Latest News

China Crossed Biden’s Red Line On Ukraine, So What?

China Crossed Biden’s Red Line On Ukraine, So What?

Authored by Mike Shedlock via MishTalk.com,

It’s ridiculous to have red lines if you are not going to do anything when they are crossed. So what should Biden do?

{kind=link}

China Has Crossed Biden’s Red Line on Ukraine

A Wall Street Journal Op-Ed moans China Has Crossed Biden’s Red Line on Ukraine.

President Biden warned China two years ago not to provide “material support” for Russia’s war in Ukraine. On Friday, Secretary of State Antony Blinken conceded that Xi Jinping ignored that warning. China, Mr. Blinken said, was “overwhelmingly the No. 1 supplier” of Russia’s military industrial base, with the “material effect” of having fundamentally changed the course of the war. Whatever Mr. Biden chooses to do next will be momentous for global security and stability.

Mr. Biden can either enforce his red line through sanctions or other means, or he can signal a collapse of American resolve by applying merely symbolic penalties. Beijing and its strategic partners in Moscow, Tehran, Pyongyang and Caracas would surely interpret half-hearted enforcement as a green light to deepen their campaign of global chaos. Mr. Xi sees a historic opportunity here to undermine the West.

What sanctions? On Who? On What? For How Long?

Op-ed writer Matt Pottinger provided no details, he just wants action. He needs to explain what sanctions make any sense at all, and how they would work.

Numerous US sanctions on Russia, China, Iran, all failed. Hell some of them on Russia and China not only failed they backfired.

So funny. Adding to my post on red lines and sanction failures.

— Mike “Mish” Shedlock (@MishGEA) May 1, 2024

How China Gets Around US Sanctions on Semiconductors

On February 18, 2024, I explained How China Gets Around US Sanctions on Semiconductors

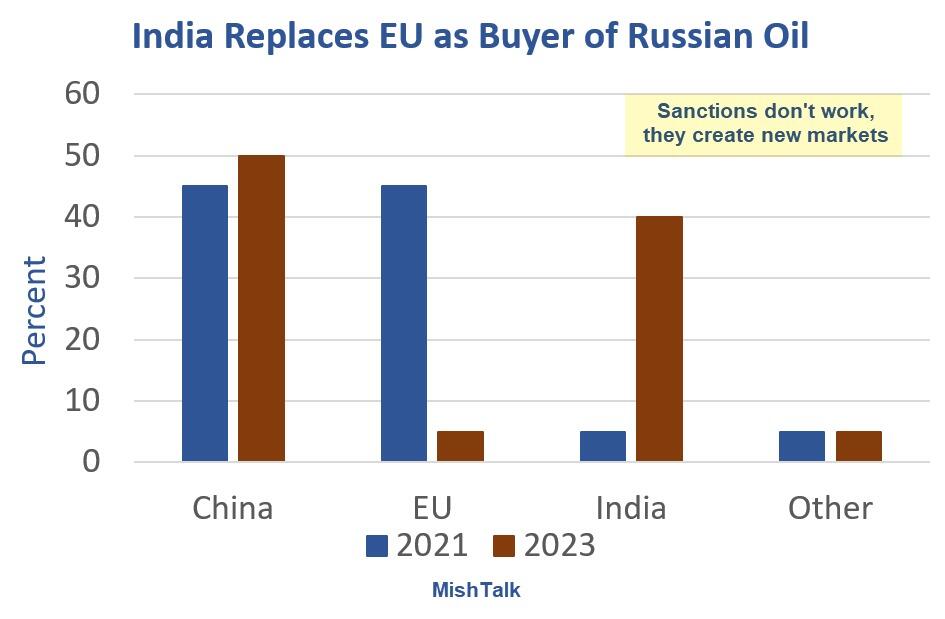

How Russia Makes a Mockery of US Sanctions in One Picture

Unprecedented US and EU sanctions against Russia have had no impact on Russia’s oil exports or revenue. Who’s the beneficiary?

{kind=link}

On December 29, 2023 I noted How Russia Makes a Mockery of US Sanctions in One Picture

On September 19, 2023, I commented Lesson of the Day: Sanctions Don’t Work Because They Create New Markets

Why Sanctions Fail

Someone always has an incentive to break sanctions.

Sanctions create new markets.

This is how Russia sells oil and how China gets access to equipment and parts.

In the case of chips, the US has forced China into a path to self-sufficiency. Hooray?!

Matt Pottinger wants sanctions. He should name some. Nah, what he really wants is to promote his book “The Boiling Moat: Urgent Steps to Defend Taiwan.”

What Color Are Biden’s Red Lines?

On March 10, I asked Are Biden’s Red Lines to Netanyahu Really Yellow or Green?

Presumably you know the answer now, but if not, please consider this idle threat: Biden Threatens Sanctions on Israeli Soldiers Yet Wants More Money for Israel

If you are going to have red lines, I suggest they should be red.

Israel vs China Red Lines

In the case of Israel, there was an easy remedy. Biden could have withheld aid. Instead, when Israel repeatedly crossed lines, Biden stepped up the aid further emboldening Netanyahu.

In the case of China, there are no sanctions or policy actions that make any sense, so there should not be any red lines.

Attempting to set foreign policy for the world is a huge mistake. And setting red lines you cannot or will not do anything about makes one look silly.

