much cheaper due to intervention risk, domestic investors might choose to start switching some of their US equity positions back to the domestic market, repatriating yen and pressuring USD/JPY lower in the process.

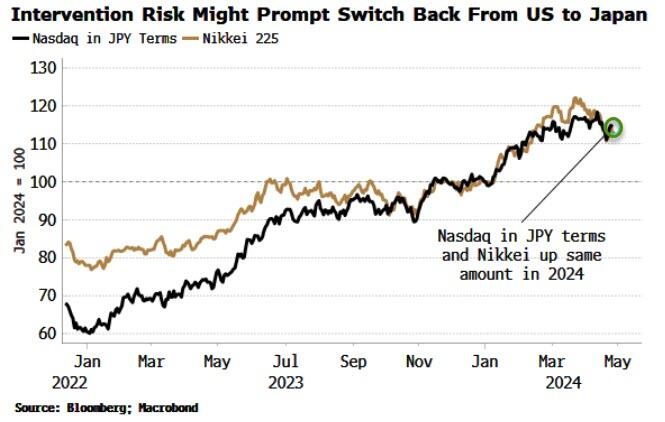

The chart below shows that on the year, the Nasdaq in yen terms and the Nikkei are both up by the same 13%-14% on the year. A stronger yen would present an ongoing headwind to the US position.

{kind=link}

Equity positions are typically less FX hedged than bond positions, meaning that the repatriation of the currency is not neutered by the unwind of the hedge.

The dynamics of spot trading, options barriers and potential intervention as well as US PCE data released later today will dominate the currency’s short-term gyrations, but the slightly longer-term considerations of profit taking on foreign positions will start to drive the medium-term outlook.

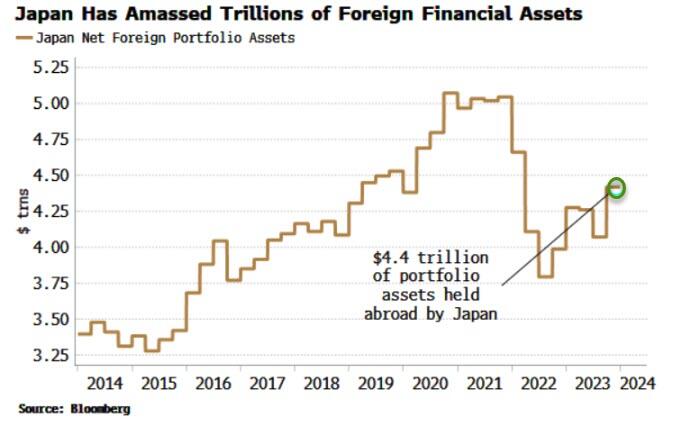

Once that trend establishes itself, longer-term drivers of the yen will come into focus. Japan is the world’s largest net creditor, and there is a significant structural short in the yen.

The country’s net international investment position is $3.3 trillion, but its net position in portfolio assets, i.e. so-called hot flows that could be liquidated quickly, is $4.4 trillion.

{kind=link}

Only a fraction of that being repatriated has significant potential to drive the yen considerably higher.

The question is, how much pain is China willing to take from its regional neighbor’s ‘devaluation’?