Tyler Durden

Wed, 05/01/2024 – 15:40

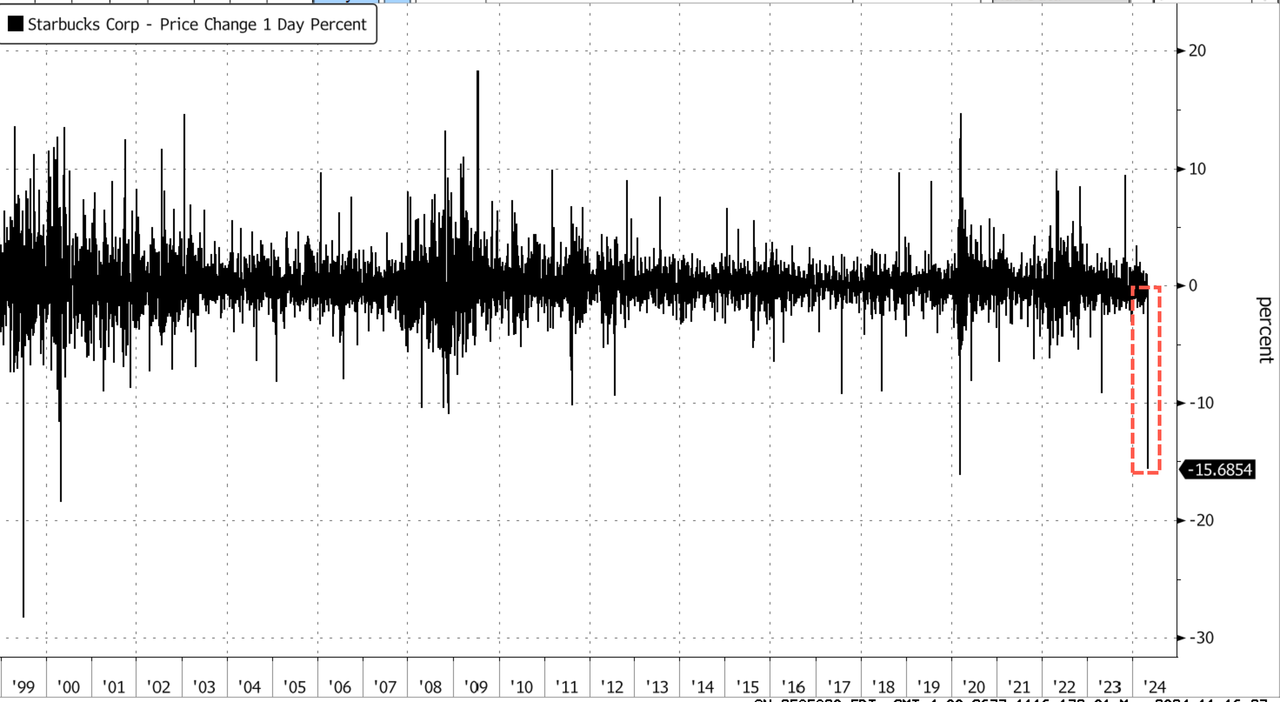

Starbucks On Brink Of Worst Crash Since Dot Com After “Stunning” Earnings Miss

Starbucks On Brink Of Worst Crash Since Dot Com After “Stunning” Earnings Miss

Starbucks shares plummeted by 16% during the early cash session, approaching the -16.2% level last seen during the Covid crash. If intraday losses surpass 16.2% and remain above this level at closing, it would mark the company’s worst single-day loss since the Dot Com crash in early 2000.

{kind=link}

“Starbucks reported what’s perhaps the worst set of results of any large company so far” this quarter, analyst Adam Crisafulli of Vital Knowledge wrote in a note. William Blair downgraded the coffee chain, citing last quarter’s “stunning across-the-board miss on all key metrics.”

Starbucks reported a 4% drop in same-store sales in the second quarter compared with the same period last year, while analysts tracked by Bloomberg were expecting growth. In China, same-store sales plunged 11%. The company’s top geographic segments are showing a pullback in consumer spending.

On Tuesday evening, CEO Laxman Narasimhan started the earnings call with investors by clarifying his unhappiness with last quarter’s results.

“Let me be clear from the beginning. Our performance this quarter was disappointing and did not meet our expectations,” Narasimhan said.

He said major headwinds originate from a “cautious consumer,” adding, “A deteriorating economic outlook has weighed on customer traffic and impact felt broadly across the industry.”

Here’s a snapshot of the second quarter’s earnings results (list courtesy of Bloomberg):

Comparable sales -4%, estimate +1.46% (Bloomberg Consensus)

North America comparable sales -3%, estimate +2.05%

US comparable sales -3%, estimate +2.31%

International comparable sales -6%, estimate +1.36%

China comparable sales -11%, estimate -1.62%

Adjusted EPS 68c, estimate 80c

Net revenue $8.56 billion, estimate $9.13 billion

Operating income $1.10 billion, -17% y/y, estimate $1.35 billion

Adjusted operating margin 12.8%, estimate 14.5%

Operating margin 12.8%, estimate 14.4%

North America operating margin +18%, estimate +19.5%

International operating margin 13.3%, estimate 15.2%

Channel development operating margin 51.7%, estimate 43.6%

Average ticket +2%, estimate +2.41%

North American average ticket price +4%, estimate +4.15%

International avg. ticket -3%, estimate +0.1%

North America net new stores 134, estimate 144.33

International net new store openings 230, estimate 429.23

Comparable transactions -6%, estimate -0.27%

North America comparable transactions -7%, estimate -1.86%

International comparable transactions -3%, estimate +1.37%

Goldman analysts Eric Mihelc and Scott Feiler told clients, “Expectations were for a clear sales miss and a modest EPS miss, but both came worse than the lowered bar.”

They added, “The miss was across geography and was as bad, if not worse, than worst fears.”

Other Wall Street analysts shared the same gloom and doom about the coffee chain (list courtesy of Bloomberg):

Deutsche Bank analyst Lauren Silberman cuts Starbucks to hold from buy

Says the “challenging” results was a sign “headwinds are more pervasive and persistent than we expected, and we have limited visibility into the pace and magnitude of a recovery”

Had thought comparable sales deceleration in the US was more transitory and isolated to a specific cohort

However, with the decline in 2Q traffic and what seems to be limited improvement from Lavender and Spicy Refreshers, Silberman sees it being difficult to “underwrite a meaningful reacceleration,” which is key to the bull case

William Blair, Sharon Zackfia (cuts to market perform from outperform)

After healthy demand over the past three years, Zackfia says the “tide has turned quickly,” with Starbucks posting the weakest traffic performance outside the pandemic or Great Recession

China now “looks more fragile,” with comparable sales down 11%, and even Starbucks Rewards members “took a rare dip,” she adds

Jefferies, Andy Barish (hold)

There was a “notable” miss on US and international comparable sales as well as EPS, and Barish says there is “no easy fix in sight to reaccelerate SSS near-term”

Notes that international comparable sales was “similarly weak,” with traffic and comparable transactions both declining; China’s comparable sales miss and Middle East volatility more than offset positive comps seen in Japan, APAC and Latin America

PT cut to $84 from $94

Citi, Jon Tower (neutral)

Starbucks is “putting a lot of oars in the water to try and paddle” its way back to a stable comparable sales outlook that investors would be willing to underwrite

However, Tower expresses concern that there is not enough “coxswain keeping oarsmen working in unison/with accountability”; adds that it ignores the “true leak in the bottom of the boat,” flagging broad consumer pushback to cumulative transaction growth and the value equation

Notes China store margins are still in the double digits and the segment is profitable despite top-line declines

PT cut to $85 from $95

Cowen, Andrew Charles (hold)

“We believe 2024 guidance has been derisked as we model 0% NA comps & 3% EPS growth, the high end of the range”

Expects shares to be in a “holding pattern” as Starbucks restores credibility while competition and tough macroeconomic conditions present headwinds

PT cut to $85 from $100

Bloomberg Intelligence, Michael Halen and Jennifer Bartashus

“Starbucks slashed fiscal 2024 same-store sales, revenue and EPS guidance and lacks a cogent plan to boost demand”

“We believe several initiatives, including targeting overnight sales, dozens of new products and a four-week mobile- app upgrade cycle are overkill — a distraction unlikely to boost traffic”

On Tuesday, a similar story occurred at McDonald’s when the burger chain reported lower-than-expected quarterly sales growth.

Notably, working-poor consumers are pulling back spending in a period of stagflation (read here & here).

Tyler Durden

Wed, 05/01/2024 – 15:25

The Path Of Least Resistance: Northwestern Reaches Controversial Settlement With Pro-Palestinian Protesters

The Path Of Least Resistance: Northwestern Reaches Controversial Settlement With Pro-Palestinian Protesters

Northwestern University has agreed to a controversial settlement with pro-Palestinian protesters encamped on its campus this week, including a commitment for scholarships for Palestinians, Palestinian faculty appointments, and special housing for Muslim students.

The protesters will also be allowed to continue their protests while agreeing to stay in a particular area of campus. It will also put the students and supporting faculty on bodies to review any university investments and purchases, a major demand from supporters of the Boycott, Divestment and Sanctions (BDS) movement.

{kind=link}

Previously, protesters had reportedly prevented some students and faculty from entering buildings and engaged in property damage.

The Daily Northwestern reported the details of the deal and noted

“the University has committed to provide a conduit for students to engage with the Investment Committee of the Board of Trustees. It will also re-establish an Advisory Committee on Investment Responsibility this fall, which will include students, faculty and staff.

…

In addition, the University committed to some support for Palestinian students and faculty in the agreement. NU will ‘support visiting Palestinian faculty and students at risk,’ and will provide the cost of attendance for five Palestinian undergraduates to attend Northwestern.

…

The University also committed to providing an ‘immediate temporary space for MENA/Muslim students’ — a longtime demand from students on campus — and will provide and renovate a house for MENA/Muslims students as soon as possible. The final house is expected to come in 2026.”

It also includes a commitment of the university to intervene with employers to guarantee that students suffer no consequences for participating in protests in their jobs and internships.

Northwestern (my alma mater) has always chosen the path of least resistance when it comes to protesters, including at times surrendering core academic functions. I have been particularly critical of the loss of freedom of speech and academic integrity on campus.

Students previously succeeded in cancelling a speech by former U.S. Attorney General Jeff Sessions. Student Zachery Novicoff embodied the rising intolerance to free speech on campus. He is quoted as saying “There’s a limitation to free speech. That ends at overtly racist old white dudes.”

I criticized former Northwestern University President Morton Schapiro for his lack of support for free speech on campus. Schapiro denounced what he called “absolute” free speech positions and endorsed speech sanctions, including treating speech as a form of assault.

During his tenure, the university often seemed a mere pedestrian to mob action taken against dissenting voices. For example, we previously discussed a Sociology 201 class by Professor Beth Redbird that examined “inequality in American society with an emphasis on race, class and gender.” To that end, Redbird invited both an undocumented person and a spokesperson for the Immigration and Customs Enforcement. It is the type of balance that is now considered verboten on campuses.

Members of MEChA de Northwestern, Black Lives Matter NU, the Immigrant Justice Project, the Asian Pacific American Coalition, NU Queer Trans Intersex People of Color and Rainbow Alliance organized to stop other students from hearing from the ICE representative. However, they could not have succeeded without the help of Northwestern administrators (including Dean of Students Todd Adams). The protesters were screaming “F**k ICE” outside of the hall. Adams and the other administrators then said that the protesters screaming profanities would be allowed into the class if they promised not to disrupt the class. Really? They were screaming profanities and seeking to stop the class but would just sit nicely as the speaker answered questions?

Of course, that did not happen. As soon as the protesters were allowed into the classroom, they prevented the ICE representative from speaking. The ICE official eventually left and Redbird canceled the class to discuss the issue with the protesters that just prevented her students from hearing an opposing view.

The comments of the Northwestern students were predictable after being told by people like Schapiro that some offensive speech should be treated as a form of assault. SESP sophomore April Navarro rejected that faculty should be allowed to invite such speakers to their classrooms for a “good, nice conversation with ICE.” She insisted such speakers needed to be silenced because they “terrorize communities” and profit from detainee labor. Here is the face of the new generation of censors being shaped by speech-intolerant academics like Schapiro:

“We’re not interested in having those types of conversations that would be like, ‘Oh, let’s listen to their side of it’ because that’s making them passive rule-followers rather than active proponents of violence. We’re not engaging in those kinds of things; it legitimizes ICE’s violence, it makes Northwestern complicit in this. There’s an unequal power balance that happens when you deal with state apparatuses.”

Last year, the Northwestern student body banned press from meetings to protect students from the harm of media coverage. The students also have previously frozen funds of conservative groups.

The Northwestern journalism faculty is little better. Steven Thrasher, the Daniel H. Renberg Chair of social justice in reporting at Northwestern, who trashed a reporter who waited for the facts before reporting on a police shooting.

Of course, it is not just conservative speakers that the students want to ban. In 2021, they called for the removal of the President of the Board of Trustees. Despite being a major donor and supporter of the school, J. Landis Martin was denounced as a Republican who donated money to former President Donald Trump.

The university issued a statement that “This path forward requires the immediate removal of tents on Deering Meadow, cessation of non-approved use of amplified sound and a commitment that all conduct on Deering and across campus will comply with all University rules and policies. Compliant demonstration can continue at Deering Meadow through June 1.”

The university has long lacked the fortitude to stand up to students engaging in disruptive protests.

The danger of such passivity is evident on our campuses. As Henry David Thoreau warned, “all rivers and most corrupt men follow the path of least resistance.”

Here is the Northwestern agreement.

Tyler Durden

Wed, 05/01/2024 – 15:05

Wall Street Reacts To Powell Unleashing His Inner Dove

Wall Street Reacts To Powell Unleashing His Inner Dove

Ahead of today’s FOMC statement and Powell presser, we said that the bogey for a dovish interpretation today will come not from the Fed’s rate decision, which we knew would be unchanged, but the QT tapering decision…

The big question for today: how much will Fed taper QT by?

If Taper goes to $30BN (from $60BN/month), that means less funding needed in Q3 (most likely from Bills), and means less pressure on issuance. Yields should slide

— zerohedge (@zerohedge) May 1, 2024

… and sure enough, the fact that the Fed announced an accelerated QT tapering and it was bigger than expected ($35BN vs $30BN) is why the market is viewing the Fed announcement as dovish and futures are now soaring.

And while we wait for Powell’s presser to conclude, here are some other hot takes from Wall Street strategists and thinkers:

David Russell, head of market strategy at TradeStation

“The Fed is still in wait-and-see mode before they get dovish. But the data hasn’t been cooperating. This statement keeps investors data dependent and focused on April numbers like CPI two weeks from now.”