Tyler Durden

Fri, 04/26/2024 – 10:50

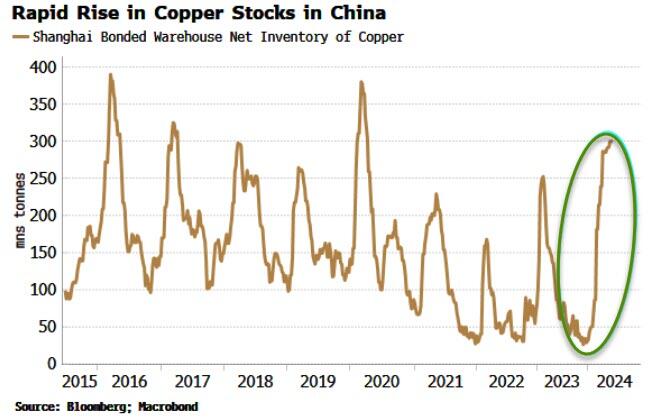

Yuan Devaluation Fever Heats Up As China Stockpiles Metals

Yuan Devaluation Fever Heats Up As China Stockpiles Metals

Authored by Simon White, Bloomberg macro strategist,

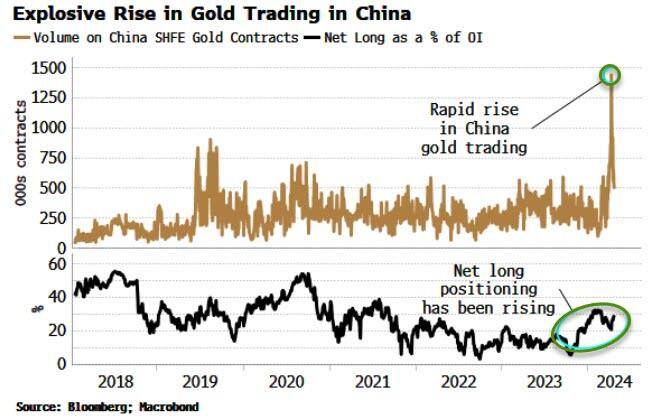

Gold trading in China has exploded and stocks of copper have risen sharply prompting speculation that policymakers are on the brink of a yuan devaluation. Even though it’s still a tail-risk, it’s one requiring greater vigilance as the economy becomes increasingly deflationary, redoubling capital outflow pressures.

The yuan has been steadily falling versus the dollar this year. So far the decline has been measured, but activity in commodities has prompted conjecture that China is about to orchestrate a significant one-off yuan devaluation. Futures gold trading in China has moved sharply higher, and the net long position has been rising.

{kind=link}

Also, there has been a sharp rise in China’s copper stocks. Copper as well as other commodities is used as a source of collateral in China.

{kind=link}

USD/CNY has been bumping up against the upper band of the PBOC’s fix for the currency pair.

{kind=link}

China has a nominally closed capital account, but it is de facto leaky. Capital outflow is rising, and this puts further pressure on the economy as it has a geared negative effect on domestic liquidity.

Allowing the yuan to depreciate against the dollar (it is appreciating against most other currencies) takes some of the pressure off.

China, though, has been unofficially intervening, via the state banks, to stabilize the yuan’s fall.

Nonetheless, it is still less likely than not they will countenance a significant devaluation of the yuan versus the dollar.

First, it would compromise the financial stability that China has sought to obtain.

Second, it risks a tariff backlash from the US.

Third it may be counter-productive if it looks panicky and prompts even more capital outflow.

The stockpiling could well be for other reasons.

Rising global inflation risks (there is more to come, and even China will likely soon face consumer inflation);

reserve diversification in a more multi-polar world;

and raw materials for solar (AI needs a lot of energy) and EVs, and so on.

China planning for an invasion of Taiwan is another tail-risk that can’t be completely discounted.

Falling bond yields, though, show China is nearing a crunch point (read why here) and will need to do something soon to avert a debt deflation.

Even though a full-scale devaluation is less likely, it’s a non-negligible risk that can’t be ignored.

Tyler Durden

Fri, 04/26/2024 – 10:35

George Soros Paying Student Agitators To Whip Up Anti-Israel Protests

George Soros Paying Student Agitators To Whip Up Anti-Israel Protests

George Soros and his far-left movement is paying student agitators to co-opt and amplify anti-Israel protests at colleges across the country, the NY Post reports.

{kind=link}

The protests, which began at Columbia University, have expanded nationwide – with copycat tent cities erected at colleges including Harvard, Yale, Berkeley in California, the Ohio State University and Emory in Georgia, with organized branches of the Soros-funded Students for Justice in Palestine (SJP) having organized them.