Audrey Childe-Freeman, chief G-10 FX strategist at Bloomberg Intelligence

“A first glance at the statement brings dollar bears some breathing space as the language adjustment is not as hawkish as may have been feared, though the reference about underwhelming inflation progress entertains a potential new layer of hawkishness at a later stage that could contain dollar downside ahead of the press conference. Muted dollar reaction so far captures this well.

“The language embraced thus far does not signal that the narrative has shifted back to new rate-hike debates, but rather to pushing back the timing on a rate cut. This is probably good enough for near-term euro-dollar relief given the feared hawkish pivot.”

Brian Coulton, chief economist at Fitch Ratings

“With unemployment still low and the labor market still tight, there is only a limited risk to the Fed’s employment mandate from waiting longer before embarking on rate cuts. On the other hand the risk of failing to get inflation down on a sustained basis seems to be rising as each week goes by. Patience is the watchword now for the Fed and the risk of fewer or no rate cuts this year is growing.”

Erica Adelberg, Bloomberg Intelligence’s mortgage-backed securities strategist:

“Making it explicit that any surplus MBS paydowns will be reinvested into Treasuries could adversely affect the MBS/Treasury basis, but at this point MBS paydowns are projected to be about half of the $35 monthly cap on average for the foreseeable future. The average loan rate backing the Fed’s MBS holdings is more than 300 bps below current mortgage rates, so it would take a significant interest rate rally to hit the MBS cap.”

Kathy Bostjancic, Chief Economist at Nationwide:

“We expect Chairman Powell will underscore this hawkish pivot in his press conference and emphasize that the timing of pace of rate cuts will depend highly on the future path of inflation. He likely will indicate the Fed is on an extended pause until inflation resumes its disinflationary trend.”

Ira Jersey, Bloomberg rates strategist:

“His lack of comment about the possibility of a hike is interesting, and I’d be surprised if he’s not asked about the potential for hikes in the press conference. But it seems that ‘on hold’ is his base case for now.”

Bloomberg Economics’ Anna Wong and Stuart Paul:

“For anyone wondering if this year’s hot inflation readings were just a blip, the May 1 FOMC meeting offered a clear answer: Hawkish tweaks to the statement show policymakers have lost confidence that inflation is moving in the right direction. At the same time, the Fed announced it would start tapering its balance-sheet run off in June – a month earlier than we expected — and will reduce the runoff cap by a bit more than we foresaw. That initially comes across as dovish, but the motivation here is key. If it turns out the Fed wants the run-off process to last longer — ultimately boosting the chance that its balance sheet will return to pre-pandemic size – that actually would be hawkish.”

Developing

Tyler Durden

Wed, 05/01/2024 – 14:51

Watch Live: Fed Chair Powell Walk The ‘Asymmetric’ Tight-Rope At Today’s Presser?

Watch Live: Fed Chair Powell Walk The ‘Asymmetric’ Tight-Rope At Today’s Presser?

As expected, no change in rates from The Fed, and a hawkish bias to the language changes in the FOMC statement.

The bigger than expected QT taper news is noteworthy and Powell will have to explain why they are ‘easing’ this policy more than expected while inflation remains ‘out of control’… and they are not ready to cut rates.

So now it’s down to Powell to avoid a faux pas (as we detailed below) over shifts in The Fed’s ‘asymmetric’ response function.

Watch Powell walk that tightrope live here (due to start at 1430ET):

* * *

As we detailed earlier, today’s Fed meeting had the market feeling (and positioned for) “HAWKISHNESS,” especially after the ECI pile-on yesterday, which didn’t simply “upside surprise,” but re-accelerated to 1.2% after ending 2023 at 0.9%, and showing that persistent wage pressures further add to the risk of keeping inflation “too elevated” for the Fed.

However, according to Nomura MD Charlie McElligott, the largest risk with the Fed today is that there will be no summary of economic projections / no dot plots…

…meaning that outside of the usual statement, it will be Powell’s press conference alone that dictates market behavior… and the backtest on that is a bit dicey, with some historic faux pas in-sample.

{kind=link}

He’s gotta find a way to “keep it in the pocket,” where his language simply must message “balance of risks”…

…which means (as we detailed earlier) that he dangerously must “toe the line” on widening out the Fed path away from currently asymmetric “when cut?”-messaging dating back to Dec ’23…

…and instead back to a two-way distribution with both ‘cut’ and honest-to-God ‘hike’ –optionality.

Nomura’s rates guru Jonathan Cohn details just how narrow a path it is for Powell:

Powell’s FOMC presser and, in particular, his answer to the inevitable question around potential hikes represents a key risk.

Following meaningful policy path repricing since CPI and reorientation of Fedspeak, the bar for Powell to exceed market hawkishness is high.

Powell, pricing, positioning

What to expect

Statement:

Our economists expect two hawkish changes (see their preview here)

Change “inflation has eased over the past year, but remains elevated” to “inflation remains elevated”

Removal of “greater” in the Fed’s expectation that it would not ease rates “until it has greater confidence that inflation is moving sustainably toward 2%”

Presser:

Powell’s FOMC presser will again be highly scrutinized, particularly his answer on whether hikes are in play. Bostic and Bowman flagged hikes as a risk and Williams did not rule them out, inviting a reassessment of two-way risk. Though Powell will likely maintain that policy is restrictive, he will also likely want to retain optionality amid high uncertainty around neutral. The phrasing of that optionality sentiment will be critical.

Is the market ready / priced?

How much is priced: The market has repriced a lot, going from 63bp of cuts in 2024 pre-CPI to 28bp currently. Market-implied year-end rates for 2024 and 2025 are well above the median dots, granted the March dot plot had some ‘cuspy’ medians. The repricing owes primarily to sticky inflation arresting progress through H2 last year, though there has also clearly been a reduced ‘recession’ premium as well. In terms of hike appreciation, the market-implied probability of a hike by year-end is now around 15%, double what it was pre-CPI. Given the reorientation of Fedspeak amid this sticky inflation (i.e., less emphasis on cuts this year), there is a higher bar for Powell to exceed market hawkishness.