Biden has sparked a wildfire. pic.twitter.com/YXbHCKONcm

— Edward Snowden (@Snowden) April 25, 2024

Which might explain this:

Something odd about those campus tent encampments. Almost all the tents are identical – same design, same size, same fresh-out-of-the-box appearance. Which suggests that rather than an organic process, whereby students would bring a variety of individual tents, someone or some… pic.twitter.com/86JV5BD9NM

— Afshine Emrani MD FACC (@afshineemrani) April 23, 2024

The parent organization of SJP has been funded by a constellation of nonprofits which all lead to Soros.

At three colleges, the protests are being encouraged by paid radicals who are “fellows” of a Soros-funded group called the US Campaign for Palestinian Rights (USCPR).

USCPR provides up to $7,800 for its community-based fellows and between $2,880 and $3,660 for its campus-based “fellows” in return for spending eight hours a week organizing “campaigns led by Palestinian organizations.”

They are trained to “rise up, to revolution.”

The radical group received at least $300,000 from Soros’ Open Society Foundations since 2017 and also took in $355,000 from the Rockefeller Brothers Fund since 2019. -NY Post

The group has three “fellows” who have helped propel the protests into a nationwide phenomenon, which you can read more about here…

We’re sure if the protests get violent, prosecutors will take appropriate action, yes?

{kind=link}

And while many of the protesters are just morons…

“I wish I was more educated.”

Video captured at New York University shows that some of the students protesting there have no idea why. Full reporthttps://t.co/iYSbhaxxEf pic.twitter.com/iqXpoZexiP

— m o d e r n i t y (@ModernityNews) April 25, 2024

Some of them are quite spicy, like the leader of Columbia’s encampment…

“Be glad — be grateful — that I’m not just going out and murdering Zionists. I’ve never murdered anyone in my life, and I *hope* to keep it that way.” This is a top leader of @Columbia’s encampment, with whom the school is “negotiating,” expanding on his thoughts about how Israel… pic.twitter.com/ugodO4O7M5