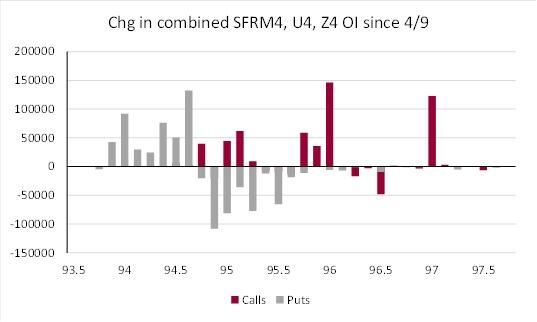

{kind=link}

Repositioning: At the front-end, there have been a couple waves of washouts in ‘sell hike’ trades like 1×2 payer spreads in the sell-off. An examination of open interest changes coupled with insights from our futures desk suggests a good deal of positioning post-CPI was rolled into lower strikes, not simply taken off. And with the increase in put OI in 94.625 (no cut) strike largely a function of buyers, those combining with sales in lower strikes (short skew) seem prepared for something like no cut or one hike scenario. Of course, the risk is that if Powell rhetoric around potential hikes is seen as hawkish and followed by strong NFP and CPI, we move quickly toward the low strikes as the market prices in a higher probability of multiple hikes and we get another positioning flush. I do think that if the Fed feels the need to change its directional bias and hike (not just stay on hold), one has to price in a high probability of multiple hikes, not a one and done. However, I still think there’s a very high bar for the Fed to pay more than lip service to open-mindedness.

{kind=link}

QT slowdown

The Fed is expected to announce a reduction in the pace of QT, likely to $30bn per month for UST. I wouldn’t expect much guidance on an end date. Slowing runoff should theoretically allow for a longer period of QT and lower ultimate level of reserves (thanks to more time for an efficient redistribution of liquidity) – a level around which uncertainty bands are very large.

Putting it together suggests a ‘middle of the road’ Powell can give way to a temporary relief rally, while a blundered characterization of hike optionality could lead to another position flush out and bear-flattening of the yield curve.

Hence, McElligott warns that with all this HAWKISH mentality / sentiment / positioning, the risk is that any surprisingly dovish Fed speak or Data (e.g. NFP Friday), you COULD see potential for an outsized SHORT SQUEEZE / RALLY RISK on stops.

Tyler Durden

Wed, 05/01/2024 – 14:25

FOMC Leaves Rates Unch, Says (Bigger Than Expected) QT Taper To Start In June

FOMC Leaves Rates Unch, Says (Bigger Than Expected) QT Taper To Start In June

Tl;dr: The Fed just told the market that ‘yields are too damn high‘.

* * *

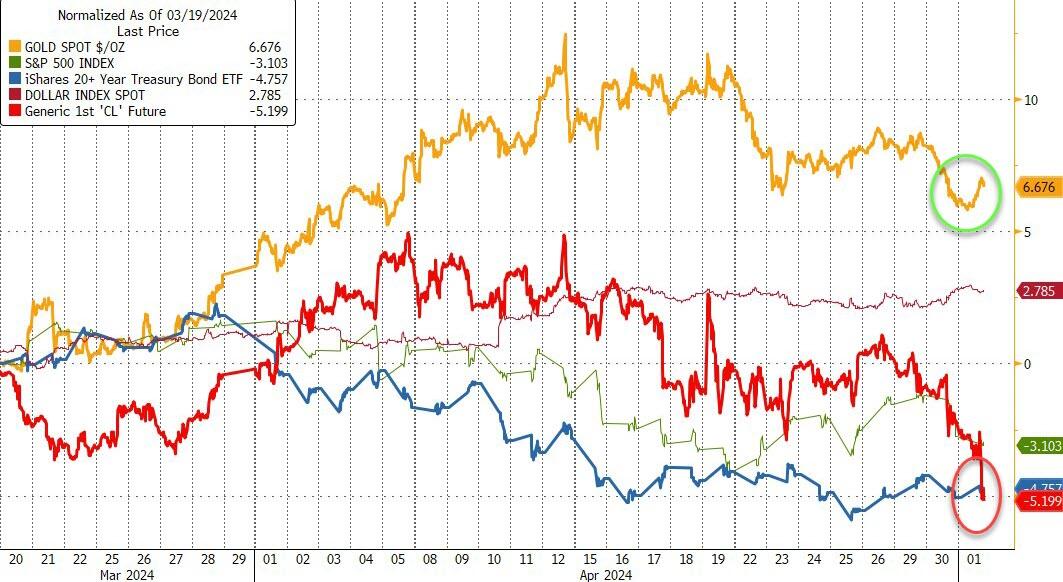

Since the last FOMC meeting, on March 20th, gold has been the biggest outperformer (interesting along with dollar strength), while stocks, bonds, and crude (and crypto) have all been sold (with bonds and oil equally ugly)…

{kind=link}

Source: Bloomberg

And since March 20th, US macro data has serially disappointed…

{kind=link}

Source: Bloomberg

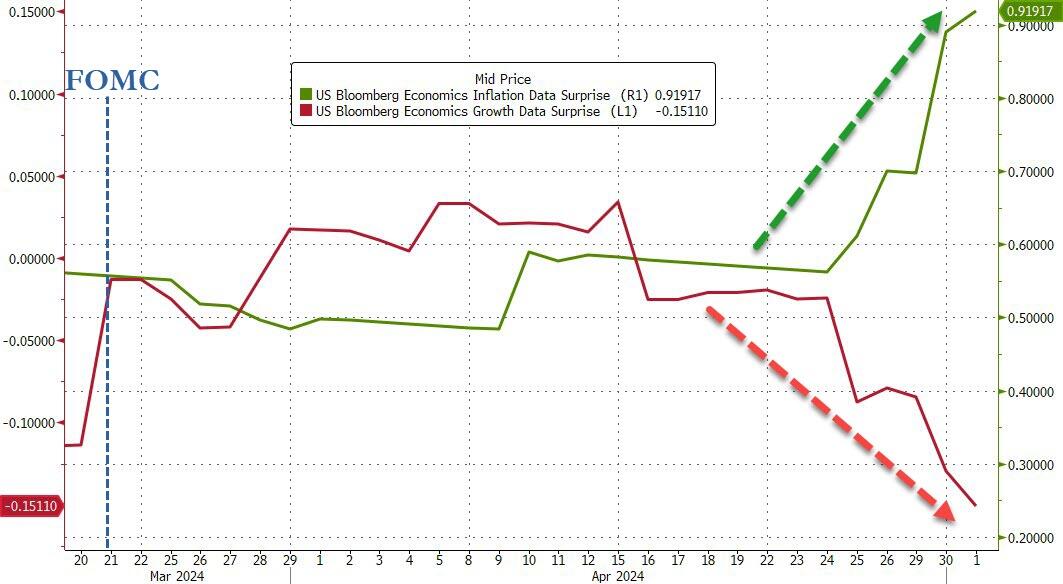

More problematically, since the last FOMC meeting, inflation data has dramatically surprised to the upside and growth data to the downside – screaming stagflation in the face of the Fed…

{kind=link}

Source: Bloomberg

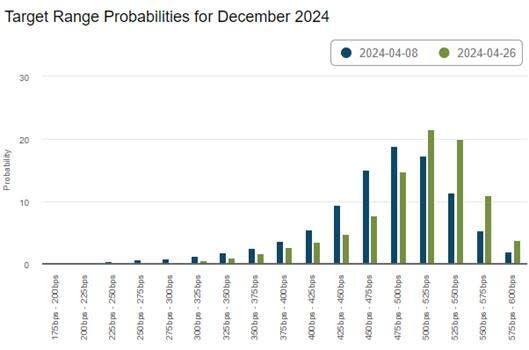

Rate-cut expectations (for 2024 and 2025) have plunged significantly since the last FOMC (that is now just one 25bps rate-cut priced in for 2024)…

{kind=link}

Source: Bloomberg

Expectations are fully priced for a nothing-burger today on rates…

{kind=link}

Source: Bloomberg

… with a slight hawkish bias in the language-changes in the statement (and the possibility of QT-taper signaling). But it will be Powell’s press conference that everyone will be focused on.

So what did The Fed say?

Rates unchanged…

*FED HOLDS BENCHMARK RATE IN 5.25%-5.5% TARGET RANGE

Key statement changes

Fed adds following sentence:

“In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.”

Fed also replaces

“The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance“

with

“The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year.

And the QT Taper is here – and its bigger than expected (-$35BN/mth vs -$30BN expected):

Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion.

The Committee will maintain the monthly redemption cap on agency debt and agency mortgage‑backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities

This means $105BN less gross issuance needed in Q3, with The Fed implicitly saying ‘yields are too high’.

Just as we said…

The big question for today: how much will Fed taper QT by?

If Taper goes to $30BN (from $60BN/month), that means less funding needed in Q3 (most likely from Bills), and means less pressure on issuance. Yields should slide

— zerohedge (@zerohedge) May 1, 2024

Read the full redline below:

{kind=link}

What happens next (on average)?

{kind=link}

Tyler Durden

Wed, 05/01/2024 – 14:00

Lu-Lu-Leveraged: Lululemon Founder Pledges Shares For Margin Loan

Lu-Lu-Leveraged: Lululemon Founder Pledges Shares For Margin Loan

Lululemon’s founder is taking on some lu-lu-leverage – and it’s coming at a time when Lululemon’s stock is more than 20% off its recent highs.

Chip Wilson, the founder of Lululemon, has reportedly used a significant portion of his stake in the company to secure financing from Goldman Sachs Group Inc., according to a new report from Yahoo/Bloomberg.

According to a recent regulatory filing, an investment firm representing the Canadian billionaire pledged 1.8 million Lululemon shares, nearly 20% of his total holdings, as collateral for a $200 million margin loan from the US bank.

Wilson’s stake, valued at approximately $660 million based on Tuesday’s closing price, comes at a challenging time for Lululemon, with its stock declining by 25% since late March due to disappointing US sales and sales projections.

While representatives for Lululemon and Wilson declined to comment, this transaction sheds light on how wealthy individuals leverage their public holdings for substantial liquidity. For Wilson, who relinquished daily management of Lululemon over a decade ago, it signifies a broader investment diversification strategy.

{kind=link}

The report states that the 69-year-old entrepreneur has expanded his investments beyond Lululemon, increasing his stake in Amer Sports Inc. and establishing a real estate firm, Low Tide Properties, among other ventures.

Additionally, he is actively investing in research to find a cure for his rare form of muscular dystrophy.

Pledging shares as collateral is common among the ultra-rich, with examples including Elon Musk leveraging Tesla Inc. stock for personal loans.

While borrowing against shares offers tax advantages, it also carries risks, as evidenced by margin calls during market downturns, such as those experienced at the onset of the pandemic.

Wilson founded Lululemon in 1998 and stepped down as chairman in 2013 following controversies and disagreements with the company’s leadership.

Despite selling a significant portion of his stake a decade ago, he retains control of approximately 8% of Lululemon’s shares, making it his largest individual asset.

Now he better hope yoga pants stay in style…

Tyler Durden

Wed, 05/01/2024 – 13:45

Robert Mueller’s Right Hand Man Warns SCOTUS: You’re “One Vote Away From… The End Of Democracy”

Robert Mueller’s Right Hand Man Warns SCOTUS: You’re “One Vote Away From… The End Of Democracy”

When Robert Mueller appointed Andrew Weissmann as one of his top advisers, many of us warned that it was a poor choice. Weissmann seemed intent to prove those objections correct in increasingly unhinged and partisan statements.

This week, he ratcheted up the rhetoric even further in claiming that the nation is “one vote away” from the end of democracy if the Supreme Court does not embrace the sweeping claims of Special Counsel Jack Smith.

{kind=link}

At the time of his appointment, many Republicans objected to Weissmann’s status as a democratic donor, including his reported attendance of the election night party for Hillary Clinton in 2016. My objection was not to his political affiliations but to his professional history, which included extreme interpretations that were ultimately rejected by courts. Weissmann was responsible for the overextension of an obstruction provision in a jury instruction that led the Supreme Court to reverse the conviction in the Arthur Andersen case in 2005.

Weissmann then became a MSNBC analyst and a professor at New York University. In his book, he attacked prosecutors for refusing to take on his extreme views. Weissmann called on prosecutors to refuse to assist John Durham in his investigation.

Now he is predicting the end of democracy if the Court remand the immunity case for further proceedings.

Weissmann told MSNBC anchor Jen Psaki on Sunday:

I think that it’s important to remember that at the outset, the court had already given Donald Trump the win that he was seeking, which is the delay of the DC trial.

So going into this, this was all upside for him. I mean, I think he had to be thinking, I’m making this really outlandish argument, with ramifications that couldn’t possibly be squared with the text and history. The text of the Constitution or the history of the presidency? So it’s all upside if the court would actually bite on this. And so what was surprising is that there were justices who actually were taking this seriously. And it just was, frankly, shocking.

Remember, going into this, the given was that private conduct was certainly not, immunized from criminal liability. What everyone’s talking about now is, hey, maybe they think that some of this is private and they can go forward, but that was what was given going into this. And the reason people are thinking that is because there seem to be four justices who were really taking Donald Trump’s claim of criminal immunity seriously. And we are.

I mean, I know it sounds like hyperbole, but I think your opening is so correct that we are essentially, as Neil put it, one vote away from sort of the end of democracy as we know it with checks and balances. And to say it’s an imperial presidency that would be created is, it’s frankly saying it would be a king, he would be criminally immune. And that that is what is so shocking is how close we are.

And we are really on the razor’s edge of that kind of result. But for the chief justice.