— Guy Benson (@guypbenson) April 25, 2024

{kind=link}

Tyler Durden

Fri, 04/26/2024 – 10:15

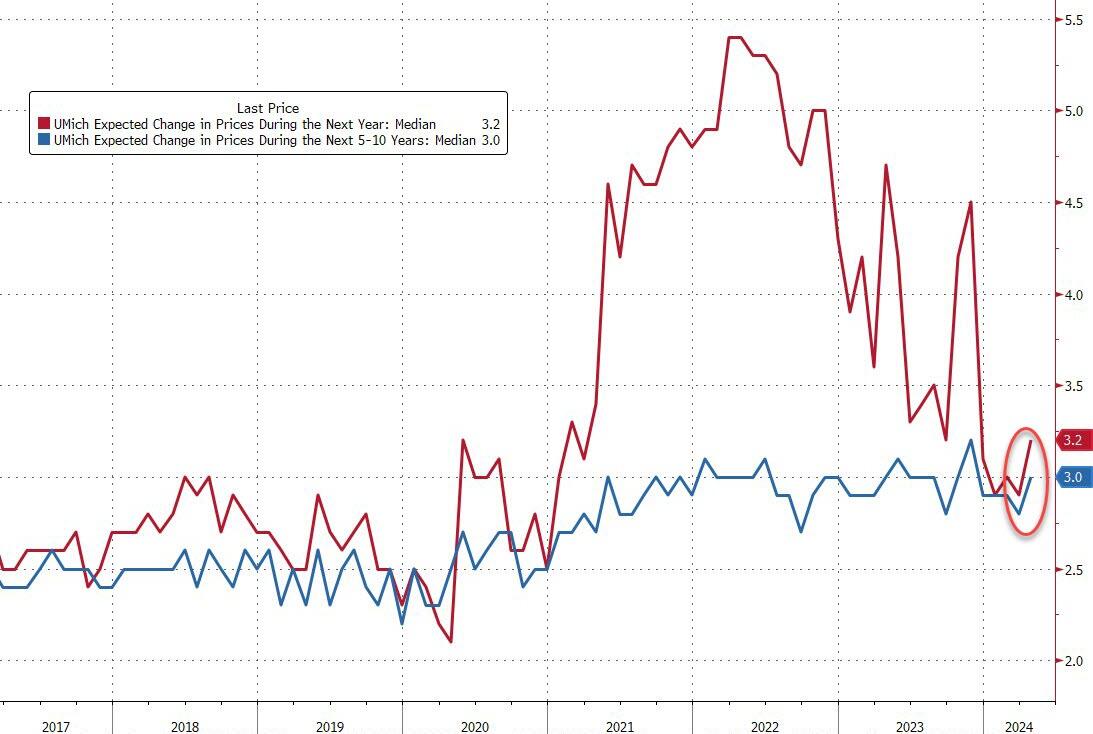

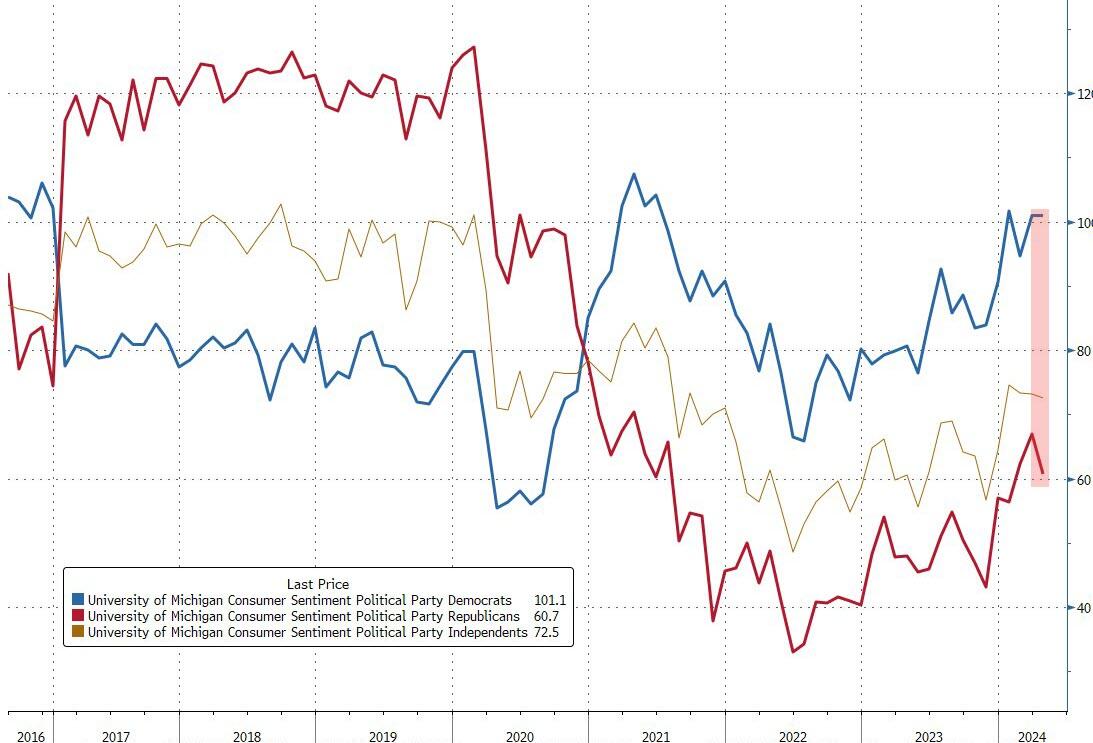

UMich Inflation Expectations Accelerated In April To 2024 Highs

UMich Inflation Expectations Accelerated In April To 2024 Highs

Short-term inflation expectations rose… again… according to the latest UMich sentiment survey with 1-year expectations at 3.2% final, up from preliminary 3.1% for April, and 2.9% for March. This is the highest level since Nov 2023…

{kind=link}

Source: Bloomberg

The headline sentiment also declined in April from three-year-highs. Consumers’ perceptions of their current financial situation and the economic outlook over the next year both slid to four-month lows. The current conditions gauge dropped to 79 from 82.5. A measure of expectations fell to 76 from 77.4.