Just for the record, it sounds less “like hyperbole” than hysteria. The justices were exploring the implications of the sweeping arguments on both sides of the immunity question. What they were not willing to do (as does Weissmann) is simply dismiss any arguments of official status on the part of the accused. That would establish a dangerous ambiguity for the future as prosecutors claim that political statements are private matters for the purpose of prosecution.

Ironically, Weissmann’s lack of concern for the implications of such an interpretation is reminiscent of his prior sweeping arguments as a prosecutor that led to the stinging defeat in the Anderson case.

Of course, there is another possibility is that the justices were not seeking the end of democracy. The Court was honestly trying to get this standard correct not just for this case but future cases. To do so, it will require a record on the underlying actions rather than the categorical threshold judgment made by the district court. The argument showed justices exploring how to avoid a parade of horribles on either extreme with a more moderate approach.

As I previously noted, it has been almost 50 years since the high court ruled presidents have absolute immunity from civil lawsuits in Nixon v. Fitzgerald. That protection applied to acts taken “within the ‘outer perimeter’ of his official responsibility.”

Apparently, that immunity did not endanger democracy.

In United States v. Nixon, the court also ruled a president is not immune from a criminal subpoena. Nixon was forced to comply with a subpoena for his White House tapes in the Watergate scandal from special counsel Leon Jaworski.

Since then, the court has avoided any significant ruling on the extension of immunity to a criminal case — until now.

There are cliffs on both sides of this case. If the court were to embrace special counsel Jack Smith’s arguments, a president would have no immunity from criminal charges, even for official acts taken in his presidency.

It would leave a president without protection from endless charges from politically motivated prosecutors.

If the court were to embrace Trump counsel’s arguments, a president would have complete immunity. It would leave a president largely unaccountable under the criminal code for any criminal acts.

The first cliff is made obvious by the lower-court opinion. While the media have largely focused on extreme examples of president-ordered assassinations and coups, the justices are clearly as concerned with the sweeping implications of the DC Circuit opinion.

Chief Justice John Roberts noted the DC Circuit failed to make any “focused” analysis of the underlying acts, instead offering little more than a judicial shrug.

Roberts read its statement that “a former president can be prosecuted for his official acts because the fact of the prosecution means that the former president has acted in defiance of the laws” and noted it sounds like “a former president can be prosecuted because he is being prosecuted.”

The other cliff is more than obvious from the other proceedings occurring as these arguments were made. Trump’s best attorney proved to be Manhattan District Attorney Alvin Bragg — the very personification of the danger immunity is meant to avoid..

Weissmann is not concerned with the clear politicization of the criminal justice system by Bragg just before one of the most consequential elections in our history.

No, the threat is that justices may want to balance the interests over immunity by rejecting the extreme arguments on both sides. They may try to pursue a course that allows for immunity for official acts or functions while rejecting immunity for non-official acts. Some or all of Trump’s actions or statements could well fall into the unprotected category.

The sense of alarm expressed by legal experts is that the Court would not simply sign off on the absolutist arguments of Smith and, most importantly, allow for a trial before the election.

So how will democracy end if the Court adopts a middle road on immunity? It appears to come down to the loss of a possible conviction to influence the outcome of the election.

At the same time, MSNBC guests are also calling, again, for the packing of the Supreme Court. While conservative justices have repeatedly voted with the Biden Administration, it does not matter. They want the Court packed to guarantee outcomes with the appointment of reliable liberal justices. All of this is being defended in the name of democracy, as was ballot cleansing.

The problem with the escalating rhetoric is that there is not much room for further hysterics. Where does Weissmann and others go from here after predicting the imminent death of democracy?

Pundits have now predicted the creation of camps for democrats, killing journalists and homosexuals, the death of the free press, and tyranny. That leaves only systemic mutilations and Roman decimation.

For lawyers to fuel this hysteria is a sad commentary on the state of our country. Whether a true crisis of faith or simple opportunism, it disregards centuries of constitutional history in overcoming every threat and obstacle. We have the oldest and most stable constitutional system in the world. To suddenly embrace tyranny would require all three branches, and the citizens as a whole, to shred an elaborate system of checks and balances.

We are better than that . . . and these inflammatory predictions.

Tyler Durden

Wed, 05/01/2024 – 13:25

Israel Won’t End War On Hamas As Part Of Hostage Deal, Bibi Tells Blinken

Israel Won’t End War On Hamas As Part Of Hostage Deal, Bibi Tells Blinken

It seems like once again that the Biden White House has almost zero sway, and that Israel is going to do whatever it is going to do, despite continued Washington pressure to halt and avoid the planned Rafah ground assault, with over a million refugees in harm’s way.

A deal is still reportedly on the table, with with no breakthrough being reported amid negotiations mediated by Qatar and Egypt. The deal would reportedly see less than 40 Israeli hostages freed but Hamas wants a permanent, lasting truce that would involve an IDF troop withdrawal from Gaza while Tel Aviv only envisions a temporary pause in fighting.

US Secretary of State Antony Blinken has blamed Hamas for lack of a breakthrough in achieving a deal, saying alongside Israeli President Isaac Herzog in Jerusalem on Wednesday, “No delays, no excuses.” He added: “The time is now.”

File image: this week marks Blinken’s seventh trip to Israel since the war began.

{kind=link}

Gaza’s terror group is “the only reason that that wouldn’t be achieved,” he emphasized. It may not happen “because of Hamas” Blinken stressed. However, Axios’ Israel correspondent Barak Ravid has reported that Blinken has conveyed to Israeli PM Benjamin Netanyahu that the US still stands against an IDF operation in Rafah “without a credible plan for protecting civilians.”

Axios cited Blinken further as saying the Biden administration “thinks there are a better options to deal with the Hamas battalions in the city other than a full scale military operation,” according to a US diplomatic source.

But importantly Netanyahu responded in the Wednesday meeting that he does not intend to accept any deal that includes ending the war. “He said if Hamas doesn’t drop this demand there will be no deal and Israel will invade Rafah, per Israeli and U.S. officials,” Ravid reports.

This is similar to what Netanyahu said the day prior: “We will enter Rafah and we will eliminate the Hamas battalions there – with or without a deal, in order to achieve the total victory.” Blinken is likely trying to get him to backdown from this hardline stance. But even as diplomacy and negotiations intensify, it could yet take several more days to reach a truce or ceasefire deal:

Suhail al-Hindi, a senior Hamas official, has told the AFP by phone that the group will issue a clear response to Israel’s ceasefire proposal “within a very short period”.

Al-Hindi did not provide a specific timeline for Hamas’s response, but another source told the AFP a reply is anticipated within the next day or two.

According to the source, Israel’s proposal includes “real concessions”, yet the question of its complete withdrawal from the Strip remains a likely sticking point.

Complicating things for Israel is the International Criminal Court (ICC) case hanging over Netanyahu and top Israeli officials.

Herzog addressed the potential for arrest warrants to be issued from the Hague-based court: “Our enemies and other elements are trying to undermine the entire process by using international legal forums that were established in order to have a world order that pursues peace, and pursues the values and norms that we all believe in in the modern world.” said the Israeli president. “Especially the efforts done at the International Criminal Court.”

“Israel has a very strong legal system, very strong adjudication and law enforcement system, and it has pursued legal steps from the highest authorities in this land [against] any other citizen,” said Herzog.

Israel expects the leaders of the free world to stand firmly against the ICC outrageous assault on Israel’s inherent right of self-defense. We expect them to use all the means at their disposal to stop this dangerous move. pic.twitter.com/mZB85XbnSd

— Benjamin Netanyahu – בנימין נתניהו (@netanyahu) May 1, 2024

Netanyahu the day prior issued a video address condemning the action. While it would be largely symbolic, as the World Court doesn’t have an enforcement arm, it would be a reputational black eye for Israel at a sensitive moment it faces immense criticism on a global stage for the soaring Gaza death toll and reports of famine.

As for the impending Rafah operation, Netanyahu has been consistent for the past two months that Israel will go into the southern city “no matter what the US says.” There’s been no wavering on this point, however there does appear to have been a delay.

Tyler Durden

Wed, 05/01/2024 – 12:45

If Treasury Bonds Hit 5%, You’re Gonna See Some Serious Sh*t

If Treasury Bonds Hit 5%, You’re Gonna See Some Serious Sh*t

Submitted by QTR’s Fringe Finance

Almost as if all of us Austrian Economists (read: any carbon based life form using common sense when it comes to finance) live in an echo chamber together, a third expert I respect came out over the last few days and has warned that 5% on the 10 year treasury would be the breaking point for markets and the economy.

If my calculations are correct, when this thing hits 5%…you’re going to see some serious sh*t.

Peter Schiff now argues that the Federal Reserve and US Treasury are being forced to confront the reality that inflation is persistent, which has led to an increase in yields, recently reaching 4.7% on the 10 year, the highest since November.

The thought process, for financial neophytes, is that bond traders will continue to sell bonds, driving yields up, in order to make it difficult for the Fed to cut rates — and essentially forcing the Fed to fight inflation head-on instead of capitulating to the economy and markets (should they crash).

This follows Jack Boroudjian’s analysis from last week, stating that rates will keep drifting higher and that 5% to 5.5% is the danger zone: Yields To Trigger “Serious Earthquakes” Across Economy: Jack Boroudjian

It also follows Harris Kupperman’s similar take: Bond Market About To Have An “Aneurism”: Harris Kupperman

Put simply, the Fed faces a dilemma: it needs to raise rates to combat inflation and make Treasuries more appealing, but higher rates would exacerbate the already burdensome debt servicing costs and threaten industries reliant on borrowing. Or, to use the parlance of my recent interview with Matt Taibbi, higher rates simply serve up another day of “sh*t burgers” to the economy, whereas lower rates act as rocket fuel for economic activity (and market confidence).

Schiff warned last week that once the 10-year Treasury yield surpasses 5%, it enters perilous territory for debt-dependent sectors like automotive and commercial real estate. He writes:

The only way the Fed can possibly tame inflation is with interest rates so high that everything collapses. Jamie Dimon himself sees 8% interest rates being needed to tame America’s Fed-fueled inflation beast — but with an economy addicted to a low cost of borrowing, this would make loans unaffordable for entire sectors of the economy that can’t do without.

A serious implosion in commercial real estate would certainly bleed into the banking sector, beginning a chain reaction. Meanwhile, with no chance of the US reigning in spending and getting its fiscal house in order, interest on the US debt can already only be paid with even more borrowed money.

And that chain reaction may already be in the works, as yet another bank failed last week when state regulators shut down Republic First Bank in Philadelphia on Friday evening, transferring its assets to the Federal Deposit Insurance Corp. (FDIC):

As of January 31, 2024, Republic Bank had approximately $6 billion in total assets and $4 billion in total deposits. The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) related to the failure of Republic Bank will be $667 million. The FDIC determined that compared to other alternatives, Fulton Bank’s acquisition of Republic Bank is the least costly resolution for the DIF, an insurance fund created by Congress in 1933 and managed by the FDIC to protect the deposits at the nation’s banks. Republic Bank is the first U.S. bank failure this year; the last failure was Citizens Bank, Sac City, Iowa on November 3, 2023.

Even more concerning is that some of the usual suspects who defend the Fed or the Keynesian line — like Art Laffer, who claimed in 2006 that the impending housing crisis was going to be nothing more than a “nice slow down” — also agrees.

Laffer, president of Laffer Tengler Investments and usually a foil to Schiff’s analysis, told Reuters last week: “Inflation is not coming down like the Fed thought it was. You’re not getting paid to take risk in the bond market right now.”

What’s next — Paul “CPI ex-everything you can possible buy doesn’t look too bad and we should claim victory over inflation” Krugman having a reality check, too?

I won’t hold my breath.

🔥 40% off FOR LIFE: Use this special coupon link and get 40% off an annual subscription, good for as long as you wish to remain a subscriber.

“The fiscal conditions of the U.S. are starting to matter, and it can put tremendous pressure on yields and push down on equity valuations in a very short period of time if the market starts to worry more,” said another analyst, Bryant VanCronkhite, who put a little Wall Street jargon lipstick on the pig of his broader point: markets could fucking crash.

I think Schiff is dead on — with limited options and banks now failing, the Fed may even try to resort to rate cuts or quantitative easing to avert a bond market collapse and stimulate borrowing while rates are high. If this happens, and the Fed prioritizes short-term stability over long-term consequences, it would be like dousing the pilot light of inflation with a 55 gallon barrel of naphtha — which is, to say the least, an explosion. The price of everything that isn’t bolted to the ground will soar: the good (financial assets, gold, etc.), the bad (everyday consumer items), and the ugly (costs of running a business, which will lop on more pressure to raise wages).

“This is especially true now, as the Fed doesn’t want to anger the incumbent during an election year,” Schiff writes, “giving it further impetus to make the economy look as rosy as possible, at least until the start of the next presidential cycle.”

And I’m inclined to side with the Austrians on this one — without gold or other hard assets and sound money in this situation, you risk becoming a case study in what inflation can do to purchasing power in the worst type of way. Personally, I’m partial to gold miners and the GDX still, but hey — read the below disclaimer carefully.

QTR’s Disclaimer: I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have not been fact checked and are the opinions of their authors. They are either submitted to QTR, reprinted under a Creative Commons license or with the permission of the author. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Wed, 05/01/2024 – 12:25