{kind=link}

Source: Bloomberg

While “consumers’ frustration over high prices in their day-to-day spending decisions grew this month, price concerns for large purchases – durable goods, vehicles, and homes – were all little changed from last month,’’ Joanne Hsu, director of the survey, said in a statement.

About 38% of consumers reported that high prices were weighing down their living standards, up from 33% who said so last month.

Sentiment gauges also provide insight into voters’ feelings about the economy and their finances leading up to the presidential election in November. President Joe Biden’s recent polling bump in key battleground states has mostly evaporated amid economic pessimism, the latest Bloomberg News/Morning Consult poll found.

“Consumers continue to express uncertainty about the future trajectory of the economy pending the outcomes of the upcoming election,” Hsu said.

{kind=link}

Partisan differences in views of the economy remain pronounced. While Democrats and Independents saw little change in sentiment this month, sentiment for Republicans fell about 6 index points.

Republicans reported declines for four of the five components of the sentiment index, reflecting their deteriorating views across multiple facets of the economy. Despite these declines, sentiment for Republicans remains well above 2022 and 2023 levels.

In fact, the current reading for Republicans’ Expectations Index is the second highest (after last month) since the end of 2020, as the Trump presidency came to a close.

Tyler Durden

Fri, 04/26/2024 – 10:09

Why Are There So Many Americans That Can’t Find A Job Even Though They Are Desperate To Be Hired?

Why Are There So Many Americans That Can’t Find A Job Even Though They Are Desperate To Be Hired?

Authored by Michael Snyder via The Economic Collapse blog,

According to the absurd numbers that the government feeds us, the unemployment rate is very low and there are lots of jobs available. But if what they are telling us is true, why are so many Americans not able to find work? As you will see below, some people haven’t been hired even though they have literally applied for hundreds of jobs.

There seems to be an enormous disconnect between what is actually happening in the real economy and the economic narrative that they are constantly pushing. By the time you are done reading this article, I think that you will agree with me.

{kind=link}

Earlier this week, I received an email from a reader that has not been able to find work after seven months of searching.

He gave me permission to share part of that email with you, and it is certainly quite heartbreaking…

Hi Michael,

I am a long-time reader of theeconomiccollapseblog.com, and your recent article comparing the economy to the movie “Weekend at Bernie’s” really stood out to me.

I’m really trying to figure out WHY it is so hard to find a job.

I was laid off from my job as a Custodial Foreman in September 2023, and have had ZERO results for my countless hours spent searching for comparable work.

I don’t know if you want to use any of this for an article or not, but if you do, please just keep doing what you normally do: Praising Jesus Christ. Without my faith in him I don’t know what I’d do.

When I wake up, I make coffee and turn on the computer and go through the state’s unemployment job search sites they provided me when I was laid off. I have been looking and also applying for jobs DAILY since September 2023. And these are not “rocket science” positions; I’m simply looking for Maintenance or Custodial or Groundskeeper type jobs. You know, “normal working class” type jobs.

But after ~300 applications (And these are all just to the jobs that I not only have experience for but also would actually want to do), I have had 1 interview. One interview in 7 months of applying and sending tailored cover letters with, daily!

If the economy is doing so “great”, why can’t he find employment?

Some of you may be tempted to think that he is just an isolated case.

Well, here is another example of an experienced worker that has applied for approximately 300 jobs without any success…

Royal Siu, who lives in Seattle and is trained as a pharmacist, likes to make his friends guess how many jobs he’s applied to. They’ll often toss out some number around 40, he told BI. He’ll tell them to keep going. Most give up by the time they reach 100. That’s when Siu drops that he’s applied to about 300 jobs. “It’s usually a shock factor to them,” he said.

Siu, who’s trying to use his pharmacy degree to work in other parts of healthcare, is finding it harder to land interviews than in a prior job search. The 28-year-old was getting more phone screenings and first and second interviews in the past. This time, it’s been a couple of months since he had a screening call. So he continues to turn to his network but also doesn’t stop applying.

What in the world is going on here?

I thought that there were “millions” of good jobs just waiting for someone to step into them.

Something definitely does not add up.

Even Americans with advanced degrees from top schools are increasingly finding themselves out of work.

If you doubt this, just check out these numbers…

Even at some top business schools, the number of recently minted M.B.A.s without jobs has roughly doubled from a couple of years ago, when U.S. companies were rushing to hire as many workers as they could, according to data from the schools.

At Harvard Business School, 20% of job-seeking 2023 M.B.A. graduates didn’t have one three months after graduation, up from 8% in 2021. At Stanford’s Graduate School of Business, 18% didn’t, compared with 9% in 2021. About 13% of those at the Massachusetts Institute of Technology’s Sloan School of Management didn’t have a job within three months, up from about 5% in 2021.

How are those numbers possible if the unemployment rate is hovering near “historic lows”?

Of course the truth is that we have been sold a lie.

If you do not have a job, you are classified by the U.S. government as either “unemployed” or “not in the labor force”.

In 2008 and 2009, the combined total of those two categories never even reached 90 million.

Today, the combined total of those two categories is over 106 million.

The Biden administration says that only 6,429,000 Americans are officially “unemployed”.

The other 99,989,000 Americans without a job are considered to be “not in the labor force”.

{kind=link}

And more will be lumped into those two categories soon, because large employers all over the nation continue to conduct mass layoffs.

For example, thousands of Tesla workers in California and Texas were just notified that they will be losing their jobs…

The notifications in California and Texas, where the electric vehicle (EV) maker has large presences, came in the form of WARN notices, according to reports.

In California, the planned Tesla headcount reductions will hit approximately 3,300 workers, The San Francisco Standard reported Tuesday.

They will apparently occur at locations in a total of four different cities in the Golden State.

Meanwhile, Texas will see almost 2,700 employees in Austin lose their jobs, according to the Austin American-Statesman.

Sadly, the pace of layoffs is likely to increase during the months ahead, because business activity in the U.S. is declining…

The U.S. economy lost momentum in April, a pair of S&P surveys found, as businesses reported a decline in new orders and reduced employment for the first time since the pandemic.

The flash U.S. manufacturing purchasing managers index slipped to a four-month low of 49.9 in April from 51.9 in March.

The S&P flash U.S. services PMI fell to a five-month low of 50.9 this month from 51.7 in March.

The surveys are the first indicators of each month to give a sense of how the U.S. economy is performing.

Meanwhile, the cost of living crisis just continues to escalate.

Shockingly, at one station in California gasoline now costs $7.29 per gallon…

Soaring gas prices have skyrocketed to a whopping $7.29 per gallon in some parts of California – which is above the current the national hourly minimum wage.

While the average price for a gallon of gas varies from state to state – drivers in a certain Silicon Valley town are facing particularly extortionate rates that set them back almost $150 for a full tank.

The Chevron gas station in Menlo Park was exposed on Sunday by a bewildered customer who posted on X that the price per gallon was four cents ‘above the federal hourly minimum wage.’

If you think that this is bad, just wait until the war in the Middle East transforms into the apocalyptic conflict that I believe it will become.

I am entirely convinced that inflation will continue to be a major problem even as economic activity in the U.S. slows down even more.

We are already experiencing “stagflation”.

What is eventually coming will be so much worse than that.

Of course the economic pain that we are going through is just one of the factors that is systematically destroying our nation.

A Warning to America: 25 Ways the US is Being Destroyed | Explained in Under 2 Minutes pic.twitter.com/qwmBO8DmMt

— Western Lensman (@WesternLensman) April 22, 2024

Just about all of our major institutions are crumbling, just about every sector of our society is in the process of melting down, and conditions are rapidly getting worse all around us.

And now we are heading into the most chaotic election season in the entire history of our country.

This is a recipe for disaster, but there is no turning back now.

* * *

Michael’s new book entitled “Chaos” is available in paperback and for the Kindle on Amazon.com, and you can check out his new Substack newsletter right here.

Tyler Durden

Fri, 04/26/2024 – 09:50